FAQ Page 1 - RBI - Reserve Bank of India

Content Type:

FAQs on Master Directions on Priority Sector Lending Guidelines

A. Computation of Adjusted Net Bank Credit (ANBC)

Clarification: The net PSLC outstanding (PSLC Buy minus(-) PSLC Sell) is added to the Net Bank Credit, as mentioned in para 6 of the Master Directions on PSL, 2020 (updated from time to time). Further, a PSLC remains outstanding until its expiry (s. no. ix of Notification on Priority Sector Lending certificates dated April 07, 2016, All PSLCs will expire by March 31st and will not be valid beyond the reporting date (i.e. March 31st), irrespective of the date it was first bought/sold. Accordingly, the effect of PSLC buy is increase in ANBC and conversely the effect of PSLC sell is decrease in ANBC and the net of PSLC buy/sell is adjusted to the ANBC for every quarter. Thus, a PSLC bought or sold in any quarter will have to be taken into account in all subsequent quarters till the end of the FY to which it pertains.

Clarification: The Master Directions on Priority Sector Lending, 2020 under para 6 provides for computation of Adjusted Net Bank Credit. The face value of securities availed under TLTRO 2.0 and SLF-MF (including the Extended Regulatory Benefits) are to be reduced (as given in ‘IX’ of para 6.1 of the Master Directions on PSL). Since these securities are considered as HTM investments, the banks have to add them as Bonds/debentures in Non-SLR categories under HTM category (as given in ‘X’ of para 6.1 of the Master Directions on PSL). It is envisaged that the Priority Sector Lending target/sub-targets should not increase on account of securities acquired under TLTRO 2.0 and SLF-MF (including the Extended Regulatory Benefits). By adding the face value of securities (X) and reducing the face value of securities (IX) there will be no increase in ANBC due to investments in TLTRO 2.0 and SLF-MF (including the Extended Regulatory Benefits.)

Clarification: The bills purchased/ discounted/ negotiated (payment to beneficiary not under reserve) under LC is allowed to be treated as Interbank exposure only for the limited purpose of computing exposure and capital requirements. It should not be excluded from the computation of ‘bank credit in India’ [As prescribed in item No.VI of Form 'A’ under Section 42(2) of the RBI Act, 1934] which allows for exclusion of interbank advance. While exposure may be to the LC issuing bank, the bills purchased/discounted amounts to bank credit to its borrower constituent. If this advance is eligible for priority sector classification, then bank can claim it as PSL. Banks have to take note of the above aspect while reporting Net Bank Credit in India as well as computing the Adjusted Net Bank Credit for PSL targets and achievement

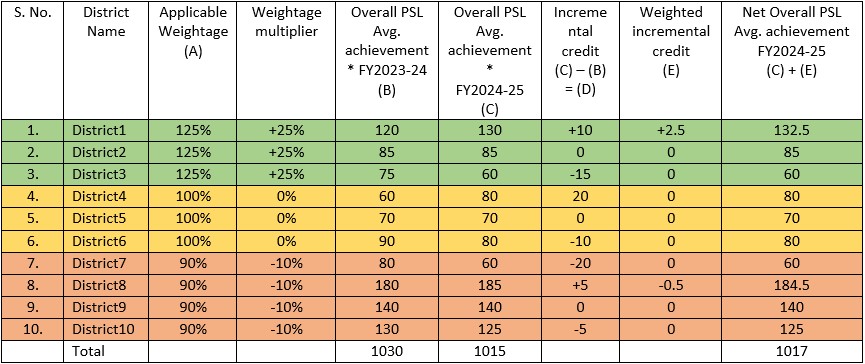

B. Adjustment for Weights in PSL Achievement

Clarification: As detailed in Para 7 of the Master Directions on Priority Sector lending, 2020 on “Adjustments for weights in PSL Achievement”, differential weightage in the incremental credit to the priority sector areas shall be reckoned from FY 2021-22 onwards. From, FY2024-25, there will be 125% weightage on incremental credit to select 196 districts with low per capita PSL credit and 90% weightage on incremental credit to select 198 districts with high per capita PSL credit. The PSL achievement against the applicable PSL target/sub-targets will be calculated after applying weightages on the incremental credit for each low/high per capita PSL credit district and PSL shortfall will be arrived at accordingly.

Clarification: If there is a decline in credit, the weighted incremental credit will be zero (0). The methodology as given below will be considered for all the districts for which data is reported in ADEPT and District-QPSA statement. Further, based on the methodology detailed above, banks are expected to monitor their own PSL achievement during the year taking into account the prescription of differential weights for credit in identified districts, for the purpose of trading in PSLCs.

* Avg. achievement will be the average of four quarters of a year, as on reporting dates of District-QPSA. Similar calculations will be done for other PSL targets.

Clarification: While calculating district-wise incremental credit for assigning weights, the organic credit i.e. only the credit directly disbursed by banks and for which the actual borrower/beneficiary wise details are maintained in the books of the bank will be considered. Credit disbursed through the following inorganic routes shall not be considered for incremental weights.

-

Investments by banks in securitised assets

-

Transfer of Assets through Direct Assignment /Outright purchase

-

Inter Bank Participation Certificates (IBPCs)

-

Priority Sector Lending Certificates (PSLCs)

-

Bank loans to MFIs (NBFC-MFIs, Societies, Trusts, etc.) for on-lending

-

Bank loans to NBFCs for on-lending

-

Bank loans to HFCs for on-lending

C. Agriculture

Clarification: The PSL guidelines are activity and beneficiary specific and are not based on type of collateral. Therefore, bank loans given to individuals/ businesses for undertaking agriculture activities do not automatically become ineligible for priority sector classification, only on account of the fact that underlying asset is gold jewellery/ornament etc. It may, however, be noted that as per FIDD Circular dated February 7, 2019 and updated from time to time, it has been advised that banks may waive margin requirements for agricultural loans upto ₹1.6 lakh. Therefore, bank should have extended the loan based on scale of finance and assessment of credit requirement for undertaking the agriculture activity and not solely based on available collateral in the form of gold. Further, as applicable to all loans under PSL, banks should put in place proper internal controls and systems to ensure that the loans extended under priority sector are for approved purposes and the end use is continuously monitored.

Clarification: As per Annex-III of Master Directions on Priority Sector Lending (PSL) dated September 4, 2020, transportation is an eligible activity under indicative list of permissible activities under Food Processing Sector. However, while classifying any facility to transporters for purchasing Commercial Vehicles under “Food & Agro-processing” category, it needs to be ensured that the transporter is using the vehicle exclusively for transportation of food & agro-processed products or is a type of vehicle which is specifically used for “Food & Agro-processing” e.g. cold storage trucks, vans etc. If the commercial vehicle is also used for transportation of products other than those related to food & agro processing, the facility shall not be eligible for classification under ‘Food & Agro-processing’ category. In such cases, the same may be classified under MSME (Services), if it meets the conditions prescribed for the same in our Master Direction on PSL.

D. MSME

Clarification: Government of India (GoI), vide Gazette Notification S.O. 2119 (E) dated June 26, 2020 and updated from time to time, has notified the new composite criteria of investment in plant & machinery as well as turnover for classification of an enterprise under MSME. Under the composite criteria, if an enterprise crosses the ceiling limits specified for its present category in either of the two criteria of investment or turnover, it will cease to exist in that category and be placed in the next higher category but no enterprise shall be placed in the lower category unless it goes below the ceiling limits specified for its present category in both the criteria of investment as well as turnover. Based on the new definition, the earlier criteria regarding continuity of PSL status for three years even after an enterprise grows out of the MSME category concerned, is no longer valid.

E. Export Credit

Clarification: Bank lending to export credit under agriculture and MSME sectors is classified as PSL under the respective categories viz, agriculture and MSME and there is no cap on credit for the same. Export Credit (other than in agriculture and MSME) is classified as priority sector as per the following table:

| Domestic banks / WoS of Foreign banks/ SFBs/ UCBs | Foreign banks with 20 branches and above | Foreign banks with less than 20 branches |

| Incremental export credit over corresponding date of the preceding year, up to 2 per cent of ANBC or CEOBE whichever is higher, subject to a sanctioned limit of up to ₹40 crore per borrower. | Incremental export credit over corresponding date of the preceding year, up to 2 percent of ANBC or CEOBE whichever is higher. | Export credit up to 32 per cent of ANBC or CEOBE whichever is higher. |

F. Education

Clarification: For the loans sanctioned before September 4, 2020, outstanding value up to ₹10 lakh, irrespective of the sanctioned limit, shall continue to be classified under priority sector till maturity. However, while reckoning any fresh loan under PSL to a borrower who had already availed education loan from the bank prior to September 4, 2020, it needs to be ensured that the aggregate sanctioned limit does not exceed ₹20 lakh for classification of the loans under PSL.

In the mentioned scenario, as the combined sanctioned limit becomes ₹30 lakh, the ₹18 lakh loan extended after September 4, 2020 shall not be eligible for PSL classification. However, with regard to the ₹12 lakh loan, which was already PSL as per earlier guidelines, the outstanding value under the facility, up to ₹10 lakh shall continue to be eligible under PSL till maturity.

G. Social Infrastructure

H. Weaker Sections

Clarification: As per extant guidelines, priority sector loans are eligible for classification as loans to minority communities as per the list notified by the GoI from time to time. The same may be read with Master Circular- Credit Facilities to Minority Communities which under para 2.2 states “In the case of a partnership firm, if the majority of the partners belong to one or the other of the specified minority communities, advances granted to such partnership firms may be treated as advances granted to minority communities. Further, if the majority beneficial ownership in a partnership firm belongs to the minority community, then such lending can be classified as advances to the specified communities. A company has a separate legal entity and hence advances granted to it cannot be classified as advances to the specified minority communities.”

I. Investment by Banks in securitized assets / Transfer of Assets through Direct Assignment/ Outright Purchase

J. PSLCs

Clarification: The banks are required to submit a request to FIDD, CO (fiddplan@rbi.org.in) to obtain registration for PSLC trading by submitting a) DEA Fund Code b) Customer identification number and c) RBI Current account number.

Clarification: All PSLCs will be valid till end of FY i.e. March 31st and will expire on next day i.e. April 1st.

Clarification: The duration of the PSLCs will depend on the date of issue with all PSLCs being valid till end of FY i.e. March 31st and expiring on next day i.e. April 1st.

Clarification: PSLCs may be construed in the nature of 'goods' in the course of inter-state trade or commerce, dealing in which has been notified as a permissible activity under section 6(1)(o) of BR Act vide Government of India Notification dated May 4, 2016. GST on PSLCs for the period July 01, 2017 to May 28, 2018 has to be paid by the seller bank on forward charge basis at the rate of 12%. With effect from May 28, 2018, GST has to be paid by the buyer bank under Reverse Charge Mechanism (RCM) at the rate of 18%. Further, IGST is payable on the supply of PSLC traded over e-kuber portal. If a bank which was liable to pay GST had already paid CGST/SGST or CGST/UGST, the bank is not required to pay IGST towards such supply. Further, as per the extant guidelines, no transaction charge/ fees is applicable on the participating banks payable to RBI for usage of the PSLC module on e-Kuber portal.

(The clarification given above is not a legal advice or opinion in the matter and it may not necessarily reflect the most current legal developments. The market participants should seek the advice of the tax experts/consultants/specialists before acting upon any of the information provided above).

Clarification: There are only four eligible categories of PSLCs i.e. PSLC General, PSLC Small and Marginal Farmer, PSLC Agriculture & PSLC Micro Enterprises.

Clarification: 'Export Credit' can form a part of underlying assets against the PSLC - General. However, any bank issuing PSLC-General against 'Export Credit' shall ensure that the underlying 'Export Credit' portfolio is also eligible for priority sector classification by domestic banks.

Clarification: Foreign banks with less than 20 branches are not allowed to buy PSLC General for achieving their 8% target of lending to sectors other than exports. However, such banks are allowed to buy PSLC Agriculture, PSLC Micro Enterprises and PSLC Small and Marginal Farmer for the same.

Clarification: The trade summary of PSLC market is available to the participants through the e-Kuber portal. Any new functionality will be notified to the participants via 'News & Announcements' section under e-Kuber portal.

Clarification: A bank can purchase PSLCs as per its requirements. Further, a bank is permitted to issue PSLCs upto 50 percent of previous year’s PSL achievement without having the underlying in its books. This is applicable category-wise. The net position of PSLCs (PSLC Buy – PSLC Sell) has to be considered while reporting the quarterly and annual priority sector returns. However, with regard to ascertaining the underlying assets, as on March 31st, the bank must have met the priority sector target by way of the sum of outstanding priority sector portfolio and net of PSLCs issued and purchased.

Clarification: The misclassifications, if any, will have to be reduced from the achievement of PSLC seller bank only. There will be no counterparty risk for the PSLC buyer, even if, the underlying asset of the traded PSLC gets misclassified.

Clarification: The premium will be completely market determined. No floor/ ceiling has been prescribed by RBI in this regard.

Clarification: There will be real time settlement of the matched premium and accordingly respective current accounts of the participating banks with RBI will be debited/ credited to the extent of matched premium

Clarification: The order matching will be done on anonymous basis through the portal and the buyer/ seller cannot select the counterparty. Partial matching will happen depending on the matching of premium and availability of category wise PSLC lots for sale and purchase.

Clarification: The normal trading hours shall be from 10 AM to 4:30 PM. The PSLC market operates on all days except Saturdays, Sundays, holidays declared under The Negotiable Instruments Act, 1881 by the Government of Maharashtra. and such holidays as RBI may declare from time to time.

Clarification: The nature of PSLC trading has been kept anonymous to maintain most efficient price discovery. There is no provision for settling deals on bilateral basis and reporting on the portal subsequently. RBI has the discretion to cancel any deals which is settled at substantially higher/ lower premiums as compared to the prevailing rates on the portal.

K. On-lending under Priority Sector

Clarification: In the case of bank’s lending to NBFCs / MFIs / HFCs for on-lending, only that portion of the portfolio should be reckoned for PSL classification that has been disbursed by the NBFC / MFI / HFC to the ultimate borrower/s as on the reporting date. The reckoning of residual portfolio, if any, can be done on subsequent reporting dates, based on the disbursement of eligible loans and reported by the NBFC / MFI / HFC to the bank.

Clarification: The Master Directions on Priority Sector Lending, 2020 under para 21, 22, 23 allows banks to classify as PSL its lending to NBFCs including HFCs and NBFC-MFIs and other MFIs (Societies, Trusts etc.) which are members of RBI recognised SRO for the sector for on-lending to eligible priority sectors. Banks may adopt a uniform methodology for on-lending as follows:

a) Classification under PSL:

• The banks can classify on-lending to NBFC in the respective categories of PSL. The classification will be allowed only when the NBFC has disbursed the Priority Sector Loans to the ultimate beneficiary after receiving the funds from the bank.

• The NBFCs must provide a CA certificate to the banks stating that the individual loans of the portfolio, against which on-lending benefit is being claimed, are not being used to claim benefit from any other bank(s). Also, NBFC must put in place a suitable process to flag such loan(s) in their systems to enable its internal/statutory auditors as well as RBI supervisors to verify the same.

b) Information sharing:

• The banks may devise internal control mechanisms to ensure that the portfolio under on-lending is PSL compliant and adheres to co-terminus clause. The same should be made available to RBI supervisor/s as and when required. The following information/record should be collected by the bank from the EI:

-

Name of the beneficiary, Amount sanctioned, Loan amount outstanding, Loan tenure, disbursement date, category of PSL.

-

A statement to the effect that the portfolio is PSL compliant must be certified by a CA and shared by the EI with the bank on a quarterly basis in line with the PSL reporting by the bank to RBI. With respect to adherence to the co-terminus clause, the bank should ensure the same as on March 31 each year.

c) Adherence to co-terminus condition:

• The banks availing benefit of on-lending for PS assets must adhere to the condition that the tenure of the loan under on-lending to an EI is broadly co-terminus with the tenure of PS assets created by the EI.

• In view of the operational difficulties of exactly matching the co-terminus duration, the banks are allowed a variance of 3 months from the portfolio duration. An illustration for calculating adherence to the co-terminus duration is given below:

| Sr. No. | Loan outstanding (A) | 31st March of current FY (B) | Loan end date (C) | Loan period (days) (D= C-B) | Weighted average loan outstanding days (E=A*D) |

| 1 | 50000 | 31-03-21 | 01-02-23 | 672 | 33600000 |

| 2 | 80000 | 31-03-21 | 01-05-24 | 1127 | 90160000 |

| 3 | 100000 | 31-03-21 | 11-08-23 | 863 | 86300000 |

| 4 | 300000 | 31-03-21 | 16-10-22 | 564 | 169200000 |

| 5 | 400000 | 31-03-21 | 23-11-22 | 602 | 240800000 |

| Total | 930000 | 620060000 | |||

| Weighted maturity of portfolio in days (F=(sum of E)/(sum of A) | 666.73 | ||||

| In months (F/30) | 22.22 | ||||

| In years (F/365) | 1.83 | ||||

In the above illustration, the residual maturity of bank loan to NBFC should be around 22.22 months. Banks are expected to calculate the weighted average residual maturity of portfolio ever year as on March 31 and ensure that residual maturity of bank loan to NBFC matches with the weighted average residual maturity of on-lending portfolio within the tolerance limit of +-3 months.

d) Treatment of pre-payment, foreclosure loans:

-

The PS assets created by the entity may undergo pre-payment or foreclosure thereby changing the ‘weighted maturity’ of the portfolio.

-

As the banks are required to calculate ‘weighted maturity’ at the end of FY, the loan outstanding in the event of pre-payment/foreclosure will also change accordingly.

-

The NBFC may add PS assets to the on-lending portfolio. However, it must meet conditions mentioned above such as disbursements for the PS asset by the eligible entity must be on/after receipt of funds from the bank. The addition of PS assets to the portfolio pool can also be done in case of pre-payment/foreclosure of other PS assets in the pool to ensure adherence to the co-terminus clause.

Clarification: Bank lending to NBFCs (other than MFIs) and HFCs are subjected to a cap of 5% of average PSL achievement of the four quarters of the previous financial year. In case of a new bank the cap shall be applicable on an on-going basis during its first year of operations. The prescribed cap is not applicable for bank lending to registered NBFC-MFIs and other MFIs (Societies, Trusts, etc.) which are members of RBI recognised ‘Self-Regulatory Organisation’ of the sector. Bank lending to such MFIs can be classified under different categories of PSL in accordance with conditions specified in our Master Directions FIDD.CO.Plan.BC.5/04.09.01/2020-21 dated September 04, 2020 and updated from time to time.

L. Co-lending by Banks & NBFCs

Clarification: While the guidelines allow sharing of risks and rewards between the bank and the NBFC for ensuring appropriate alignment of respective business objectives, the priority sector assets on the bank’s books should at all times be without recourse to the NBFC.

Clarification: Only if the bank can exercise its discretion regarding taking into its books the loans originated by NBFC as per the Agreement, the arrangement will be akin to a direct assignment transaction. If the Agreement entails a prior, irrevocable commitment on the part of the bank to take into its books its share of the individual loans as originated by the NBFC, it shall not be akin to direct assignment transaction.

Clarification: Both entities, the bank & the NBFC shall be guided by the bilateral Master Agreement entered by them for implementing the Co-lending Model (CLM). The agreement may state any cap on the number and amount of loans that can be originated by the NBFC under the Co-lending model.

Clarification: If the Agreement entails a prior, irrevocable commitment on the part of the bank, it has been advised that the partner bank and NBFC shall have to put in place suitable mechanisms for ex-ante due diligence by the bank. Such due diligence should ensure compliance with RBI regulations on KYC and outsourcing of activities before disbursal of the loans by the NBFC.

Clarification: Back-to-back basis implies that the loans will be first opened by NBFC and then bank will open loan accounts subsequently.

Install the RBI mobile application and get quick access to the latest news!

Page Last Updated on: December 10, 2022