FAQ Page 1 - ଆରବିଆଇ - Reserve Bank of India

Content Type:

All you wanted to know about NBFCs

E. Depositor Protection Issues

Companies registered with MCA but not required to be registered with the Reserve Bank as NBFCs are not under the regulatory domain of the Reserve Bank. Whenever Reserve Bank receives any such complaints about the companies registered with MCA but not registered with the Reserve Bank as NBFCs, it forwards the complaints to the Registrar of Companies (RoC) of the respective state for any action. The complainants are advised that the complaints relating to irregularities of such companies should be promptly lodged with RoC concerned for initiating corrective action. However, in case it comes to the knowledge of the Reserve Bank that those companies were required to be registered with the Reserve Bank but have not done so and have accepted deposits as defined under RBI Act, such action, as is deemed necessary under the provisions of the RBI Act, will be taken.

FAQs on Non-Banking Financial Companies

Depositor Awareness

All you wanted to know about NBFCs

E. Depositor Protection Issues

As per Reserve Bank’s Directions, overdue interest is payable to the depositors in case the NBFC has delayed the repayment of matured deposits, and such interest is payable from the date of receipt of such claim by the NBFC or the date of maturity of the deposit whichever is later, till the date of actual payment. If the depositor has lodged his claim after the date of maturity, the NBFC would be liable to pay interest for the period from the date of claim till the date of repayment. For the period between the date of maturity and the date of claim it is the discretion of the company to pay interest.

In cases where NBFCs are required to freeze the term deposits of customer based on the orders of the Government authorities or the deposit receipts are seized by the Government authorities, they shall follow the procedure as given below:

i. A request letter may be obtained from the depositor on maturity. While obtaining the request letter from the depositor for renewal, NBFCs should also advise him to indicate the term for which the deposit is to be renewed. In case the depositor does not exercise his option of choosing the term for renewal, NBFCs may renew the same for a term equal to the original term.

ii. No new receipt is required to be issued. However, suitable note may be made regarding renewal in the deposit ledger.

iii. Renewal of deposit may be advised by registered letter / speed post / courier service to the concerned Government department under advice to the depositor. In the advice to the depositor, the rate of interest at which the deposit is renewed should also be mentioned.

iv. If overdue period does not exceed 14 days on the date of receipt of the request letter, renewal may be done from the date of maturity. If it exceeds 14 days, NBFCs may pay interest for the overdue period as per the policy adopted by them, and keep it in a separate interest free sub-account which should be released when the original fixed deposit is released.

However, the final repayment of the principal and the interest so accrued should be done only after the clearance regarding the same is obtained by the NBFCs from the respective Government agencies.

FAQs on Non-Banking Financial Companies

RNBCs

All you wanted to know about NBFCs

E. Depositor Protection Issues

An NBFC accepts deposits under a mutual contract with its depositors. In case a depositor requests for pre-mature payment, the Reserve Bank has prescribed regulations for such an eventuality in the Master Direction - Non-Banking Financial Companies Acceptance of Public Deposits (Reserve Bank) Directions, 2016 (as amended from time to time) wherein it is specified that NBFCs cannot grant any loan against a public deposit or make premature repayment of a public deposit within a period of three months (lock-in period) from the date of its acceptance. However, in the event of death of a depositor, the NBFC may, even within the lock-in period, repay the deposit at the request of the joint holders with survivor clause, or to the nominee / legal heir only against submission of relevant proof, to the satisfaction of the NBFC. Further, in order to enable a depositor to meet the expenses of an emergent nature, the NBFC may subject to satisfaction of the NBFC about the circumstances, prematurely repay tiny deposits (i.e., up to ₹10,000/-) and also other deposits, as per the provisions laid down by the Reserve Bank.

An NBFC, which is not a problem company, subject to above provisions, may permit premature repayment of a public deposit after the lock–in period, at its sole discretion, at the rate of interest prescribed by the Reserve Bank.

A problem NBFC is prohibited from making premature repayment of any deposits or granting any loan against public deposits, as the case may be. The prohibition shall not, however, apply in the case of death of depositor or repayment of tiny deposits (i.e. up to ₹ 10,000/-) in order to enable a depositor to meet expenses of an emergent nature, subject to lock in period of 3 months in the latter case.

FAQs on Non-Banking Financial Companies

Nomination facility

All you wanted to know about NBFCs

E. Depositor Protection Issues

In terms of Section 45-IB of the RBI Act, 1934, the minimum level of liquid assets to be maintained by deposit taking NBFCs is 15% of public deposits outstanding as on the last working day of the second preceding quarter. Of the 15%, NBFCs are required to invest not less than 10% in approved securities and the remaining 5% can be in unencumbered term deposits with any Scheduled Commercial Bank (SCB)/ SIDBI/ NABARD; or bonds issued by SIDBI or NABARD. Thus, the liquid assets may consist of Government securities, Government guaranteed bonds and term deposits/ bonds, as specified.

The investment in Government Securities should be in dematerialised form which can be maintained in Subsidiary General Ledger (SGL) Account with the Reserve Bank or a Gilt Account with Constituents’ Subsidiary General Ledger (CSGL) Account or a dematerialized account with a depository through a depository participant registered with SEBI. In case of Government guaranteed bonds, the same may be kept in dematerialised form with SCB/ Stock Holding Corporation of India Limited (SHCIL) or in a dematerialised account with a depository through a depository participant registered with SEBI. However, in case Government bonds are in physical form, the same may be kept in safe custody of SCB/SHCIL along with term deposits of SCB/ SIDBI/ NABARD.

NBFCs have been directed to maintain the mandated liquid asset securities at a place where the registered office of the company is situated. However, if an NBFC intends to entrust the securities at a place other than the place at which its registered office is located, it may do so after obtaining the permission of the Reserve Bank in writing. The liquid assets maintained as above are to be utilised for payment of claims of depositors. However, deposits being unsecured in nature, the depositors do not have direct claim on liquid assets.

The Reserve Bank has issued detailed regulations on deposit acceptance, including the quantum of deposits that can be collected, mandatory credit rating, mandatory maintenance of liquid assets for repayment to depositors, manner of maintenance of its deposit books, prudential regulations including maintenance of adequate capital, limitations on exposures, and inspection of the NBFCs, besides others, to ensure that the NBFCs function on sound lines. If the Reserve Bank observes through its inspection or audit of any NBFC or through complaints or through market intelligence, that a certain NBFC is not complying with the Reserve Bank’s directions, it may prohibit the NBFC from accepting further deposits and prohibit it from selling its assets. In addition, if the depositor has complained to the Company Law Board (CLB) [now National Company Law Tribunal (NCLT)] which has ordered repayment and the NBFC has not complied with the CLB/NCLT order, the Reserve Bank can initiate prosecution of the NBFC, including criminal action and winding up of the NBFC.

More importantly, the Reserve Bank initiates prompt action, including imposing penalties and taking legal action against companies which are found to be violating its instructions/norms on the basis of Market Intelligence reports, complaints, exception reports from statutory auditors of the companies, information received through SLCC meetings, etc. The Reserve Bank immediately shares such information with all the financial sector regulators and enforcement agencies in the State Level Coordination Committee Meetings.

As part of its public policy measure, the Reserve Bank has been in the forefront in taking several initiatives to create awareness among the general public on the need to be careful while investing their hard earned money. The initiatives include issue of cautionary notices in print media and distribution of informative and educative brochures/pamphlets and close interaction with the public during awareness/outreach programs, Townhall events, participation in State Government sponsored trade fairs and exhibitions. At times, it even requests newspapers with large circulation (English and vernacular) to desist from accepting advertisements from unincorporated entities seeking deposits. The Reserve Bank has also launched its public awareness initiative with the tag line ‘RBI Kehta Hai’ which may be accessed at https://rbikehtahai.rbi.org.in/.

NBFCs shall obtain credit rating from any of the SEBI-registered credit rating agencies.

The minimum investment grade credit rating issued by any of the SEBI-registered credit rating agencies for deposit taking NBFCs shall be ‘BBB–‘.

In the event of downgrading of credit rating below the minimum specified investment grade rating, the deposit taking NBFC shall stop accepting public deposits and also stop renewing existing deposits with immediate effect, however the existing deposits would be allowed to run off to maturity. The NBFCs shall also report the position within fifteen working days to the Reserve Bank.

The purpose of enacting this law is to protect the interests of the depositors. The provisions of RBI Act are directed towards enabling RBI to issue prudential regulations that make the financial entities function on sound lines. RBI is a civil body and the RBI Act is a civil Act. Both do not have specific provisions to effect recovery by attachment and sale of assets of the defaulting companies, entities or their officials. It is the State government machinery which can effectively do this. The Protection of Interest of Depositors in Financial Establishments Acts, confers adequate powers on the State Governments to attach and sell assets of the defaulting companies, entities and their officials.

Yes, to a large extent. The Act makes offences, such as, unauthorized acceptance of deposits by any entity, firm or company a cognizable offence, that is entities that are indulging in unauthorized deposit acceptance or unlawful financial activities can be immediately imprisoned and prosecuted. Under the Act, the State Governments have been given vast powers to attach the property of such entities, dispose them off under the orders of special courts and distribute the proceeds to the depositors. The widespread State Government / State Police machinery is best positioned to take quick action against the culprits.

Further, Government of India has recently enacted the Banning of Unregulated Deposit Schemes Act, 2019, a Central Legislation, which provides a comprehensive mechanism to ban the unregulated deposit schemes, other than deposits taken in ordinary course of business, and to protect the interest of depositors. This Act has specific provisions for restitution of depositors through various means viz., attachment and sale of property, etc. This Act also provides for enhanced legislative mechanism for handling unregulated deposit schemes viz., constitution of Designated Courts to deal with matters under the Act, powers for investigation (including by Central Bureau of Investigation in case deposits, deposit-takers and properties are located in more than one State or Union Territory, or outside India), search & seizure, penal provisions, etc.

The Reserve Bank is strengthening its market intelligence function and is constantly examining the financials of companies, references for which are received through market intelligence or complaints to the Reserve Bank. As part of initiative of State Level Consultation Committee comprising of Regulators and Government, the Sachet portal (https://sachet.rbi.org.in/) has been launched and members of public are requested to share any relevant information pertaining to unauthorised collection of deposits. In this, context, members of public can contribute a great deal by being vigilant and lodging a complaint immediately if they come across any financial entity that contravenes the RBI Act. For example, if they are accepting deposits unauthorisedly and/conducting NBFC activities without obtaining due permission from the Reserve Bank. More importantly, these entities will not be able to function if members of public start investing wisely. Members of the public must know that high returns on investments will also have high risks. And there can be no assured return for speculative activities. Before investing, the public must ensure that the entity they are investing in is a regulated entity with one of the financial sector regulators.

F. Collective Investment Schemes (CIS) and Chit Funds

No. CIS are schemes where money is exchanged for units, be it profits, income, produce, property etc. Collective Investment Schemes (CIS) do not fall under the regulatory purview of the Reserve Bank and falls under the regulatory purview of SEBI.

Chit Fund companies are regulated under the Chit Fund Act, 1982, which is a Central Act, and is implemented by the State Governments. In order to avoid duality of regulation, companies, doing the business of chit, as defined under Section 2(b) of the Chit Funds Act, 1982 are exempted from the provisions of Section 45-IA, 45-IB and 45-IC of the RBI Act, 1934. Thus, chit fund companies are not required to be registered with the Reserve Bank and would be registered and regulated by the State Government under Chit Funds Act, 1982. However, chit fund companies are subject to other provisions under Chapter IIIB of the RBI Act, 1934 and the Reserve Bank has prohibited chit fund companies from accepting deposits from the public in 2009. In case any Chit Fund is accepting public deposits, the Reserve Bank can prosecute such chit funds

G. Money Circulation/Multi-Level Marketing (MLM)/ Ponzi Schemes/ Unincorporated Bodies (UIBs)

No, Multi-Level Marketing companies, Direct Selling Companies, Online Selling Companies do not fall under the purview of the Reserve Bank. Activities of these companies fall under the regulatory/administrative domain of respective state government. The provisions of the Consumer Protection Act, 2019 and the Consumer Protection (Direct Selling) Rules, 2021 may be referred. The list of regulators and the entities regulated by them are provided in Annex I.

While some of these terms are not formally defined, generally, the money circulation, multi-level marketing / chain marketing or Ponzi schemes are schemes promising easy or quick money upon enrollment of members. Income under multi-level marketing or pyramid structured schemes do not come from the sale of products they offer as much as from enrolling more and more members from whom hefty subscription fees are taken. It is incumbent upon all members to enroll more members, as a portion of the subscription amounts so collected is distributed among the members at the top of the pyramid. Any break in the chain leads to the collapse of the pyramid, and the members lower in the pyramid are the ones that are affected the most. Ponzi schemes are those schemes that collect money from the public on promises of high returns. As there is no asset creation, money collected from one depositor is paid as returns to the other. Since there is no other activity generating returns, the scheme becomes unviable and impossible for the people running the scheme to meet the promised return or even return the principal amounts collected. The scheme inevitably fails, and the perpetrators disappear with the money.

No. Acceptance of money under Money Circulation Schemes, by whatever name called, is not allowed as acceptance of money under those schemes is a cognizable offence under the Prize Chit and Money Circulation (Banning) Act, 1978, and are banned. The Reserve Bank has no role in implementation of this Act, except advising and assisting the Central Government in framing the Rules under this Act.

Money Circulation schemes, by whatever name called, are an offence under the Prize Chits and Money Circulation Schemes (Banning) Act, 1978. The Act prohibits any person or individual to promote or conduct any money circulation scheme or enrol as member to its schemes or anyone to participate in it by either receiving or remitting any money in pursuance of such chit or scheme. Contravention of the provisions of this Act, is monitored and dealt with by the State Governments.

Any information/grievance relating to such schemes should be given to the police / Economic Offence Wing (EOW) of the concerned State Government or the Ministry of Corporate Affairs. If brought to the notice of the Reserve Bank, the same shall be informed to the concerned State Government authorities.

UIBs include an individual, a firm or an unincorporated association of individuals. In terms of provisions of section 45S of RBI Act, these entities are prohibited from accepting any deposit. The Act makes acceptance of deposits by such UIBs punishable with imprisonment or fine or both. The State government has to play a proactive role in arresting the illegal activities of such entities to protect the interests of depositors.

UIBs do not come under the regulatory domain of the Reserve Bank. Whenever the Reserve Bank receives any complaints against UIBs, it immediately forwards the same to the Economic Offences Wing (EOW) of the State Government police agencies. The complainants are also advised to lodge the complaints directly with the State government police authorities (EOW) so that appropriate action against the culprits is taken immediately and the process is hastened.

As per Section 45T of the RBI Act, both the Reserve Bank and the State Governments can apply for search warrant before appropriate Court, and on issue of such warrant, the same shall be executed as per procedure laid down in Law by the enforcement authorities. Nonetheless, in order to take immediate action against the offenders, the information should immediately be passed on to the State Police or the Economic Offences Wing of the concerned State, who can take prompt and appropriate action. Since the State Government machinery is widespread and the State Government is also empowered to take action under the provisions of the RBI Act, 1934, any information on such entities accepting deposits may be provided immediately to the respective State Government’s Police Department/EOW.

Many of the State Governments have enacted the State Protection of Interests of Depositors in Financial Establishments Act, which empowers the State Government to take appropriate and timely action.

The Reserve Bank on its part has taken various steps to curb activities of UIBs which includes spreading awareness through advertisements in leading newspapers to sensitise public, organize various depositor awareness programmes, and keeps close liaison with the law enforcing agencies (Economic Offences Wing).

Before investing in schemes that promise high rates of return, the depositors/ investors must ensure that the entity offering such returns is registered with one of the Financial Sector Regulators and is authorized to accept funds, whether in the form of deposits or otherwise. Depositors/ investors must generally be circumspect if the interest rates or rates of return on deposits/ investments offered are high. Unless the entity accepting funds is able to earn more than what it promises, the entity will not be able to repay the depositor/ investor as promised. For earning higher returns, the entity will have to take higher risks on the investments it makes. Higher the risk, the more speculative would be its investments on which there can be no assured return. As such, members of public should forewarn themselves that the likelihood of losing money in schemes that offer high rates of interest are more.

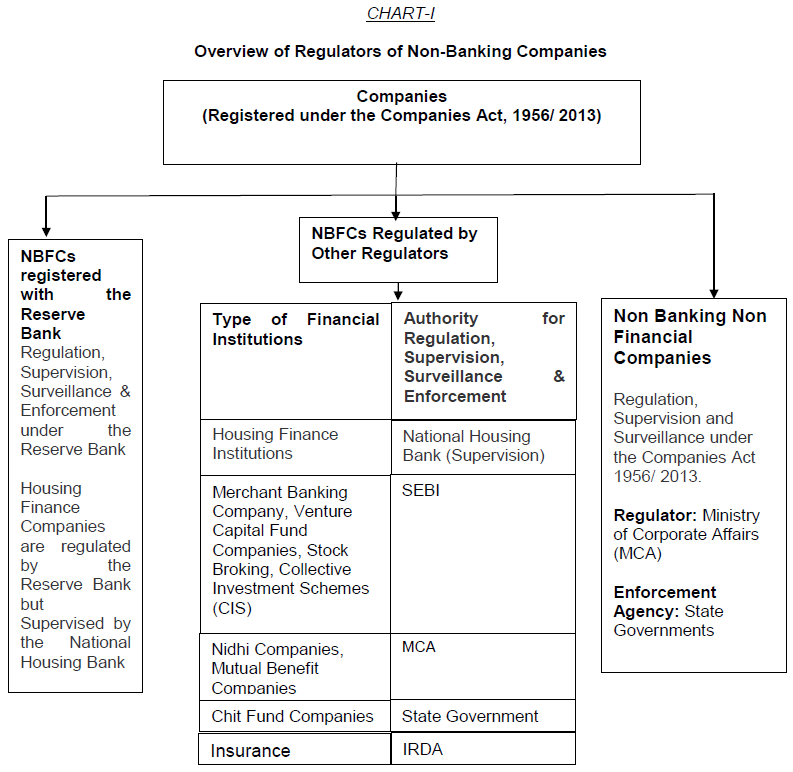

The two Charts given at Annex I and Annex II depict the activities and the regulators overseeing the same. Further, The First Schedule of the ‘The Banning of Unregulated Deposit Schemes Act, 2019’ may be referred for the list of regulated deposit schemes.

Complaints may hence be addressed to the concerned regulator. If the activity is a banned activity, the aggrieved person can approach the State Police/Economic Offences Wing of the State Police and lodge a suitable complaint.

H. Other/ miscellaneous aspects

Commercial Real Estate (CRE) would consist of loans to builders/ developers/ others for creation/ acquisition of commercial real estate (such as office building, retail space, multi-purpose commercial premises, multi-tenanted commercial premises, industrial or warehouse space, hotels, land acquisition, development and construction etc.) where the prospects for repayment, or recovery in case of default, would depend primarily on the cash flows generated by the asset by way of lease/rental payments, sale etc. Further, loans for third dwelling unit onwards to an individual will be treated as CRE exposure. Exposure shall also include non-fund based limits.

Commercial Real Estate – Residential Housing (CRE–RH) is a sub-category of CRE that consist of loans to builders/ developers for residential housing projects (except for captive consumption). Such projects should ordinarily not include non-residential commercial real estate. However integrated housing project comprising of some commercial spaces (e.g., shopping complex, school etc.) can also be specified under CRE-RH, provided that the commercial area in the residential housing project does not exceed 10 percent of the total Floor Space Index (FSI) of the project. In case the FSI of the commercial area in the predominantly residential housing complex exceed the ceiling of 10 percent, the entire loan should be classified as CRE and not CRE-RH.

No, the group requires to consolidate total assets of only those NBFCs which have been granted Certificate of Registration by the Bank. However, in case unregistered CICs in the group with asset size below ₹100 crore have accessed public funds, the asset size of such CICs shall be consolidated for the above purpose, but it would not change the status of unregistered CICs.

Loans against units of mutual funds (except units of exclusively debt oriented mutual funds) would attract LTV requirements as applicable to loans against shares. Further, the LTV requirement for loans/ advances against units of exclusively debt-oriented mutual funds may be decided by individual NBFCs in accordance with their loan policy.

In this case prior written approval of the Reserve Bank is to be obtained by the NBFC ‘A’. In case NBFC ‘A’ would cease to exist after the merger, the Certificate of Registration shall be surrendered for cancellation. Where ‘B’ is an NBFC, as a result of merger if there is change in control in ‘B’, or change in shareholding pattern of paid-up equity capital of ‘B’ by 26% or more, or change in management in ‘B’ which would result in change in more than 30% of the directors (excluding independent directors), prior written approval of the Reserve Bank is required. If ‘B’ is not an NBFC but is likely to meet Principal Business Criteria (i.e., 50-50 criteria) post-merger, it would also need to approach the Reserve Bank for prior written approval as well as registration as an NBFC.

Where a non-NBFC mergers with an NBFC, prior written approval of the Reserve Bank would be required if such a merger satisfies any one or all of the conditions viz., (i) any change in control in the NBFC due to merger, (ii) any change in the shareholding of the NBFC consequent to the merger which would result in change in shareholding of 26% or more of the paid up equity capital of the NBFC, (iii) any change in the management of the NBFC which would result in change in more than 30% of the directors, excluding independent directors. It may be noted that the NBFC shall continue to fulfil the Principal Business Criteria (i.e., 50-50 criteria) after merger to be eligible to hold the Certificate of Registration as an NBFC.

The NBFCs being amalgamated will require to obtain prior written approval of the Reserve Bank. Depending upon the nature of amalgamation/merger proposal, requisite approvals as per regulations needs to be sought.

Yes, prior approval of the Reserve Bank would have to be obtained before approaching any Court or Tribunal seeking orders for merger/ amalgamation involving NBFCs, including all such cases which would ordinarily fall under the scenarios explained in FAQs 84, 85 or 86.

Disclaimer: These FAQs are issued by the Reserve Bank for information and general guidance purposes only. The Reserve Bank will not be held responsible for actions taken and/or decisions made on the basis of the same. For clarifications or interpretations, if any, one may be guided by the relevant circulars and notifications issued from time to time.

| Related Press Release | |

| May 31, 2013 | Check before Depositing Money with Financial Entities: RBI Advisory |

ରିଜର୍ଭ ବ୍ୟାଙ୍କ ଅଫ୍ ଇଣ୍ଡିଆ ମୋବାଇଲ୍ ଆପ୍ଲିକେସନ୍ ଇନଷ୍ଟଲ୍ କରନ୍ତୁ ଏବଂ ଲାଟେଷ୍ଟ ନିଉଜ୍ କୁ ଶୀଘ୍ର ଆକ୍ସେସ୍ ପାଆନ୍ତୁ!