IST,

IST,

Approach Paper on Automated Data Flow from Banks

The document contains the following chapters : Chapter I - Guiding Principles for defining the approach: This chapter deals with the guiding principles and of the Approach for Automated Data Flow. Chapter 2 - Assessment Framework: This chapter provides the detailed methodology (based on a score sheet) for self assessment by banks to determine their current state along Technology and Process dimensions as People dimension being an abstract and dynamic dimension, it is left to the individual banks to calibrate their strategies suitably. Based on the scores of self-assessment, the banks would be classified into clusters. Chapter 3 - Common End-State: This chapter describes the end state, i.e. the stage to be reached by the banks to achieve complete automation of data flow. The end state has been defined across Process and Technology dimensions. Chapter 4 -Benefits of Automation: This chapter elaborates the benefits of automation for the banks. It also defines the challenges and critical success factors for this project. Chapter 5 - Approach for Banks: This chapter provides the approach to be followed by the scheduled commercial banks to achieve the end state. The approach has four key steps. Each step defines a number of activities and tasks that need to be accomplished to complete the step. The Chapter is divided into two sections. The first section deals with the standard approach which has to be followed by all banks and the second section deals with the specific variations from the standard approach and ways to deal with it. Chapter 6- Proposed Roadmap: This chapter provides a framework for grouping the returns submitted to the Reserve Bank. Depending on the group of returns and bank’s cluster (as defined in chapter on Assessment Framework), maximum estimated timelines have been indicated for completing the automation process. Chapter 7 – Summary: This chapter provides the conclusion for the entire approach paper. Annexure A – Assessment Framework – Scoring Matrix and Sample Assessment: This annexure provides the scoring matrix to be used by the banks for the purpose of self assessment. The annexure also provides an illustrative assessment for a representative bank. Annexure B – Task details for the Standard Approach and an illustrative example of approach adopted by bank: This annexure describes the task details required to complete an activity as defined in the chapter on Approach for banks. It also illustrates the adoption of the approach by a sample bank. Annexure B1 – Task Details - “Prepare Data Acquisition layer” Annexure C – Returns Classification: This annexure provides an Excel based classification of representative returns. Appendix I - Other End State Components, Technology Considerations and Definitions: This appendix describes the component-wise technology considerations for the End-state architecture. It also provides definitions of terms used in the document. Appendix II – Global Case Study: This appendix describes the process followed by a global regulator for automating their data submission process. Chapter 1 The guiding principles define the basis on which the entire approach has been framed. These are applicable to all banks regardless of their overall maturity in Process and Technology dimensions. 1.1 Guiding Principles: The guiding principles used in this Approach are detailed below:

Conclusion The guiding principles ensure that the approach to achieve the common end state as mentioned above is independent of the current technologies being used by the banks and can be used by all the banks irrespective of their current level of automation. It seeks to leverage on the huge investment made by banks in technology infrastructure. Chapter 2 The assessment framework measures the preparedness of the banks to achieve automation of the process of submission of returns. This framework covers the Technology and Process dimensions. This chapter explains the process to be followed by the banks to carry out a self-assessment of their current state. 2.1 Banks’ Current State Assessment Framework The end-to-end process adopted by the banks to submit data to Reserve Bank can be broken into the following four logical categories.

Figure 1: Information Value chain for Reserve Bank return submission Banks have to assess themselves on dual dimensions i.e. Process and Technology across each of the above four logical categories which will lead to the assigned scores. Based on the overall score, the bank’s preparedness and maturity to adopt a fully automated process will be assessed. 2.2 Methodology Adopted for Self Assessment 2.2.1 The overall methodology for assessment of current state is defined below: a) Self Assessment by banks based on defined parameters: Banks are required to assess themselves on Technology and Process dimensions. The parameters for Technology and Process dimensions and the corresponding assessment principles are given in Annexure A. b) Calculation of standardized score for each parameter: Each of the parameters is scored on a scale of 0-1. Due to this no single parameter can skew the results when the scores are aggregated. c) Calculation of the category score: The category scores are calculated by using the average of standardized scores of all applicable parameter(s) assessed for the category. d) Calculation of overall maturity score for each dimension: The overall maturity score is calculated using the weighted average of the individual category scores. Weights for assessing the overall maturity score, are calculated across four categories of assessment – namely data capture, data integration & storage, data conversion and data submission. e) Classification of bank as per the Technology and Process maturity score bands: The overall Technology/Process maturity score is used to place the bank in one of the clusters on the two dimensional axis viz. Process maturity vs. Technology maturity as illustrated below :

Figure 2: Technology and Process maturity based bank clustering 2.2.2 As an illustration, a sample assessment of a bank has been provided under Annexure A. A spread sheet with pre-defined fields to enable banks to carry out the self assessment exercise has been provided in paragraph 2 of Annexure A. The classification of the bank will define the implementation roadmap for reaching the end state. Conclusion Based on the level of Process and Technology maturity, each bank is placed in one of the six clusters illustrated above. The timeframe for automation for each group of returns will depend on the cluster in which the bank is placed. This in turn will determine the timelines for the banks to achieve the common end state for all returns. The common end state is the state of complete automation for submission of the returns by the banks to RBI without any manual intervention. To achieve the objective of automated data flow and ensure uniformity in the returns submission process there is need for a common end state which the banks may reach. The common end state defined in this chapter is broken down into four distinct logical layers i.e. Data Acquisition, Data Integration & Storage, Data Conversion and Data Submission. The end state covers the dimensions of Process and Technology. 3.1 Data Architecture Data Architecture refers to the design of the structure under which the data from the individual source systems in the bank would flow into a Centralized Data Repository. This repository would be used for the purpose of preparation of returns. 3.1.1 The conceptual end state architecture representing data acquisition, integration, conversion and submission is represented in Figure 3 given below. Under this architecture, the Data Integration & Storage layer would integrate and cleanse the source data. Subsequently, the Data Conversion layer would transform this data into the prescribed formats. The transformed data would then be submitted to Reserve Bank by the Data Submission layer.

Figure 3: Conceptual Architecture for End State for banks to automate data submission The details of each layer are enumerated below: (a) Data Acquisition Layer: The Data Acquisition layer captures data from various source systems e.g. - Core Banking Solution, Treasury Application, Trade Finance Application, etc. For data maintained in physical form, it is expected that this data would be migrated to appropriate IT system(s) as mentioned in the chapter on approach for banks. (b) Data Integration & Storage Layer: The Data Integration & Storage layer extracts and integrates the data from source systems with maximum granularity required for Reserve Bank returns and ensures its flow to the Centralized Data Repository (CDR). Banks having a Data Warehouse may consider using it as the CDR after ensuring that all data elements required to prepare the returns are available in the Data Warehouse. To ensure desired granularity, the banks may either modify source systems or define appropriate business rules in the Data Integration & Storage layer. (c) Data Conversion/Validation Layer: This layer converts the data stored in the CDR to the prescribed formats using pre-defined business rules. The data conversion structure could be in the form of a simple spreadsheet to an advanced XBRL instance file. The Data Conversion layer will also perform validations on the data to ensure accuracy of the returns. Some common validations like basic data checks, format and consistency validations, abnormal data variation analysis, reconciliation checks, exception report, etc. would be required to be done in this layer. (d) Data Submission Layer: The Data Submission layer is a single transmission channel which ensures secure file upload mechanism in an STP mode with the reporting platforms like ORFS. In all other instances, the required returns may be forwarded from the bank’s repository in the prescribed format. The returns submission process may use automated system driven triggers or schedulers, which will automatically generate and submit the returns. When the returns generation process is triggered, the system may check if all the data required to generate this return has been loaded to the central repository and is available for generating the return. It may start preparing the return only after all the required data is available. The Data Submission layer will acknowledge error messages received from Reserve Bank for correction and further processing. 3.2 Process Elements The key characteristics of the processes need to be defined for each of logical layers:

3.3 Returns Governance Group (RGG) Organization Structure 3.3.1 The governance of the returns submission process at the banks is mostly distributed across the various business departments with little or no centralization. Presently, governance for returns submission, if any, is limited to the following kind of roles: (a) Central team, if any, acting as “Facilitator” - Routing queries to respective departments, monitoring report content, verification of returns, adherence to timelines, interpretation guidelines, clarifications from Reserve Bank on queries. (b) Central team, if any, acting as “Watchdog” – Conducting periodic internal compliance audits, maintaining a repository of who files what returns, and provides updates on regulatory changes to internal users. 3.3.2 In order to strengthen the return submission process in an automated manner, it is suggested that banks may consider having a Returns Governance Group (RGG) which has representation from areas related to compliance, business and technology entrusted with the following roles and responsibilities: (a) RGG may be the owner of all the layers indicated in the end state from the process perspective. The role of the RGG may be that of a “Vigilante and Custodian”. (b) Setting up the entire automation process in collaboration with the bank’s internal Technology and Process teams. This is to ensure timely and consistent submission of returns to Reserve Bank. Though the data within the repository could be owned by the individual departments, the RGG could be the custodian of this data. (c) Ensuring that the metadata is as per the Reserve Bank definitions. (d) Management of change request for any new requirement by Reserve Bank and handling ad-hoc queries. 3.3.3 In the context of the automated submission system being adopted by the banks, the RGG, will have the following responsibilities for each layer of the return submission end state:

Conclusion Each bank may be at a different level of automation, but as defined in this chapter, the end state will be common for all the banks. To achieve this, the banks may require a transformation across dimensions of Process and Technology. The key benefits derived by the bank in implementing the end state are defined in the next chapter. Chapter 4 By adopting an automated process for submission of returns, the banks would be able to submit accurate and timely data without any manual intervention. This process would also enable the banks to improve upon their MIS and Decision Support Systems (DSS), etc. 4.1 Key Benefits of automated data flow for banks: The automation of data flow will benefit the banks in terms of the following:

4.2 A comparison of the issues with the current scenario and benefits of automation is given in the table below:

Conclusion With the realization of the end state objective of automated data flow, the banks may be benefited in terms of enhanced data quality, timeliness, and reduced costs. This Chapter defines the approach to be followed by banks to reach the common end state. The approach, based on the Guiding Principles defined in Chapter 1, is divided into two sections: (a) Standard Approach to be followed by all the banks - The Standard approach assumes that the bank has little or no automation for submission of returns due to which it is possible to provide an end-to-end roadmap for achieving total automation of data flow. The standard approach comprises of four key steps which is divided into activities and further divided into tasks & sub-tasks, which are only indicative and not exhaustive. (b) Variations (Customisation required due to variations from the Standard Approach) - Variations refer to situations where certain level of automation is already in place at the banks-end and would therefore require customisation of the existing systems to achieve total automation. In other words such customisation would mean carrying out changes and modifications to the existing architecture with respect to the technology and processes dimensions with a view to reach the common end state. 5.1 The Standard Approach Overview 5.1.1 The high level schema for the proposed approach is represented in Figure 4. The approach comprises of four logical steps. Each of the steps is further subdivided into activities. The activities are further broken down into the tasks required to complete the activity.

Figure 4: Approach Design The four steps involved in the standard approach for automation of data flow would involve building of the following layers as illustrated below:

Figure 5: Steps to automate data submission process 5.1.2 Each of these steps is discussed below along with activities required to achieve the objective underlying each step. The figure below lists a few illustrative activities involved in the four steps. Further the activities are classified into tasks and sub-tasks as given in Annexure B.

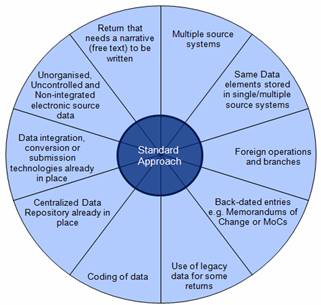

Figure 6: Illustrative steps and activities to be followed in the Standard Approach 5.1.2.1 Building Data Acquisition Layer: This step focuses on building the source data. This will ensure availability and quality of the data in the source systems of the banks. The activities identified under this step are detailed below. a) Ensure Data Capture: The data components required to be submitted in the returns are mapped to the data elements in the source systems of the acquisition layer. The components which cannot be mapped need to be identified so that the source system can be enhanced accordingly. This activity can be further broken down into tasks as discussed in Annexure B. b) Ensure Data Quality: Data quality is ensured by improving the data entry processes and by introducing post entry data validation checks. This activity can be further broken down into tasks as discussed in Annexure B. c) Ensure Data Timeliness: The availability of data elements may be matched with the frequency prescribed by Reserve Bank for the relative returns. This activity can be further broken down into tasks as discussed in Annexure B. 5.1.2.2 Building Data Integration & Storage Layer: The source data from the Data Acquisition layer may be extracted, integrated and stored in the CDR. This repository would be the single source of information for all returns. This step outlines the activities and tasks to be performed to build this layer. The activities identified under this step are detailed below: a) Build a common master data framework - Master data consists of information about customer, products, branches etc. Such information is used across multiple business process and is therefore configured in multiple source systems of the bank. As part of this activity, the inconsistencies observed in capturing this master data are studied to ensure building of a common master data. This activity can be further broken down into tasks as discussed in Annexure B. b) Build a common metadata framework: Metadata is information extracted from the data elements from the functional and technical perspective. The tasks required to build the common metadata framework are detailed in Annexure B. c) Define a standard data structure for storage: The CDR stores bank-wide data required for preparation and submission of returns. The flow of information from Source systems to the CDR will require a well defined data structure. The data structure may be based on the master data and metadata framework built in first two activities. This activity can be further broken into the tasks as given in Annexure B. d) Ensure data is stored in Centralized Data Repository: Data from the source systems would be stored in the Centralized Data Repository. The stored data would be integrated on the basis of well defined business rules to ensure accuracy. This would involve initial as well as incremental uploading of data on a periodic basis. This activity can be broken into tasks as given in Annexure B. 5.1.2.3 Build Data Conversion Layer: The Data Conversion Layer transforms the data into the prescribed format. This layer is an interface between data storage layer and submission layer. The activities identified under this step are detailed below: a) Mapping of prescribed data with repository data -To prepare the required return, it is essential to ensure mapping of prescribed data with the corresponding structures in the CDR. This activity can be broken into tasks as given in Annexure B. b) Design the business logic for mapping and validation: As the data available in the CDR will not be in the same structure and format as prescribed, business logic will need to be defined for this conversion. Since data conversion layer is the final layer where the data transformations take place before submission, the business logic will also include data validation rules. The data validation rules will include basic data checks, format validations, consistency validations, abnormal data variations and reconciliation checks. This activity can be broken into tasks as given in Annexure B. c) Availability of infrastructure: Successful implementation of business logic would depend upon availability of suitable infrastructure. This activity can be broken into tasks as given in Annexure B. 5.1.2.4 Build Data Submission Layer: The systems and codes in this layer would have the capability to authorise the data flow into the Reserve Bank’s systems. This layer will also have the ability to receive messages and information from the Reserve Bank systems. The Data Submission layer would certify that the data submitted to Reserve Bank is reliable and generated using automated system. The activities identified under this step are detailed below: a) Adhering to the calendar of returns-Based on the frequency of submission of returns, this activity would generate a detailed calendar with reminders and follow-ups. This activity can be broken into tasks as given in Annexure B. b) Tracking mechanism for return submission-This activity provides for a mechanism to track the submission of returns and generate status reports. This activity can be broken into tasks as given in Annexure B. c) Provision for feedback from Reserve Bank systems-Under this activity, a mechanism would be developed to receive feedback to act as a trigger for further action. This activity can be broken into tasks as given in Annexure B. d) Provision for generation of certificate -Under this activity, the banks may be able to certify that the return submission is fully automated with no manual intervention. This activity can be broken into tasks as given in Annexure B. 5.2. Variations to the Approach The standard approach would be customized by banks on the basis of the current state of technology. These customization cases are called variations of which. A few illustrative examples have been discussed in Figure 7 below:

Figure 7: Variation to Standard Approach The details of the variations are as follows: 5.2.1 Multiple source systems: For data residing in multiple source systems, there would be a need for integration of data. In such cases, customization of the standard approach would be needed at the time of developing a CDR. a) A detailed mapping of both master and transactional data, wherever applicable, may be carried out across all the source systems. This mapping may be at the same level of granularity. The common elements across both these systems must be mapped to understand the consolidation process. b) The metadata and master data framework would need to be designed keeping in mind the sharing of source system data across multiple systems. c) The integration of data across the source systems would continue to take place through the Data Integration & Storage layer and the integrated data would be available in the CDR. 5.2.2 Same Data elements stored in single/multiple source systems: Generally, each data element may be stored in a single and definitive source system. However, there would be instances of same data elements being stored in multiple source systems. It may also be possible that within the same system there may be multiple modules and data flows from one module to another. In such cases, there is a need to identify the appropriate source system from where the data element has to be taken for further processing. The alternatives to be followed for such a scenario could be:

For master data, there may be instances where different attributes for the master data will be sourced from different systems. Therefore the source system with enriched data, highest data quality with latest updates may be used. There may be instances of duplicate source of data within the same system or module. In such cases, data from the most appropriate source may be taken. 5.2.3 Foreign operations and branches: The standard approach assumes that the bank is operating only in India and hence has a common set of business and operational guidelines under which it operates. However, banks with foreign operations will have to follow different set of guidelines. The local nuances and business environment may warrant different business practices. In such cases, design of the CDR as well as the Data Integration & Storage layer will have additional considerations and corresponding activities and tasks. The key considerations and corresponding activities for this variation are discussed below:

5.2.4 Back-dated entries e.g. Memoranda of Change or MoCs: MoCs are given affect by making changes in the financial statements. . Back dated entries are required to be made in the source systems to incorporate these changes, which is a challenge in the context of automated data flow. This can be handled by designing an appropriate module which will integrate the MoCs and generate a revised GL for further processing. 5.2.5 Use of legacy data for some returns: In some cases, legacy data may be required for submission of returns for which it may be necessary to store the same in the CDR. This data is static and is typically stored in tapes or maintained in physical form in registers. In such a case, the CDR may be enhanced for capturing such legacy data. 5.2.6 Coding of data: Coding and mapping of master and transactional data would be required for some of the returns to synchronise it with the codes prescribed by Reserve Bank e.g. BSR coding, sector coding for Priority sector returns, etc. This can be done either by updating the source systems or building the same outside the source systems. 5.2.7 Centralized Data Repository: If a bank already has a centralized data repository in place, then the same may be leveraged for achieving automated data flow to Reserve Bank. In cases where data is partially available in the CDR, the bank may enhance the integration layer for capturing the relevant data required for submission to Reserve Bank. 5.2.8 Data integration, conversion/submission technologies: Banks may choose to leverage on the investment already made in technologies while building the various layers as prescribed in the end state architecture, rather than procuring new technology. 5.2.9 Unorganised, Uncontrolled and Non-integrated electronic source data: It may be possible that a bank may be using desktop-based or standalone technology tools e.g. spread sheet, etc. for storage of certain source data. While this data may be in electronic form, it is dispersed across the bank. Therefore, there is no control on addition, deletion or updation of this data and no audit trails are available to track this data. As this data is not organised and reliable, it cannot be used for the automated data flow to Reserve Bank. In such cases, the data may be brought under a controlled mechanism or be included in the source system. 5.2.10 Return that needs a narrative (free text) to be written: Some of the returns may require a narrative to be written by the bank before submission. Such narratives are not captured in any source system and are required to be written during the preparation of the returns. In such cases a separate system can be developed where the user can enter all the narratives required for the returns. These narratives will be stored in the central repository. The Data conversion layer while generating the returns will include these narratives in the appropriate returns. Storing the narratives in the central repository will ensure that the complete return can be regenerated automatically as and when required. Conclusion Banks may carry out a self-assessment, based on the Technology & Process dimensions and place itself appropriately in one of the prescribed clusters. The banks can then follow the standard approach by applying variations, if any, for achieving the end state. 6.1 Due to varied levels of computerisation in banks as also due to a large number of returns to be submitted by them, it is necessary to plan and execute the steps for achieving automated data flow between banks and Reserve Bank in a time-bound manner. To achieve this objective, it is important for banks to carry out a thorough assessment of their current state of computerisation, through a prescribed methodology. This would make it possible for banks to place themselves in different clusters, as has been illustrated in Annexure A. Simultaneously, the returns required to be submitted by banks to Reserve Bank, would be categorised into five broad groups. 6.2 Based on a quick study made on eight banks, maximum time-lines for achieving automation have been estimated for different clusters of banks for each group of returns. They are indicated in Table below.

Table 1: Timelines for achieving the end-state of automated data flow from banks 6.3 To begin with, a common-end state would be achieved when a bank is able to ensure automated data flow to Reserve Bank for four out of the five groups of return (Simple, Medium, Complex I and Complex II). It may not be possible for the Banks to achieve complete automation for the returns falling in the fifth group viz. “Others” as data required for these returns may not be captured in IT Systems. However, it is envisaged that in due course, this group would also be covered under the automated dataflow. 6.4 Incidentally, as a collateral benefit of automation, the banks would be able to channelize their resources efficiently and minimize the risks associated with manual submission of data. 6.5 The proposed Roadmap comprises of the following-: 6.5.1 Returns Classification Framework As mentioned above, the returns currently submitted by the banks to Reserve Bank, have been classified into five broad groups on the basis of the feedback provided by eight sample banks by adopting a Moderate approach. Each return was assigned to the group which was chosen by majority of banks (refer to the Annexure C for the detailed Returns Classification on 171 representative set of returns). Each of these groups of return can be considered for automation individually without having an adverse impact on the other returns. 6.5.2 Implementation Strategy Due consideration has been given to the different clusters of banks and the different categories of returns to ensure that the bank has flexibility in implementing the approach based on their current state without compromising on the overall vision of automating the entire process of submission of returns to Reserve Bank. The suggested timelines have been given in ranges to factor in differences across banks within a cluster. 6.5.3 Key Challenges The banks might face following challenges on account of converting to a fully automated state of submission: (a) The data required to prepare the returns might be captured in more than one source application. Hence all the source systems must be integrated prior to submission of the returns through complete automation. (b) Currently MoCs are given effect outside the core applications; hence this process will need to be integrated into this solution. (c) The data transformations and business rules are not well documented; hence prior to undertaking the automation project, it might be necessary for banks to prepare a detailed process documentation to capture this information. (d) Legacy data will need to be corrected for mapping to the Reserve Bank published codes and definitions. (e) Data granularity will need to be standardized across the source systems. Conclusion The roadmap enables the bank to take a phase wise approach to achieve the end state. The bank can decide to break the above defined return groups into smaller groups. These sub-groups can then be implemented either in a sequential manner or in parallel depending on the ability of the bank to deploy the requisite resources. However, care must be taken to ensure that the overall time lines are adhered to. 7.1 An automated data flow from the IT systems of banks to Reserve Bank with no manual intervention will significantly enhance the quality and timeliness of data. This will benefit the Indian banking sector by enabling more informed policy decisions and better regulation. Over and above the regulatory benefits, there will be many other benefits in disguise to the internal operations, efficiency and management of banks. This can be understood by taking a closer look at the different layers of the end-state given in chapter on common end state. 7.2 Firstly, the data acquisition layer will ensure higher data quality and higher coverage of source data by the systems in electronic form. This will eliminate any inefficiency in the operational processes of the bank as most of the processes can be automated using systems. Secondly, major benefits will be derived from the harmonized metadata in the bank at the data integration & storage layer. This will allow for smooth communication and lesser data mismatches within the bank which often take place due to difference in definitions across departments. Thirdly, the centralized data repository will have a wealth of data that can be easily leveraged by the bank for internal reporting purposes. This not only saves major investment towards a separate reporting infrastructure but also provides management of the banks with recent data of high quality for decision support. Last but not the least, the automated flow of data from banks will have significant benefits in costs and efficiency of the returns submission process itself. The automated flow of data will ensure a smooth process with minimal delays in submission of data that is of much higher quality. 7.3 The realization of the above benefits will accrue to the bank when the automation of data flow is accomplished and the final automated end-state has been reached. The end-state has a layer-by-layer flow of data from the place where it is generated to the central repository and finally to Reserve Bank. To achieve the end-state the banks need to use the constituents of the paper in an integrated manner as given below: a) Banks need to carry out a current state assessment across the various technology and process parameters defined in chapter on Assessment Framework. This will help the bank identify the cluster that it falls in. b) Banks need to study the proposed roadmap. Banks need to take one return group at a time and study the approach provided in chapter on approach for banks. c) While studying the approach, banks need to customize the approach based on the return group, variations applicable to the bank and also on the business model and technology landscape of the bank. d) A further fine tuning of the approach can be done by carrying out the assessment separately for different return groups and not for the bank as a whole. Annexure A – Assessment Framework – Assessment Framework – Parameters, scoring matrix and guidelines The parameters and guidelines for conducting self assessment on technology and process dimensions are as defined below: 1(a) Parameters and guidelines for Technology dimension:

1 (b) Parameters and guidelines for Process dimension:

1 (c) Self Assessment using the Excel Model The banks will need to conduct a self assessment using an excel model. The bank must evaluate themselves on their Technology and Process Maturity based on the parameters defined above and assigns a rating of High, Medium or Low based on their evaluation. The response must be populated along with the rationale in the “Technology Maturity” and “Process Maturity” worksheets. The overall maturity score will be automatically calculated using the embedded logic within the worksheet. Click here to view the Excel Model for banks. The Technology maturity score is on a scale of 0-1 and hence 3 bands of 0-0.33 (Low), 0.33-067 (Medium), 0.67-1 (High) are defined. Similarly the Process maturity score is on a scale of 0-1 and hence 2 bands of 0-0.5 (Low), 0.5-1 (High) are defined. 2. Sample Assessment A Sample Assessment for one of the bank is illustrated below as reference: 2(a) Technology Dimension:

2(b) Process Dimension:

Thus as per the maturity scores, on the process v/s technology maturity grid, the bank is classified as follows:

Figure 8 : Current maturity based classification of the sample bank based bank Annexure B Task Details for the standard approach This chapter provides the task and sub-task (if applicable) level details of the approach provided in Approach for banks. The high level schema for the proposed approach is represented below in Figure 12.The entire approach is constructed in a hierarchical manner with overall approach comprised of four steps. Each of the steps is further subdivided into activities with each of the activity defined as multiple micro level tasks and each task further broken down to sub-tasks, wherever applicable.

Each of these steps is discussed above in chapter on approach for banks along with the constituent activities. The detailed level tasks and sub-tasks are given in the four Annexures– B1, B2, B3 and B4. On completion of the tasks and sub-tasks, an illustrative approach for a bank to reach the end-state has been provided in Annexure B5. Annexure B1 1. Prepare Data Acquisition layer: The task level details for this step are defined under the activities listed below: 1(a) Ensure required data is captured: This activity can be further broken down into 6 major tasks:

Figure 10: Prepare Data Acquisition – Ensure Required Data is captured

• Identify the enhancements required to capture the missing elements against each identified gap. Filling a gap may be done by:

• The identified enhancements will be logically grouped based on similar characteristics for the purpose of implementation. Depending on the system enhancement required, there might also be a need to modify and/or introduce new data capture processes. • The historical data is migrated into the enhanced system. The quantum of data migrated must ensure that all requirements as per the Reserve Bank return formats are satisfied. For reasons of consistency, comprehensiveness or analysis, the bank may choose to update the data in full. 1(b) Ensure Data Quality: The tasks defined below need to be performed to ensure data quality of the source data:

Figure 11: Prepare Data Acquisition – Ensure Data Quality • Identify the points of capture of the data and the processes at each of these points of capture where the data quality gets impacted • Identify the most common types of errors being committed at the data capture location e.g. always taking the first item in drop down, always providing a standard value for a mandatory item as the same is not available for entry, etc. • Analyze and finalize solutions for addressing each of the data quality issues identified above. This may include mechanisms both in terms of systems and processes like (this is a sample list and not exhaustive)

• A separate data quality enhancement drive may be undertaken, to augment the quality of the historical data. This may include (this list is a sample and not exhaustive)

1 (c) Ensure Data Timeliness: The tasks defined below need to be performed to ensure data timeliness:

Figure 12: Prepare Data Acquisition – Ensure Data Timeliness

Annexure B2 – Task Details – 1. Prepare Data Integration & Storage layer The task level details for this step are defined under the activities listed below: 1(a) Build a common master data framework - The tasks defined below need to be performed to build the common master data framework:

Figure 13: Prepare Data Integration& Storage Layer – Build a common Metadata Framework

1(b) Build a common metadata framework: The tasks defined below need to be performed to build the common metadata framework:

Figure 14: Prepare Data Integration& Storage Layer – Build a common Master Date Framework

1 (c) Define a standard data structure for storage: The tasks defined below need to be performed to define the standard data structure for storage:

Figure 15: Prepare Data Integration& Storage Layer – Define a standard Data Structure

1(d) Ensure data is loaded to centralized data repository: This has two main aspects (A) First time loading of data and (B) Incremental loading of data on a periodic basis. The tasks defined below need to be performed for the first time loading of data:

Annexure B3 – Task Details -“Prepare Data Conversion Layer” 1. Prepare Data Conversion Layer The task level details for this step are defined under the activities listed below 1(a) Map target data to repository data structure- The tasks defined below need to be performed to build the mapping of target data to source data:

Figure 17: Prepare Data Conversion Layer–Map target data to repository data structure 1(b) Design the business logic for mapping and validation: The tasks defined below need to be performed to design the business logic for conversion:

Figure 18: Prepare Data Conversion Layer –Define the Business logic for mapping and Validations

1(c) Implement the business logic: The tasks defined below need to be performed to implement the business logic:

Figure 19: Prepare Data Conversion Layer – Implement the Business Logic

Annexure B4- Task Details - “Prepare Data Submission Layer” 1. Prepare Data Submission layer The task level details for this step are defined under the activities below. 1 (a) Prepare and Implement the calendar of returns submission - The tasks defined to prepare and implement the calendar of returns are:

Figure 20: Prepare Data Submission Layer – Prepare and Implement the Calendar for Returns Submission

1(b) Build the return submission tracking mechanism. The tasks defined for building the tracking mechanism are:

Figure 21 : Prepare Data Submission Layer – Build the return submission tracking mechanism

1(c) Build provision for receiving and interpreting feedback from Reserve Bank systems. The tasks defined to build provision for receiving and interpreting feedback from Reserve Bank are:

Figure 22: Prepare Data Submission Layer – Build provision to receive feedback from Reserve Bank

1(d) Build provision for generation of certificate: The tasks defined to build provision for generation of certificate are:

Figure 83: Prepare Data Submission Layer – Build provision for generation of certificate

Annexure B5 – Illustrative Approach for a bank 1. Introduction to the current state of the bank The bank is a scheduled commercial bank with pan India presence in terms of branches, ATMs, regional and zonal offices. All the Bank’s branches are live on the Core Banking Solution. The bank has foreign operations and foreign branches in addition to their domestic operations. Apart from core banking solution, the bank also has other technology based applications for treasury (front and back office). The bank is currently in the process of implementing an Enterprise Data Warehouse (EDW). CBS data is also loaded into a legacy credit application. Though the data is available centrally in the core banking solution, the data extract from the CBS is sent to the Branches for auditing and preparation in the desired format, prior to submission. Most of the departments within the Bank manually key in the data into the Reserve Bank applications for submitting the returns. 2. Assumptions

3. Approach: The approach for the sample bank to traverse from its current state to the common end state of complete automation of returns is defined as per the standard approach and variations covered in chapter on approach for banks.

The key steps and the activities to be undertaken by the bank to become automated are as defined below: Step 1 : Prepare Data Acquisition Layer: The data elements that are not captured or stored in any source system will be brought under a controllable defined IT system which then would be added into the data acquisition layer. The key activities that the banks need to do are as follows: (a) The bank needs to conduct a mapping exercise between Reserve Bank reporting requirements and the data being captured across the different source systems available in the bank. Step 2 : Prepare Data Integration & Storage layer: This step will ensure that the Centralized Data Repository serves as the single source for preparing all Reserve Bank returns. The key activities for performing this step are as follows: (a) Conduct a data profiling exercise on the transactional data and identify priority cleansing areas. The data will be cleansed prior to loading into the repository. Multiple iterations might be required to completely cleanse the historical data. (b) A one-time exercise must be conducted to synchronize the data between the credit application and the CBS to ensure consistency of legacy data. All changes applied to the credit application must be replicated in the CBS using a bulk upload facility. Henceforth the credit application will be synchronized with the core banking system on an on-going basis at a specified frequency. The bank must make a policy decision to not allow any changes to the data being uploaded into the credit application by the branch personnel. Data for the Centralized Data Repository will be sourced from the core banking solution. (c) Harmonize the metadata definitions to aid the common understanding of definitions and data across the bank. The definitions need to be collected from various sources like internal system documents, Reserve Bank circulars, tacit knowledge, policy documents, bank’s manuals etc. A central metadata repository will be used to store this data. All applications would have access to this repository. (d) Define the business rules to integrate the data across the different systems. Wherever, data resides in more than one system, the most recently updated record will be considered for loading into the repository, subject to the metadata being same. (e) All MoCs will be identified and an application created to store these MoCs. This application will also be considered as a source system under the data acquisition layer. (f) Identify the master data entities and their attributes to define a master data model. Integrate the attributes of master data entities across different source systems and link the transactional data to the new integrated master data. (g) Define a flexible and agile data model for EDW by considering the Reserve Bank’s regulatory requirement and metadata and master data frameworks. (h) Define the storage mechanism of centralized data repository in accordance with the data model. (i) The timestamps for worldwide operations may be marked as per IST while loading the data so as to ensure that common cut-off is taken for all data irrespective of the time zone. (j) Define appropriate operational parameters to make the repository functional by identifying initial data loading schedule, incremental data loading schedule, data retention, archival and data security guidelines. Step 3 : Prepare data conversion layer (a) Conduct mapping of data required by the Reserve Bank to the Centralized Data Repository and define the logic and formats required to prepare the Reserve Bank returns. (b) Implement the data conversion layer using a tool or customized scripts. (c) Generate the previous period returns submitted by the bank using the new system. This is to test whether the logic has been correctly defined. Step 4 : Prepare data submission layer (a) Do a test submission of the prepared returns to Reserve Bank’s returns receiving system. (b) Implement a tracking system that allows defining the submission calendar and can track the return submission status. (c) Define event triggers based on possible response codes to be received from Reserve Bank for tracking purposes. (d) Conduct a process and system audit at the end of the implementation to ensure that the data being reported to Reserve Bank is as per the Reserve Bank guidelines for automation. (e) Cut-over to the new automated submission process for submitting the identified set of returns to Reserve Bank. (f) The bank will also need to provide a certificate to Reserve Bank declaring that the return group was generated using automation with no manual intervention. (g) For the remaining returns, the bank continues with the earlier process of submitting the data to Reserve Bank. After completion of this project the bank undertakes the second group of returns. The activities required for this group will be the same as defined above for the first group. Annexure C – Representative Returns Classification Click here to view the Returns Classification Excel Appendix I – Other End State components, Technology Considerations and Definitions Data Quality Management may involve following activities: (a) Data Profiling: is a systematic exercise to gather actionable and measurable information about the quality of data. Typical Data profiling statistics include specific statistical parameters such as - Number of nulls, Outliers, Number of data items violating the data-type, Number of distinct values stored, Distribution patterns for the data, etc. Information gathered from data profiling determines the overall health of the data and indicates the data elements which require immediate attention. (b) Data Cleansing: process may be enabled for detecting and correcting erroneous data and data anomalies prior to loading data in the repository. Data cleansing may take place in real-time using automated tools or in batch as part of a periodic data cleansing initiative. Data Cleansing is done by applying pre-defined business rules and patterns to the data. Standard dictionaries such as Name matching, Address Matching, Area – Pin code mapping, etc. can also be used. (c) Data Monitoring: is the automated and/or manual processes used to continuously evaluate the condition of the bank’s data. A rigorous data monitoring procedure may be enabled at banks to handle the monitoring of data quality. Based on the data monitoring reports, corrective actions will be taken to cleanse the data. Data Privacy and security is an essential part of the bank’s end state vision so as to prevent any unauthorized access, modification or destruction of sensitive data. The security needs to be ensured across the solution at various levels: (a) Network Security: This is designed to act as a checkpoint between the internal network of the bank and the Reserve Bank’s network(s). The data must be transmitted using a secure, encrypted format to ensure there is no interception of data. (b) Application security: This provides the ability to the administrator to access the Centralized Data Repository on the banks’ side and limit the access to the authorized users only. There may be appropriate log of activity to ensure that details like user-id, time of log in, data elements viewed etc. are captured. (c) Database security: This forms a security layer around the Centralized Data Repository so as to control and monitor access, update rights and for deletion of data held within the database. (d) Workstation Security: Workstation security is done through the usage of solutions like anti-virus protection, screen saver passwords and policies around installation of personal software and internet access. The data organizational structure and setup of governance processes that manage and control the return submission process may be clearly defined and documented as part of the overall data governance policy within the bank. This helps in communicating the standard procedures to all stakeholders effectively. The key constituents of a data governance model that the bank needs to put in place are: (a) Clearly defined roles and responsibilities across all the departments involved in the returns submission process. (b) Clear accountability may be put in place by defining data ownerships and process ownerships across the departments and at each layer in the process. (c) Key metrics e.g. - number of instances of data validation failures at Data Validation Layer may be defined, recorded and tracked. (d) Clear decision-making guidelines and protocols, escalation process for decision resolution procedures may be put in place. (e) Open sharing of governance information i.e. governance process models and definitions may be available to anyone in the overall governance organization who needs them. The data governance group for the Returns submission process at the bank’s end must consist of members from the IT function and the compliance department and each of the main business groups owning the data within the bank.

Figure 24: Model data governance structure for banks From the Reserve Bank perspective the governance model may define the following: (a) As far as possible, there may be a single point of contact, clearly identified by the bank for communication with Reserve Bank for returns related issues. In case of multiple points of contact, the segregation of responsibilities for each point of contact may be clearly defined and may be in-line with the principles defined in this section. Banks also need to provide justification for having multiple points of contact and why single contact will not suffice. (b) There may be a well defined escalation matrix for each point of contact defined by the bank. The escalation matrix may lead up to the ultimate authority at the banks’ end with no exceptions. (c) The data governance organization defines the basis on which the ownerships of data and information will be segregated across the bank. While there can be numerous models for the same, the three typical models are – Process Based, Subject Areas Based and Region Based. (a) Process based model defines data ownership for each layer in the process separately – whereby the ownership for same data at data acquisition layer and data submission layer will reside with different owners. (b) Business Function based model defines data ownership based on the data subject area e.g. foreign exchange data, Priority sector data etc. (c) Region Based model defines data ownership based on the regions e.g. North Zone data, South Zone data etc. Given the nature of regulatory information and the process it is recommended that the data ownership may be primarily based on the business function. Based on the size, while some banks may need to also have a layer of regional ownership, the eventual model may be subject area based. Detailed audit trails must be captured to cover the entire submission process. The audit trail must provide the ability to re-create the return if required in a controlled manner and also offer itself to detailed audit functions. The key element to be captured by the audit trail must include: (a) Source of the Data The audit trail can either be maintained using a monitoring tool or a standard operating process documentation which defines all the details required for audit purposes. There is a need to define a change management process to manage and maintain the automated data flow architecture. While change management is a continuous process, some possible change management scenarios that could occur for the Automated Data Flow process are as mentioned below: 5.1 Modification in existing return owing to:

5.2 Modification in the source system:

An acknowledgement will be generated by Reserve Bank once the data is successfully received and validated by Reserve Bank. The acknowledgement can be in the form of an e-mail sent to the respective banks or as per a mutually agreed information exchange format. If there is an error in either the validation or receipt of data by Reserve Bank, an error message will be sent to the concerned bank. The message shall indicate the type of error and the error details. The corrective action will be driven through systems and processes within the bank, to find out the cause of the exception and take appropriate remedial action. 7. Data Retention and Archival The data archival policy may be defined in line with regulatory guidelines as well as the internal policy of the bank, e.g. if the bank has its internal policy to retain the treasury data for five years while Reserve Bank requires a seven year data then the retention period may be at least seven years. (a) Metadata is the means for inventorying and managing the business and technical data assets. Metadata plays a critical role in understanding the data architecture for the overall system and the data structures for individual data elements. It also enables effective administration, change control, and distribution of information about the information technology environment. (b) The metadata across all the individual applications must be collated using a centralized metadata repository. The metadata to be captured across the different applications must be standardized. This is to ensure the same unique characteristics are captured and checked for consistency across the applications. (c) The metadata (data definitions) may be synchronized across various source systems and also with the Reserve Bank definitions. This is important to ensure that all transformations have been correctly applied to the data as per the Reserve Bank definitions. Master data is the consistent and uniform set of identifiers and extended attributes that describe the core entities of the bank. Some examples of core entities are parties (customers, employees, associate banks, etc), places (branch locations, zonal offices, regions or geographies of operations, etc.) and objects (accounts, assets, policies, products or services). Master data management essentially reduces data redundancy and inconsistencies while enhancing business efficiencies. The essential components of master data management are as follows: (a) Defining Master Data: Using the data available in the different applications a unique master record is generated. This record can consist of elements from different systems, without any duplication of information. (b) Creating Master Data: Once the elements forming the unique record for the particular data entity are identified the source mapping document is prepared. Wherever the master data is available in more than one source application, the element which is most accurate and recent must be considered for the master record formation. (c) The storage, archival and removal of Master data may be in compliance with the guidelines provided in the Data Retention and Archival Policy. 10. Technology Considerations for the End State 10.1 Data Acquisition Layer – Comprises of all the source systems which capture the data within the bank such as the Core Banking Solution, Treasury Application, Trade Finance Application and any other systems used by the bank to capture transactional, master, and /or reference data. 10.2 Data Integration & Storage Layer- 10.2.1 Data Integration - The data integration can be done either by using an ETL (Extract-Transact-Load) tool or custom developed scripts or a middleware application.

10.2.2 Data Storage - Data storage is a defined repository for the data. The data can be stored using an Operational Data Store, Data Mart or a Data Warehouse.

10.3 Data Conversion Layer - The data conversion process to convert the bank’s data in the format specified by Reserve Bank can be achieved using standard reporting formats like XBRL, XML, Excel based files or flat files. This layer can be developed either using data conversion tools available in the market or customized scripts. These scripts must be developed to ensure appropriate application of the business logic required for generating the returns, perform appropriate validations and convert the data in the specified format. There are several applications available in the market which would allow conversion of data from the bank’s internal format the XBRL or XML formats. The conversion solutions can be implemented using either client-server approach or as a series of services using service oriented architecture (SOA). Owing to the varied nature of the return formats, it might be found that no single solution satisfies all requirements. In such a case a mix of custom developed scripts and readily available tools might be required to develop this layer. 10.4 Data Submission Layer - The data submission from the banks to Reserve Bank can be achieved using web based submission systems such as a secure web portal where the data can be uploaded directly or by using a batch loading (FTP) process, template based web page entries loading (HTTP), and custom developed Web Services. The submission process can be triggered automatically using a scheduler. Data submission can be designed to support either “push” or “pull” mechanisms. If the data submission is initiated by the bank then it is considered to be a “Push”. In a “Pull” mechanism the submission process is initiated by Reserve Bank. 10.5 Data Validation Layer - A business rules engine can be used to do the data validation on the Reserve Bank side. Also, a custom built script can be developed to do the validation instead of using the business rules engine. (a) Security - Generally available, database management systems allow for defining role based access to the data. Along with access control, additional security measures in the form of data encryption, identity management can be used to ensure there is no unauthorized access to the data. Data security may also be maintained whilst transmitting the data to Reserve Bank. (b) Metadata – Metadata describes other data. It provides information about a certain data element’s content. For e.g. the metadata for Account balance can be range of valid values, data type, currency used etc. (c) Metadata Management - Metadata can be maintained using either the Open Information Model (OIM) or the Common Warehouse Meta model (CWM) depending on the overall architecture prevalent in the bank. The standard that has gained industry acceptance and has been implemented by numerous vendors is the Common Warehouse Meta model. The metadata management tool can be sourced as a separate package or can be part of the integrated suite of data integration and warehouse solutions. The metadata repository may be stored in a physical location or may be a virtual database, in which metadata is federated from separate sources (d) Data Quality Management - Data Quality Management can be done either using a packaged tool or using custom developed scripts. Though custom developed scripts are cheaper and more flexible than a packaged tool. However, scripts are not very often preferred as they take longer to develop and are not easy to maintain on an on-going basis. The standard tools available in the market have pre-defined dictionaries which allow automated tool based profiling, cleansing and standardisation with minimal manual intervention. (e) Reporting Tools - Reporting tools can be used by the bank to prepare the returns in the format desired by Reserve Bank. These tools provide the flexibility to do both standard reporting, i.e. where formats are pre-defined as well ad-hoc reporting, i.e. where format is defined by the user on the fly. In addition to allowing the user to create the report for internal consumption, the tools also provide for the ability to create external reports in XBRL or SDMX formats. The tools also provide facilities to export the reports in various formats such as: PDF, Microsoft Office Word format (.doc, .docx), Microsoft Office Excel format (.xls, .xlsx), Web page based reporting, etc. (a) Atomicity – Atomicity is the measure of granularity. Data which cannot be further broken down into smaller components is known as atomic data. (b) Backdated entries in accounts – These are entries in accounts that are made effective from an earlier date. These changes are generally required after an audit is done. For e.g. if an audit done on August 26th recommends a change in one of the entries for July 25th, such a change will be termed as a backdated entry. (c) Centralized Data Repository – Refers to a repository of enterprise-wide data as required for preparing the returns to be submitted to Reserve Bank. (d) Complete Automation – Is defined as no manual interventions required from the point of capture of data within the core system to the submission of the return to Reserve Bank. (e) Data Granularity – Is defined as the level of detail of the data. Higher the granularity, deeper the level of detail. For e.g. a repository that stores daily account balances is more granular than a repository that stores monthly account balances. (f) IT System / Core Operational System - The system refers to a technology based solution that supports collection, storage, modification and retrieval of transactional data within the Bank. (g) People Dimension – This refers to the human resources aspect of the returns generation process which includes availability of resources, the roles and responsibilities of people involved, their skills and training. (h) Process Dimension – This refers to the procedures and steps followed in the returns generation process. This will also cover the validation and checking done on the returns generated and review mechanism followed before submitting the return. It also includes the mechanism for submitting returns to Reserve Bank and receiving feedback or answering queries from Reserve Bank. (i) Technology Dimension – This refers to all the IT systems used or required for the entire returns generation and submission process. It includes the systems required for collecting data, processing it and submitting the return. Appendix II – Global Case Study Banking - FDIC Call Report, CEBS 1. Many regulators across the world share some common challenges in their reporting functions owing to the nature of their requirements. Some of the most common ones are as defined below:

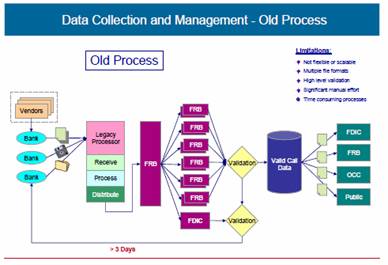

Regulators in the banking sector in the United States of America recognized these challenges and undertook a modernization project to overcome them. Members of the Federal Financial Institutions Examination Council (FFIEC), the Federal Deposit Insurance Corporation (FDIC), the Federal Reserve System (FRS), and the Office of the Comptroller of the Currency (OCC) sought to resolve these challenges through a large-scale deployment of XBRL solutions in its quarterly bank Call Report process. In addition, through the modernization project, the FFIEC also sought to improve its in-house business processes. 2. Legacy Data Collection Process –

Figure 27 The FDIC was responsible for validating data of approximately 7,000 financial institutions, and used a centralized process at its Washington, DC headquarters. Historically, the agencies exchanged data continuously to ensure that each had the most recent data that had been validated by the responsible agency. Each agency maintained a complete set of all Call Report data regardless of the agency responsible for the individual reporting institution. In addition to reporting current data quarterly, institutions were also required to amend any previous Call Report data submitted within the past five years as per the requirement. Amendments submitted electronically were collected by means of the process described above. Often the institution contacted the agency, and the agency manually entered only the changes to the data. The validation and processing of Call Report amendments were similar to those for original submissions. But, in this case an agency analyst reviewed all amendments before replacing a financial institution’s previously submitted report. Amendments transmitted by the institutions using Call Report preparation software always contained a full set of reported data for that institution. Once the data was collected from all the respondents and validated by the agencies, the data was made available to outside agencies and to the public. 3. Technology Used in Automation Project The Call Agencies relied on the “Old Process” for decades, introducing enhancements in piecemeal fashion. The Call Modernization project sought to reinvent and modernize the entire process in order to make it more useful for the regulatory community and its stakeholders. At the same time, it aimed to provide a relatively neutral transparent change to financial institutions. Early in the project, Call Report preparation software vendors were invited to participate in a roundtable discussion of reporting requirements and practices with an eye towards finding ways to improve it. Based on the findings of those discussions, the FFIEC identified areas to target for improvement in undertaking an inter-agency effort to modernize and improve the legacy process. It was decided that the FFIEC may continue to provide data collection requirements that include item definitions, validation standards, and other technical data processing standards for the banking institutions and the industry. The banking institutions would continue to utilize software provided by vendors or use their own software to compile the required data. The updated software would provide automated error checking and quality assessment checks based on the FFIEC’s editing requirements. The editing requirements would have to be met before the respondent could transmit the data. Thus, all the data submitted would have to pass all validity requirements, or provide an explanation for exceptions. The regulatory agencies believed that quality checks built into the vendor software may play a key role in enhancing the quality and timeliness of the data. Placing the emphasis on validating the Call Report data prior to submission was deemed more efficient than dealing with data anomalies after submission. The FFIEC was interested in exploring the use of a central data repository as the “system of record” for Call Report data. The data would be sent using a secure transmission network. Potentially, a central data repository would be shared among the regulatory agencies, and possibly with the respondents, as the authentic source of information. Once the central data repository received data, a verification of receipt would be sent to the respondent confirming the receipt. If a discrepancy was discovered in the data, online corrections would be made in the Centralized Data Repository directly by the respondent or by the regulatory agencies during their review.

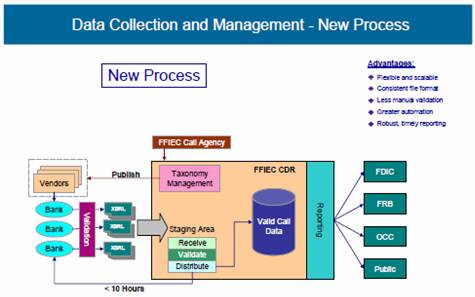

Figure 28: The new system, known as the Central Data Repository (CDR), is the first in the U.S. to employ XBRL on a large scale and represents the largest use of the standard worldwide. The CDR uses XBRL to improve the transparency and accuracy of the financial reporting process by adding descriptive “tags” to each data element. The overall result has been that high-quality data collected from the approximately 8,200 U.S. banks required to file Call Reports is available faster, and the collection and validation process is more efficient. 4. End state The FFIEC targeted five specific areas for improvement. Vendor Software - The FFIEC provided Call Report software vendors with an XBRL, version 2.1 taxonomy.

Secure Transmission - A high level of security was needed in all phases of the data submission. Security had to encompass the entire process, from entry point to delivery point. The transmission process had to be automatic, with little or no input from the filing institution. Verification of Receipt - A verification or notification mechanism was required to enable automatic reply to the institutions when the transmission of the data had been completed. In addition, institutions needed to be able to verify receipt of their transmission by logging into the CDR system. Online Corrections - Respondents had to be notified if corrections were needed to the transmitted data. The institutions would have access to their data in the central data repository system. The online correction capability needed to be available in a real-time mode. Central Data Repository - A Centralized Data Repository, “system of record,” that banks, vendors and the agencies could use to exchange data needed to be created. 5. Benefits Improvements to the data collection process have reaped immediate benefits in terms of timeliness and quality of data for the banking agencies. The CDR utilizes XBRL to enable banks to identify and correct errors before they submit their data to the federal banking agencies. Consequently, initial third quarter 2005 data submissions were of a high quality received days sooner than in previous quarters, when most data validation occurred only after the initial submission to the agencies. Top line results of Call Report Modernization Project Using XBRL

http://www.xbrl.org/us/us/FFIEC%20White%20Paper%2002Feb2006.pdf

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

রিজার্ভ ব্যাঙ্ক অফ ইন্ডিয়া মোবাইল অ্যাপ্লিকেশন ইনস্টল করুন এবং সাম্প্রতিক সংবাদগুলিতে দ্রুত অ্যাক্সেস পান!

আমাদের অ্যাপটি ইনস্টল করতে QR কোডটি স্ক্যান করুন

পেজের শেষ আপডেট করা তারিখ: