Monetary Policy Statement, 2024-25 Resolution of the Monetary Policy Committee (MPC) June 5 to 7, 2024 - RBI - Reserve Bank of India

Monetary Policy Statement, 2024-25 Resolution of the Monetary Policy Committee (MPC) June 5 to 7, 2024

| On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (June 7, 2024) decided to:

Consequently, the standing deposit facility (SDF) rate remains unchanged at 6.25 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 6.75 per cent.

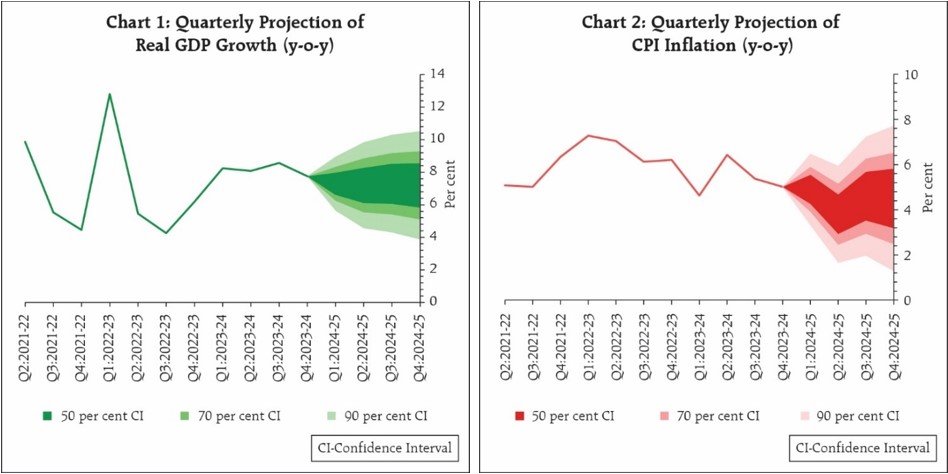

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth. Assessment and Outlook 2. Global economic activity is rebalancing and is expected to grow at a stable pace in 2024. Inflation has been moderating unevenly, with services inflation staying elevated and slowing progress towards targets. Uncertainty on the pace and timing of policy pivots by central banks is keeping financial markets volatile. Equity markets have touched new highs in both advanced and emerging market economies. Non-energy commodity prices have firmed up, while the US dollar and bond yields are exhibiting two-way movement with spillovers to emerging market currencies. Gold prices have surged to record highs on safe haven demand. 3. According to the provisional estimates released by the National Statistical Office (NSO) on May 31, 2024, real gross domestic product (GDP) growth in Q4:2023-24 stood at 7.8 per cent as against 8.6 per cent in Q3. Real GDP growth for 2023-24 was placed at 8.2 per cent. On the supply side, real gross value added (GVA) rose by 6.3 per cent in Q4:2023-24. Real GVA recorded a growth of 7.2 per cent in 2023-24. 4. Going forward, high frequency indicators of domestic activity are showing resilience in 2024-25. The south-west monsoon is expected to be above normal, which augurs well for agriculture and rural demand. Coupled with sustained momentum in manufacturing and services activity, this should enable a revival in private consumption. Investment activity is likely to remain on track, with high capacity utilisation, healthy balance sheets of banks and corporates, government’s continued thrust on infrastructure spending, and optimism in business sentiments. Improving world trade prospects could support external demand. Headwinds from geopolitical tensions, volatility in international commodity prices, and geoeconomic fragmentation, however, pose risks to the outlook. Taking all these factors into consideration, real GDP growth for 2024-25 is projected at 7.2 per cent with Q1 at 7.3 per cent; Q2 at 7.2 per cent; Q3 at 7.3 per cent; and Q4 at 7.2 per cent (Chart 1). The risks are evenly balanced. 5. Headline inflation has seen sequential moderation since February 2024, albeit in a narrow range from 5.1 per cent in February to 4.8 per cent in April 2024. Food inflation, however, remains elevated due to persistence of inflation pressures in vegetables, pulses, cereals, and spices. Deflation in fuel prices deepened during March-April, reflecting the cut in liquified petroleum gas (LPG) prices. Core (CPI excluding food and fuel) inflation eased further to 3.2 per cent in April, the lowest in the current CPI series, with core services inflation also falling to historic lows. 6. Looking ahead, overlapping shocks engendered by rising incidence of adverse climate events impart considerable uncertainty to the food inflation trajectory. Market arrivals of key rabi crops, particularly pulses and vegetables, need to be closely monitored in view of the recent sharp upturn in prices. Normal monsoon, however, could lead to softening of food inflation pressures over the course of the year. Pressure from input costs have started to edge up and early results from enterprises surveyed by the Reserve Bank expect selling prices to remain firm. Volatility in crude oil prices and financial markets along with firming up of non-energy commodity prices pose upside risks to inflation. Taking into account these factors, CPI inflation for 2024-25 is projected at 4.5 per cent with Q1 at 4.9 per cent; Q2 at 3.8 per cent; Q3 at 4.6 per cent; and Q4 at 4.5 per cent (Chart 2). The risks are evenly balanced.

7. The MPC noted that the domestic growth-inflation balance has moved favourably since its last meeting in April 2024. Economic activity remains resilient supported by domestic demand. Investment demand is gaining more ground and private consumption is exhibiting signs of revival. Although headline inflation is gradually easing, driven by softening in its core component, the path of disinflation is interrupted by volatile and elevated food inflation due to adverse weather events. Inflation is expected to temporarily fall below the target during Q2:2024-25 due to favourable base effect, before reversing subsequently. For the final descent of inflation to the target and its anchoring, monetary policy has to be watchful of spillovers from food price pressures to core inflation and inflation expectations. The MPC will remain resolute in its commitment to aligning inflation to the 4 per cent target on a durable basis. Accordingly, the MPC decided to keep the policy repo rate unchanged at 6.50 per cent in this meeting. The MPC reiterates the need to continue with the disinflationary stance, until a durable alignment of the headline CPI inflation with the target is achieved. Enduring price stability sets strong foundations for a sustained period of high growth. Hence, the MPC also decided to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns to the target, while supporting growth. 8. Dr. Shashanka Bhide, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to keep the policy repo rate unchanged at 6.50 per cent. Dr. Ashima Goyal and Prof. Jayanth R. Varma voted to reduce the policy repo rate by 25 basis points. 9. Dr. Shashanka Bhide, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns to the target, while supporting growth. Dr. Ashima Goyal and Prof. Jayanth R. Varma voted for a change in stance to neutral. 10. The minutes of the MPC’s meeting will be published on June 21, 2024. 11. The next meeting of the MPC is scheduled during August 6 to 8, 2024. (Puneet Pancholy) Press Release: 2024-2025/453 |

Share this page:

Install the RBI mobile application and get quick access to the latest news!