FAQ Page 1 - আরবিআই - Reserve Bank of India

Content Type:

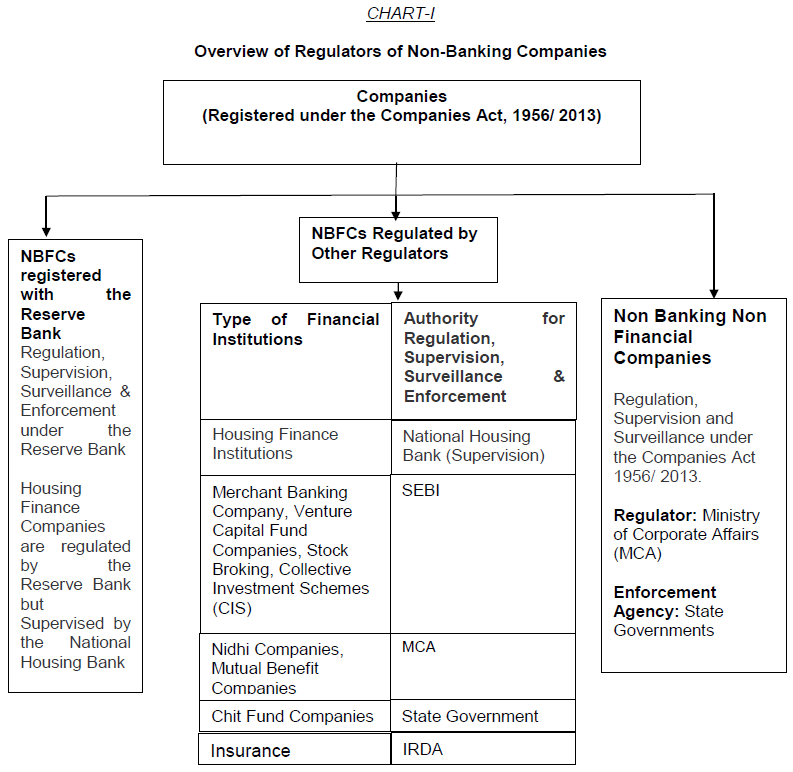

All you wanted to know about NBFCs

H. Other/ miscellaneous aspects

Where a non-NBFC mergers with an NBFC, prior written approval of the Reserve Bank would be required if such a merger satisfies any one or all of the conditions viz., (i) any change in control in the NBFC due to merger, (ii) any change in the shareholding of the NBFC consequent to the merger which would result in change in shareholding of 26% or more of the paid up equity capital of the NBFC, (iii) any change in the management of the NBFC which would result in change in more than 30% of the directors, excluding independent directors. It may be noted that the NBFC shall continue to fulfil the Principal Business Criteria (i.e., 50-50 criteria) after merger to be eligible to hold the Certificate of Registration as an NBFC.

The NBFCs being amalgamated will require to obtain prior written approval of the Reserve Bank. Depending upon the nature of amalgamation/merger proposal, requisite approvals as per regulations needs to be sought.

Yes, prior approval of the Reserve Bank would have to be obtained before approaching any Court or Tribunal seeking orders for merger/ amalgamation in all such cases which would ordinarily fall under the scenarios explained in FAQs 84, 85 or 86.

Disclaimer: These FAQs are issued by the Reserve Bank for information and general guidance purposes only. The Reserve Bank will not be held responsible for actions taken and/or decisions made on the basis of the same. For clarifications or interpretations, if any, one may be guided by the relevant circulars and notifications issued from time to time.

| Related Press Release | |

| May 31, 2013 | Check before Depositing Money with Financial Entities: RBI Advisory |

রিজার্ভ ব্যাঙ্ক অফ ইন্ডিয়া মোবাইল অ্যাপ্লিকেশন ইনস্টল করুন এবং সাম্প্রতিক সংবাদগুলিতে দ্রুত অ্যাক্সেস পান!