IST,

IST,

Monetary Policy Report – April 2024

|

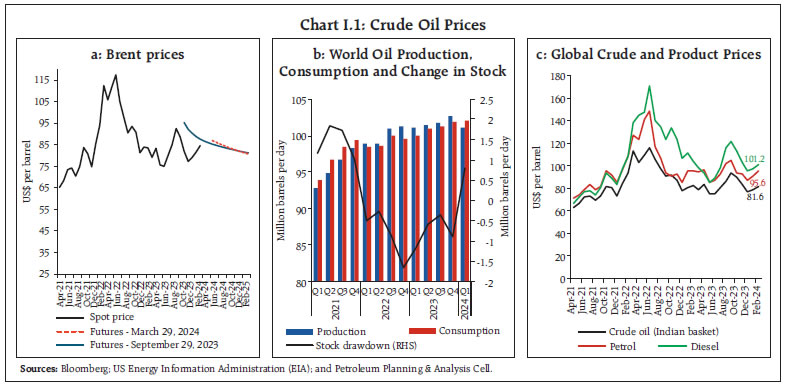

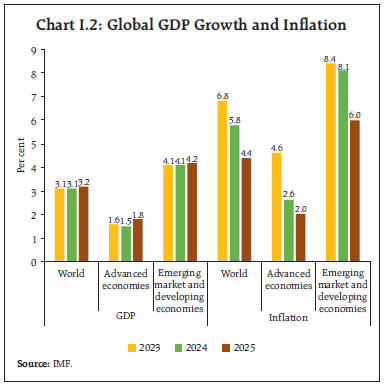

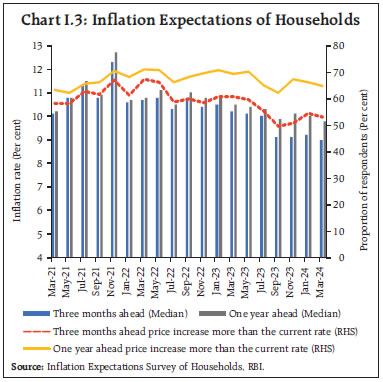

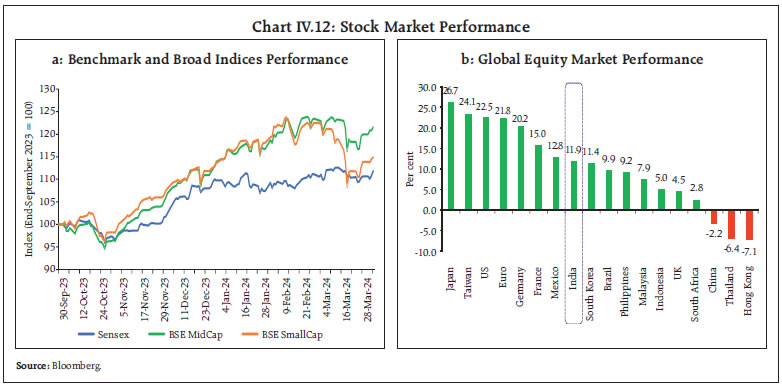

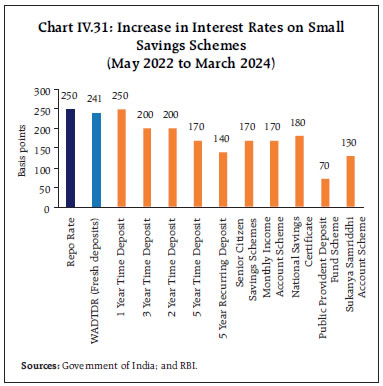

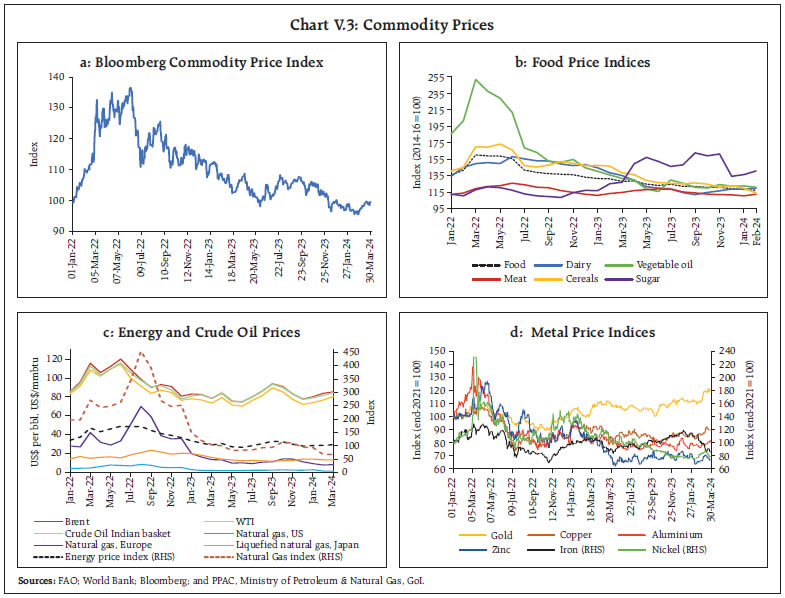

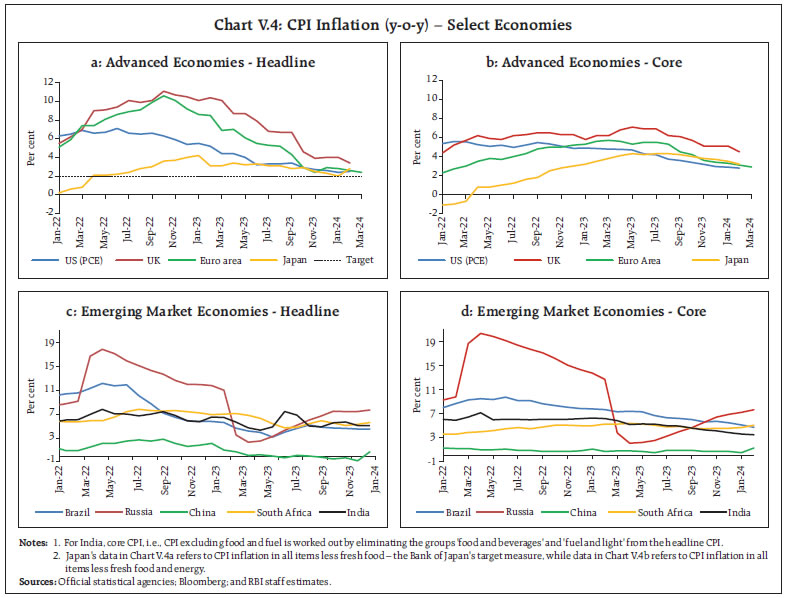

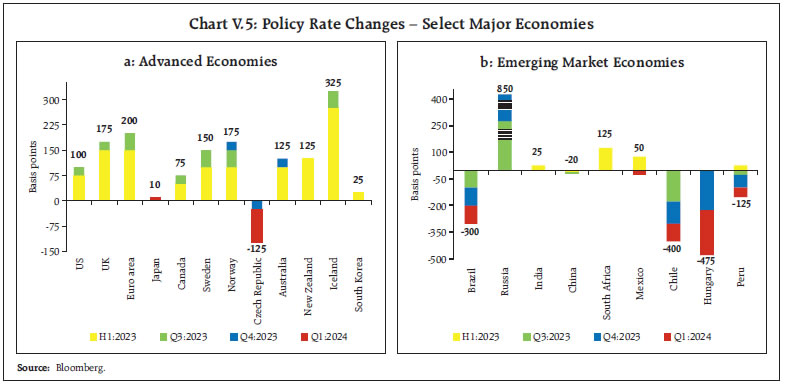

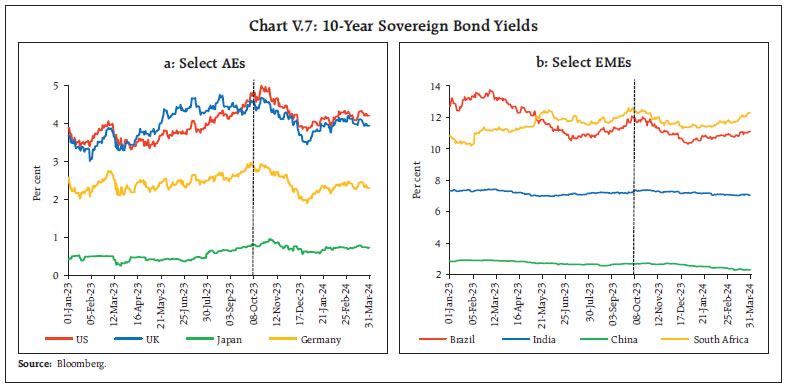

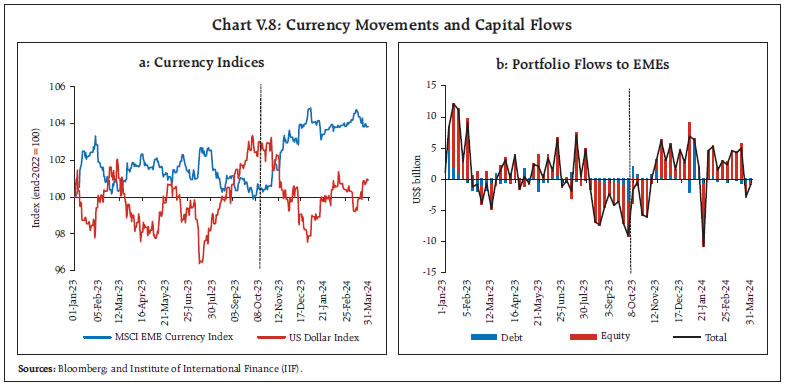

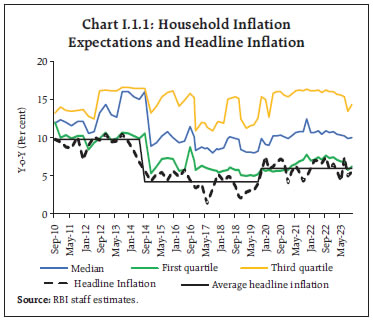

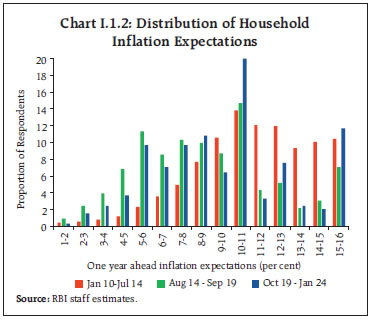

The outlook for domestic economic activity remains resilient on the back of strong domestic demand and improved macroeconomic fundamentals. Volatile food prices interrupt the path of disinflation and cloud the inflation outlook. Geopolitical hostilities, volatile global financial markets and climate shocks are the key risks to the outlook. Monetary policy remains focused on aligning inflation with the target to pave the path for sustained growth in the medium-term. I.1 Key Developments since the October 2023 MPR The global economy has remained surprisingly resilient despite repeated and overlapping shocks and unprecedented monetary tightening. Growth in the US and several major emerging market economies (EMEs) has held up better than expected. Sectorally, manufacturing activity has remained subdued, but services have exhibited strength. Headline inflation has come down across countries although the descent in core and services inflation has been slow amidst continuing tightness in labour markets. Major central banks in advanced economies (AEs) have kept policy rates on hold to ensure the aligning of inflation with targets. Incoming data on the economic outlook and evolving expectations about monetary policy’s trajectory in AEs reverberated through global financial markets imparting high volatility. A faster-than-expected decline in inflation fuelled expectations of an early reversal in the US monetary policy cycle, leading to a sharp correction in sovereign bond yields in November and December 2023. Yields have, however, hardened since the beginning of 2024 as central bank communication pushed back on market exuberance related to the magnitude and pace of monetary policy easing. Following the correction seen in Q3:2023 (July-September), global equity markets posted strong gains in November-December, primarily in AEs. The US dollar (US$) depreciated to a 6-month low at end-December but recovered subsequently on stronger-than-expected US economic data. Crude oil prices declined during October-December 2023 on slowing global demand and improved supply from countries outside of organization of the petroleum exporting countries (OPEC) but recovered thereafter in the wake of supply disruptions in key shipping routes and extension of production cuts by OPEC plus through June 2024. Food prices eased with the decline in prices of cereals, meat and vegetable oils, although sugar prices have firmed up. Turning to the domestic economy, the second advance estimates (SAE) released by the National Statistical Office (NSO) placed real gross domestic product (GDP) growth for 2023-24 at 7.6 per cent, underpinned by strong investment activity. On the supply side, gross value added (GVA) expanded by 6.9 per cent in 2023-24, with manufacturing and services sectors turning out to be the key drivers. Real GDP growth for Q3:2023-24 was placed at 8.4 per cent, outpacing consensus forecasts by a wide margin, underpinned by strong investment and an improvement in private consumption. Headline CPI inflation moderated to 5.3 per cent in October 2023-February 2024 from an average of 5.5 per cent in H1:2023-24. Sporadic food price shocks continued to impart significant volatility to the inflation trajectory, with headline inflation rising sharply in November and December 2023 due to a spike in vegetable prices. Core inflation (i.e., CPI excluding food and fuel) has, however, been on a steadily declining path. In February 2024, it fell to 3.4 per cent, among the lowest prints in the current CPI series (2012=100), driven by both core goods and services components. With the cumulative rate hike of 250 basis points (bps) undertaken during May 2022-February 2023 working its way through the economy, the Monetary Policy Committee (MPC) kept the policy repo rate unchanged at 6.50 per cent through H2 and remained resolute in its commitment to align inflation with the target, keeping in mind the objective of growth. Monetary Policy Committee Meetings: October 2023 – March 2024 When the MPC met in October 2023, global growth and trade were losing momentum, inflation was easing gradually but remained well above targets in major economies. Concerns about higher for longer interest rates were keeping financial conditions tight and imparting volatility to global financial markets. Domestically, CPI headline inflation rose sharply in July 2023 on the back of a spike in vegetable prices while core inflation softened. The projection of CPI inflation for 2023-24 was retained at 5.4 per cent as the spurt in vegetable prices was expected to be transitory. Domestic economic activity was showing resilience despite external headwinds. The real GDP growth projection for 2023-24 was retained at 6.5 per cent. The MPC observed that the unprecedented food price shocks were impinging on the evolving trajectory of inflation and that recurring incidence of such overlapping shocks could impart generalisation and persistence. Accordingly, the MPC unanimously decided to keep the policy repo rate unchanged at 6.50 and, by a majority of 5-1, voted to remain focused on the stance of withdrawal of accommodation to ensure that inflation progressively aligns with the target, while supporting growth. At the time of the December 2023 meeting, receding global inflation was engendering expectations of a reversal in the monetary policy cycle in AEs. Market sentiments improved amidst declining sovereign bond yields, a depreciating US dollar and strengthening global equity markets. In India, CPI headline inflation had fallen to 4.9 per cent (October 2023 print) from an average of 6.4 per cent during the previous quarter (July-September 2023). Furthermore, core inflation had moderated to levels last seen in Q4:2019-20. Domestic economic activity exhibited resilience, with real GDP growing by 7.6 per cent in Q2:2023-24, driven by robust investment and government consumption. The projection of real GDP growth for 2023-24 was revised up to 7.0 per cent while that of inflation was retained at 5.4 per cent. The MPC observed that recurring food price shocks were impeding the ongoing disinflation process and monetary policy needed to remain actively disinflationary to ensure anchoring of inflation expectations and fuller transmission. Against this backdrop, the MPC unanimously voted to keep the policy repo rate unchanged at 6.50 per cent and voted with a 5-1 majority to continue with the stance of withdrawal of accommodation. In the run up to the February 2024 meeting, headline CPI inflation had picked up to 5.7 per cent in December 2023, led primarily by an increase in vegetable price inflation, even as deflation in fuel prices deepened. Core inflation had softened to a four-year low of 3.8 per cent in December. Assuming a normal monsoon, CPI inflation was projected to decline to 4.5 per cent in 2024-25 from 5.4 per cent in 2023-24. Domestic economic activity was strengthening, with the first advance estimates (FAE) released by the NSO placing year-on-year (y-o-y) GDP growth at 7.3 per cent for 2023-24, underpinned by strong investment activity. Real GDP growth was projected at 7.0 per cent for 2024-25. The MPC noted that considerable uncertainty prevailed on the food price outlook from the possibility of adverse weather events. Upside risks to inflation also emanated from geopolitical developments and their impact on supply chains, volatility in international financial markets and uncertainty around commodity prices. The MPC decided by a majority of 5-1 to keep the policy repo rate unchanged at 6.50 per cent while retaining the stance of withdrawal of accommodation. The MPC’s voting pattern reflects the diversity in individual members’ assessments, expectations and policy preferences – a characteristic also reflected in voting patterns of other central banks (Table I.1). With the economic outlook diverging across countries, central banks’ policy rate decisions have become increasingly asynchronous. Central banks of Brazil and Chile, which tightened policy earlier, have reduced their policy rates since the second half of 2023 in response to declining inflation and in support of economic activity. On the other hand, Japan raised its benchmark policy rate for the first time in 17 years in March, ending eight years of negative interest rates. Macroeconomic Outlook Chapters II and III analyse macroeconomic developments relating to inflation and economic activity during H2:2023-24 (October 2023 - March 2024). Turning to the baseline assumptions, international crude prices exhibited sizeable two-way movements in H2, falling in October-December 2023 to around US$75 per barrel on slowing global demand amidst weak manufacturing activity and easing demand for transportation fuels as well as supply increases from non-OPEC countries. Amidst intensifying hostilities in the Middle-East, deep output cuts by OPEC plus, and incidents of supply outages, international crude prices moved higher from mid-December reaching an average close to US$ 85 per barrel in March. Geopolitical tensions imparted significant uncertainty to the outlook (Charts I.1a and I.1b). The spread between global petroleum product prices and crude prices eased from its recent peaks in mid-2022 but remains elevated by historical standards in view of demand-supply refinery mismatches (Chart I.1c). Taking into account these factors, the baseline assumption for crude price (Indian basket) is retained at US$ 85 per barrel (Table I.2).  Second, the nominal exchange rate of the Indian rupee (₹) saw two-way movements in the range of ₹82.8-83.4 per US dollar in H2. Taking into consideration the uncertainty around US dollar movements, the ebbs and flows of global capital flows and international crude oil prices, the baseline assumption for the exchange rate is revised to ₹83 per US dollar. Third, the global growth forecast for 2024 was revised upwards by 20 bps to 3.1 per cent by the International Monetary Fund (IMF) in its January 2024 update of the World Economic Outlook (WEO) from its October 2023 projection. Global growth is expected to increase marginally to 3.2 per cent in 2025 (Chart I.2). Global trade growth (goods and services combined) is projected to accelerate from 0.4 per cent in 2023 to 3.3 per cent in 2024 and further to 3.6 per cent in 2025. Global GDP growth for 2024 and 2025 is expected to trail its historical (2000-19) average of 3.8 per cent as multiple headwinds – tighter monetary policy; withdrawal of fiscal stimulus given debt sustainability challenges; reduced pent-up demand; financial stability risks; continued geopolitical challenges; and geoeconomic fragmentation – weigh on prospects. Inflation is projected to decline in most regions in 2024 – more rapidly in AEs vis-à-vis EMEs – amidst unwinding of supply-side pressures, restrictive monetary policy, easing labour markets and the pass-through of earlier declines in energy prices. In H2, movements in headline inflation were driven by fluctuations in food prices even as core inflation witnessed a sustained decline (Chapter II). In the March 2024 round of the Reserve Bank’s inflation expectations survey1, both the three months and one year ahead median inflation expectations of urban households decreased by 20 bps vis-à-vis the previous round. Concomitantly, the proportion of respondents expecting the general price level to increase by more than the current rate decreased for both horizons vis-à-vis the previous round (Chart I.3). The distributional characteristics of inflation expectations contain useful forward-looking information about future inflation (Box I.1).

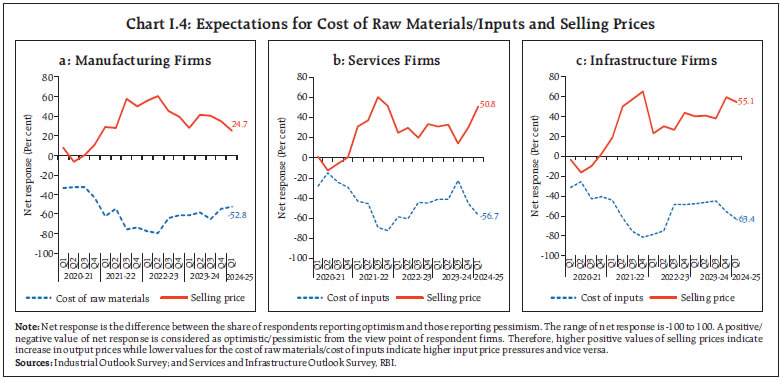

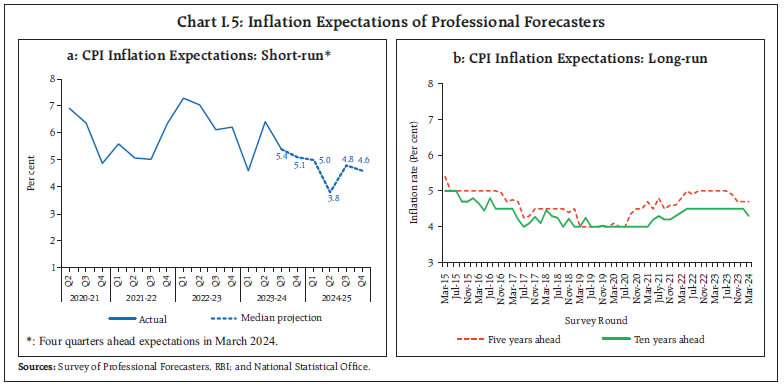

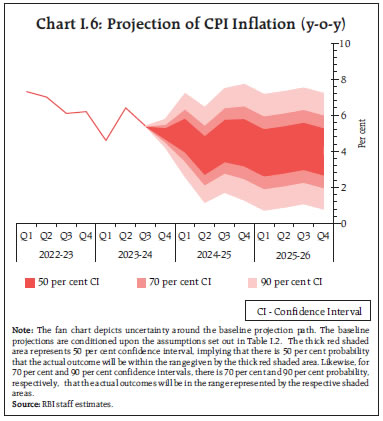

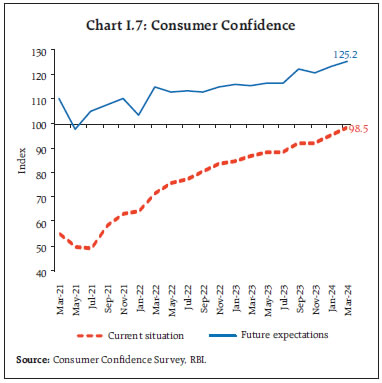

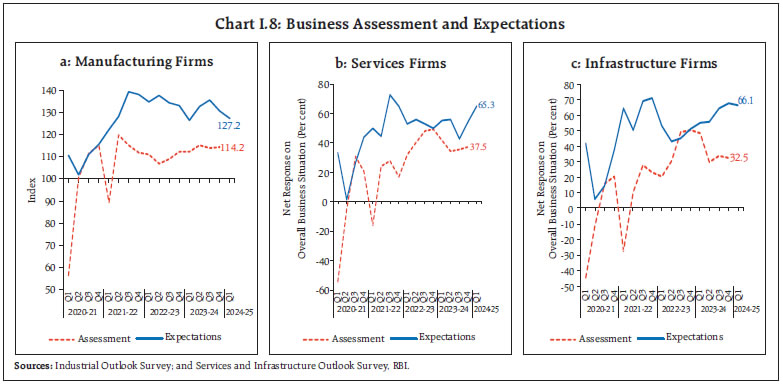

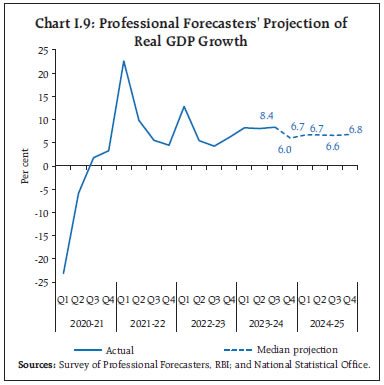

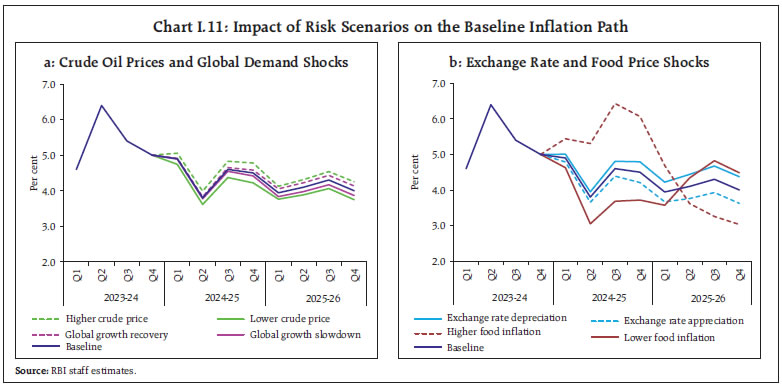

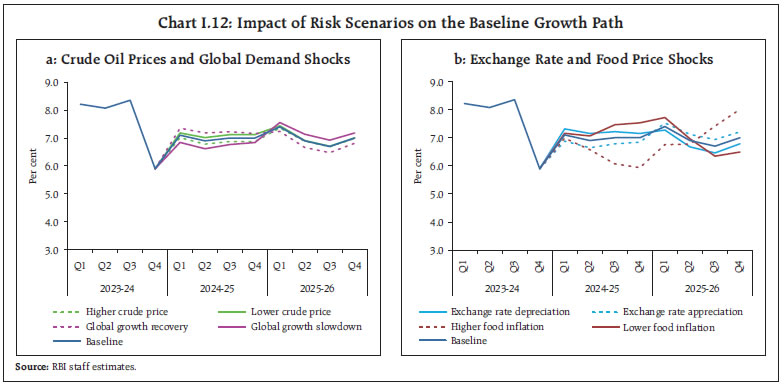

Manufacturing firms polled in the January-March 2024 round of the Reserve Bank’s industrial outlook survey expect easing in cost pressures from raw materials as well as selling prices in Q1:2024-25 vis-à-vis the previous round (Chart I.4a).3 In contrast, services sector companies expect higher input cost pressures and growth in selling prices in Q1:2024-25, while infrastructure firms expect higher input cost pressures but lower growth in selling prices (Charts I.4b and I.4c).4 In the PMI surveys, manufacturing firms reported increased input cost pressures but slower output price increases in March 2024. Services firms reported higher input and output prices, with a marked increase in the rate of inflation in March 2024. Professional forecasters surveyed by the Reserve Bank in March 2024 expected headline CPI inflation to moderate from 5.4 per cent in Q3:2023-24 to 5.1 per cent in Q4, 5.0-3.8 per cent in H1:2024-25, and 4.8-4.6 per cent in H2 (Chart I.5a and Table I.3).5 They expected core inflation (i.e., CPI excluding food and beverages, pan, tobacco and intoxicants, and fuel and light) at 3.4 per cent in Q4:2023-24 and Q1:2024-25, increasing progressively to 3.7 per cent in Q2, 4.1 per cent in Q3, and 4.3 per cent in Q4. Their 5-year ahead inflation expectations remained unchanged at 4.7 per cent, while their 10-year ahead inflation expectations declined by 20 bps to 4.3 per cent in the March 2024 round from the previous round (Chart I.5b).   Looking ahead, the outlook for inflation will be contingent largely on the evolving food inflation dynamics. Rabi sowing has exceeded last year’s levels, but pulses have witnessed a decline. According to the second advance estimates, the production of cereals, pulses and oilseeds has trailed last year’s level. Water reservoir levels remain significantly below the level of last year and of the decadal average. Vegetable prices are undergoing seasonal correction unevenly. The continuing pass-through of monetary policy actions and stance, on the other hand, is keeping core inflation subdued. Adverse weather events and continuing geopolitical hostilities, however, remain the key risks. Taking into account the initial conditions, signals from forward-looking surveys and estimates from time-series and structural models6, CPI inflation is projected to average 4.5 per cent in 2024-25 – 4.9 per cent in Q1, 3.8 per cent in Q2, 4.6 per cent in Q3 and 4.5 per cent in Q4, with risks evenly balanced (Chart I.6). The 50 per cent and the 70 per cent confidence intervals for headline inflation in Q4:2024-25 are 3.2–5.8 per cent and 2.5–6.5 per cent, respectively. For 2025-26, assuming a normal monsoon and no further exogenous or policy shocks, structural model estimates indicate that inflation will average 4.1 per cent, in a range of 3.9–4.3 per cent. In Q4:2025-26, CPI inflation is projected at 4.0 per cent, with the 50 per cent and the 70 per cent confidence intervals at 2.7–5.3 per cent and 2.0–6.0 per cent, respectively.  These baseline forecasts are subject to several upside and downside risks. The upside risks emanate from persistent food price pressures from extreme weather-related disturbances; an escalation in geopolitical hostilities which could further aggravate supply disruptions; increased volatility in prices of key commodities, particularly crude oil; and a larger pass-through of input cost pressures to output prices as demand gains strength. The downside risks emanate from an early resolution of geopolitical conflicts; a pronounced slowdown in the global demand with further easing of global commodity prices; and an improvement in supply responses of key primary commodities. Domestic economic activity is supported by an upturn in the investment cycle on the back of the government’s continued thrust on capital expenditure, higher capacity utilisation, underlying resilience of the services sector, double digit credit growth, and healthier corporate and bank balance sheets. Escalating geopolitical tensions, new flashpoints choking arterial routes of global trade, and volatile global financial conditions, however, impart uncertainty to the outlook.  Turning to the key messages from forward-looking surveys, consumer confidence of urban households (the current situation index) improved further in the March 2024 survey round vis-à-vis the previous round, reaching closer to the neutral level on the back of improved perceptions on general economic conditions and the employment situation. Consumers’ future outlook—for the year ahead—continued in optimistic territory and registered a new peak since the onset of the pandemic, propelled by improvement in all parameters (Chart I.7).7 In the Reserve Bank’s industrial outlook survey of January-March 2024, manufacturing firms were optimistic on the business outlook during Q1:2024-25, albeit with waning sentiments from the previous round (Chart I.8a). Services and infrastructure companies remained upbeat on the overall business situation in Q1:2024-25, though with some moderation in sentiments for the latter (Charts I.8b and I.8c).  Recent surveys by other agencies generally reported sequential improvement in business expectations relative to the previous round (Table I.4). Manufacturing and services firms in the latest PMI surveys exhibited optimism for the year ahead. Professional forecasters polled in the March 2024 round of the Reserve Bank’s survey expected real GDP growth at 6.0 per cent in Q4:2023-24, 6.7 per cent in H1:2024-25, and 6.6-6.8 per cent in H2 (Chart I.9 and Table I.3). Overall, the outlook for growth is improving on the back of domestic drivers of demand, although persisting uncertainties on the global front pose risks to the outlook. Taking into account the baseline assumptions, survey indicators and model forecasts, real GDP growth is expected at 7.0 per cent in 2024-25 – 7.1 per cent in Q1; 6.9 per cent in Q2; and 7.0 per cent each in Q3 and Q4 - with risks evenly balanced around this baseline path (Chart I.10 and Table I.3). For 2025-26, assuming a normal monsoon and no major exogenous or policy shocks, structural model estimates indicate real GDP growth at 7.0 per cent, with quarterly growth rates in the range of 6.7-7.4 per cent.  There are upside and downside risks to this baseline growth path. The upsides emanate from a stronger growth in the manufacturing and services sectors sustained by strong domestic demand; upbeat business optimism; accelerated private investment spurred by government’s continued capex push; an early resolution of geopolitical conflicts; faster disinflation; and improvement in global trade and supply chains. On the contrary, further escalation in geopolitical tensions and geoeconomic fragmentation; unexpected spurts in global commodity prices; increased volatility in international financial markets; deceleration in global trade and demand; and frequent weather-related disturbances due to climate change pose downside risks to the baseline growth path.   The projections of growth and inflation presented in this chapter are, inter alia, conditioned on the assumptions set out in Table 1.2. These are subject to uncertainties on the global growth outlook, crude oil prices, exchange rate and food prices. Against this backdrop, this section explores the alternative scenarios to assess the balance of risks to the baseline projections. (i) Global Growth Uncertainties Global economic activity moderated in H2:2023 but remained more robust than anticipated earlier. With inflation declining and growth holding firm, the likelihood of a soft landing has increased for the global economy. There are, however, downside risks, going forward. The escalation in geopolitical tensions in West Asia hampering shipping through the Suez Canal and resultant supply disruptions could keep inflation elevated, delaying the easing of monetary conditions. Furthermore, if the last mile of disinflation turns out to be protracted, it may require interest rates to remain higher for longer thereby posing considerable downside risks to growth. At high risk are less developed economies with relatively elevated debt-to-GDP ratio. Rising trade distortions and geoeconomic fragmentation could also weigh on global trade and growth. All these factors can pull down global growth well below the baseline. In such a scenario, if global growth is 100 bps lower than the baseline, domestic growth and inflation could be around 30 bps and 15 bps, respectively, below their baseline trajectories. Conversely, on the upside, a faster disinflation could allow monetary authorities to reduce policy rates earlier than anticipated, easing financial conditions further, improving sentiments and providing a fillip to global growth. Further, a greater push for supply-side reforms and harnessing of new technologies such as artificial intelligence could provide a boost to productivity, global growth and demand. In this scenario, if global growth is higher by 50 bps, domestic growth and inflation could edge higher by around 15 bps and 7 bps, respectively (Charts I.11a and I.12a). (ii) International Crude Oil Prices Global crude oil prices have remained highly volatile, with Brent crude falling from a high of US$ 95 in early October 2023 to below US$ 75 by mid-December, before rebounding and settling above US$ 80 in the first quarter of 2024. An escalation in the conflict in West Asia and logistical impediments in key trade routes may cause serious disruptions in the oil market. Assuming crude oil price to be 10 per cent above the baseline, domestic inflation could be higher by 30 bps and growth weaker by around 15 bps, respectively. Conversely, de-escalation of geopolitical tensions along with a further weakening of global demand may pull down crude oil prices. If crude oil prices fall by 10 per cent relative to the baseline and assuming their full pass-through to the domestic product prices, inflation could ease by around 30 bps with a boost of 15 bps to India’s real GDP growth (Charts I.11a and I.12a).  (iii) Exchange Rate In H2, the Indian Rupee (INR) moved bi-directionally against the US dollar. Looking ahead, a ‘higher for longer’ interest rate scenario could keep risk aversion towards EME assets elevated, impinging upon capital flows. Concerns around public debt in EMEs, particularly in those with large foreign currency debt, could induce flight to safety and a broad-based depreciation of EME currencies. Crude oil and other commodity prices could harden over the baseline. Should the INR depreciate by 5 per cent from the baseline assumption, inflation could edge up by around 35 bps while GDP growth could be higher by around 25 bps through stimulating exports. On the other hand, the Indian economy remains the fastest growing large economy in the world and is pivotal to the global outlook. Sustained global disinflation and the accompanying scenario of monetary easing in AEs along with the strengthening of domestic macroeconomic fundamentals and the inclusion of government bonds in global indices could enhance India’s attractiveness as a destination for foreign investors. In this scenario, if the INR appreciates by 5 per cent relative to the baseline, inflation and GDP growth could moderate by around 35 bps and 25 bps, respectively (Chart I.11b and I.12b).  (iv) Food Inflation Food inflation exhibited sizeable volatility in H2:2023-24, driven by large shocks to vegetable prices. Erratic rainfall and deficient soil moisture hindered rabi sowing, although the effect was uneven across crops and regions. While crops such as wheat, oilseeds and coarse cereals witnessed an increase in acreage, area sown under pulses declined by over 6 lakh hectares year-on-year. Water reservoir levels have dipped below the decadal average. According to the SAE, production of cereals, pulses and oilseeds in 2023-24 was lower than a year ago. These developments impart uncertainty to the outlook on food prices. The global food price outlook is also subject to significant upside risks from the historically unprecedented heat wave sweeping across the globe. The India Meteorological Department (IMD) has forecast above-normal temperatures and heatwave days during the summer season. Climate change has increased the frequency and ferocity of weather shocks, posing challenges for monetary policy (Box I.2). All these developments could impart upside risk to the domestic food inflation trajectory and could raise headline inflation by around 100 bps over the baseline. On the other hand, ample foodgrains buffer stocks and effective supply management could help ease food inflationary pressures and pull headline inflation 50 bps below the baseline.

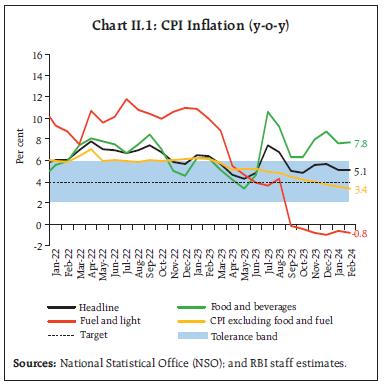

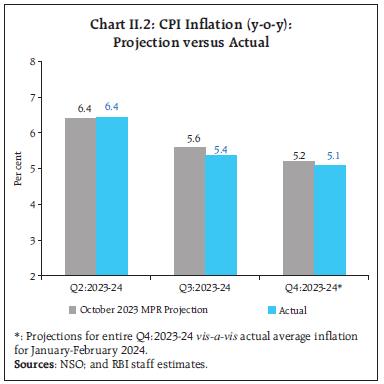

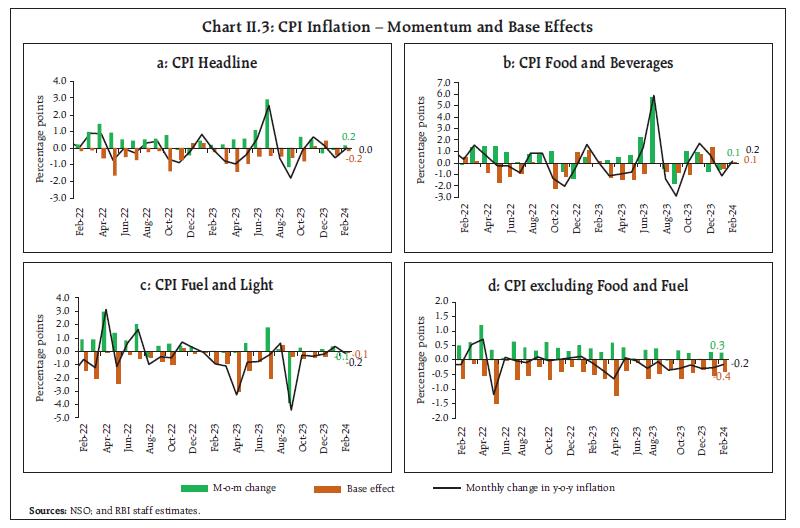

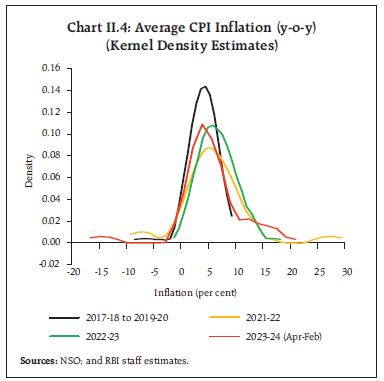

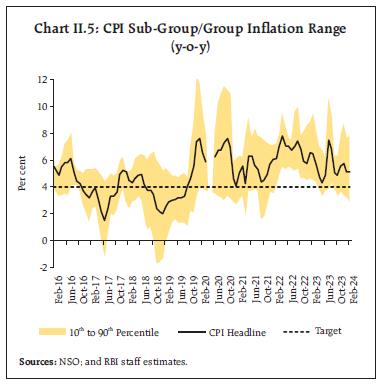

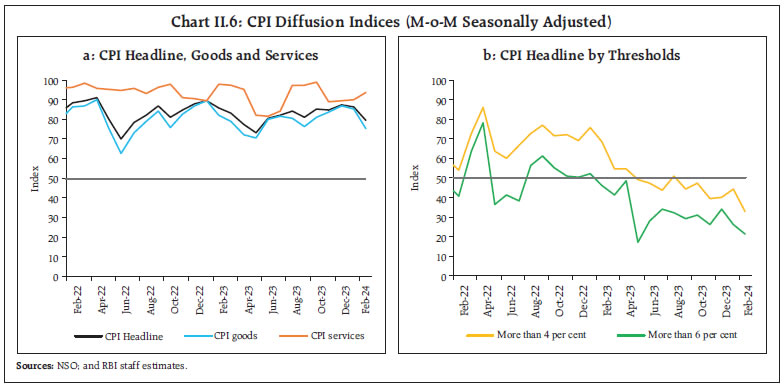

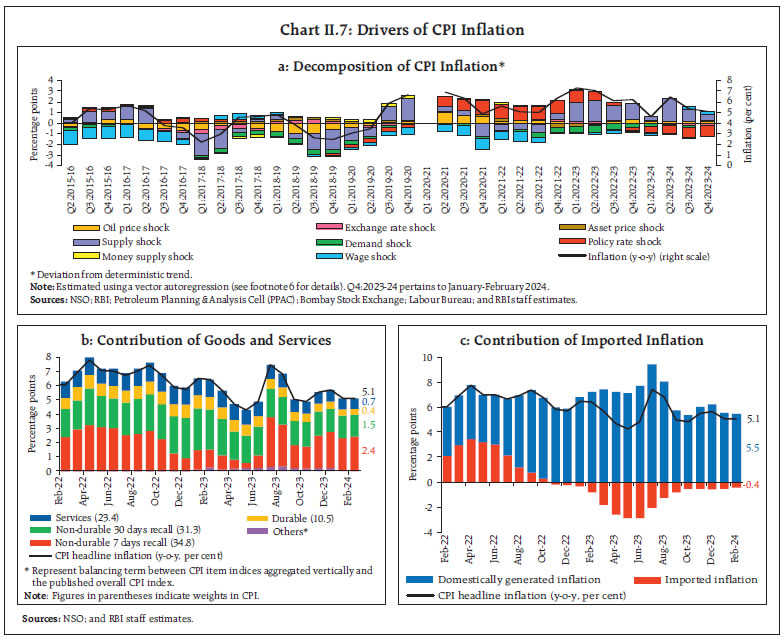

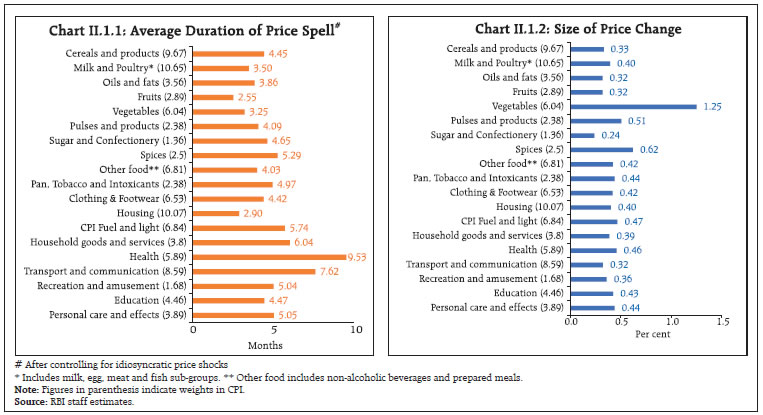

Amidst global challenges, the Indian economy has stayed resilient. Buoyed by strong domestic demand and backed by robust macroeconomic fundamentals, India has emerged as the fastest growing major economy of the world in 2023-24. The upturn in the investment cycle, broad-based revival in manufacturing and services sectors, government’s capex push, upbeat business and consumer sentiments and strong corporate and bank balance sheets provide impetus to the growth momentum going forward. Volatile food prices, however, interrupt the path of disinflation and cloud the inflation outlook. The continuing effect of monetary policy action and stance is keeping core inflation muted. Spillovers from geopolitical hostilities, volatile global financial markets and climate shocks are the key risks to the growth and inflation outlook. _________________________________________________________________________________ 1 The Reserve Bank’s inflation expectations survey of households is being conducted in 19 cities since March 2021 (18 cities in the previous rounds) and the results of the March 2024 round are based on responses from 6,083 households. 2 Unit level data on one year ahead inflation expectations from the survey of households conducted by the Reserve Bank has been used. The Bai-Perron (2003) test suggests breaks in headline CPI inflation in August 2014 and October 2019. 3 The results of the January-March 2024 round of the industrial outlook survey are based on responses from 1,354 companies. 4 Based on 587 services companies and 120 infrastructure firms polled in the January-March 2024 round of the services and infrastructure outlook survey. 5 45 panellists participated in the March 2024 round of the Reserve Bank’s survey of professional forecasters. 6 John, Joice, Deepak Kumar, Asish Thomas George, Pratik Mitra, Muneesh Kapur and Michael Debabrata Patra (2023), “A Recalibrated Quarterly Projection Model (QPM 2.0) for India”, Reserve Bank of India Bulletin, February. 7 The Reserve Bank’s consumer confidence survey is being conducted in 19 cities since March 2021 (13 cities in the previous rounds) and the results of the March 2024 round are based on responses from 6,083 respondents. Headline inflation has been on a moderating path during H2:2023-24 with resurgences in food price pressures interrupting the descent, even as core inflation softened across its goods and services components. Industrial and farm input price pressures remain muted, and nominal rural and organised sector wage growth stays steady. Going forward, the risks to the 'last mile' of disinflation process may emanate from incidence of unpredictable supply side shocks. Since August 2023, headline consumer price index (CPI) inflation1 has been on a moderating trajectory, troughing at 4.9 per cent in October 2023. A resurgence of food price pressures pushed it up to 5.7 per cent in December, despite steady core (CPI excluding food and fuel)2 disinflation and a deepening fuel price deflation. In January-February 2024, headline inflation eased to 5.1 per cent, with both food and core inflation easing and fuel prices remaining in deflation (Chart II.1). Notwithstanding the moderation, food inflation remained elevated. The softening of core inflation to 3.4 per cent in February, among the lowest prints in the current CPI series (2012=100), was broad based across its goods and services components.  The Reserve Bank of India (RBI) Act enjoins the RBI to set out deviations of actual inflation outcomes from projections, if any, and explain the underlying reasons thereof. The October 2023 MPR had projected inflation to edge down to 5.6 per cent in Q3:2023-24 and further to 5.2 per cent in Q4 (Chart II.2). Actual inflation at 5.4 per cent in Q3 and at 5.1 per cent in Q4 (January-February 2024) was lower than the projections by 20 basis points (bps) and 10 bps, respectively. The undershooting of inflation came about from food as well as core components. Proactive supply side interventions helped to contain the build-up of price pressures, especially in respect of onions, cereals and pulses. In the core component, the softening of services inflation, particularly under housing, turned out to be sharper than anticipated.  Headline inflation dynamics in H2:2023-24 were broadly shaped by the interplay between volatile food price momentum and base effects3. Favourable base effects and sharp negative price momentum – from a part reversal of the spike in vegetable prices in July, sharp decline in LPG prices and muted rise in core CPI prices – pulled down headline inflation from 6.8 per cent in August to 5.0 per cent in September. Thereafter, by November, headline inflation edged up on a significant pick-up in food price momentum and unfavourable base effects. Although the momentum turned negative in December, a strong unfavourable base effect, primarily from the food group, pushed up headline inflation further to 5.7 per cent. In January 2024, the decline in momentum, driven by correction in food prices along with favourable base effects, led to a softening of headline inflation to 5.1 per cent. It remained steady in February as a positive price momentum in food and core was evened out by favourable base effects from fuel and core groups (Chart II.3). A comparison of the distribution of CPI inflation in 2023-24 vis-à-vis 2022-23 indicates that a fall in the mean of the distribution to 5.4 per cent in 2023-24 (April-February) from 6.8 per cent in the corresponding period of 2022-23 coexisted with a marked increase in its standard deviation (Chart II.4). Furthermore, inflation variability across CPI remained high in H2 of 2023-24 (Chart II.5), attesting to the lingering impact of overlapping supply side shocks on the inflation formation process.    Headline CPI diffusion indices (DIs)4 remained elevated since August 2023, driven largely by CPI goods, with some moderation observed in February 2024. DI for CPI services corrected during November-December, but it registered a pick-up in January-February (Chart II.6a). Even as CPI DIs remained in the expansionary zone, threshold DI5 – for price increases in excess of 4 per cent as well as 6 per cent on a seasonally adjusted annualised rate (saar) basis – slipped further into the contractionary zone in H2:2023-24, indicating that a generalised and durable disinflation is underway in 2023-24 so far (Chart II.6b).  A historical decomposition of inflation using a vector autoregression (VAR)6 model indicates that the moderation in inflation in Q3:2023-24 and Q4 came from weakening of supply side shocks, especially in food prices from a spike in Q2, and from the transmission of past monetary policy actions (Chart II.7a). Price inflation in goods (with a weight of 76.6 per cent in overall CPI) contributed to around 80 per cent of headline inflation during August-December 2023 and services (with a weight of 23.4 per cent) contributed the remaining 20 per cent. By February 2024, the contribution of goods to overall inflation rose to around 86 per cent (Chart II.7b). Perishable items (non-durable with a 7-day recall7), which include vegetables, spices, fruits and other food items such as milk, meat and fish and prepared meals, contributed most to goods inflation variability. Among semi -perishables (non-durable goods with a 30-day recall), cereals, pulses, electricity, personal care items (like toiletries) and medicines were the main drivers of inflation. Broadly, the contribution of durables (goods with a 365-day recall) like clothing and footwear items, motorcycles/scooters and household goods (furniture and electronic items) to overall inflation came down from around 12 per cent during September-November 2023 to around 8 per cent in February 2024. Analysis of price setting behaviour suggests that after adjusting for idiosyncratic item-specific price shocks, economy wide price shocks tend to lead to more frequent change in food prices. Core prices tend to be stickier (Box II.1).

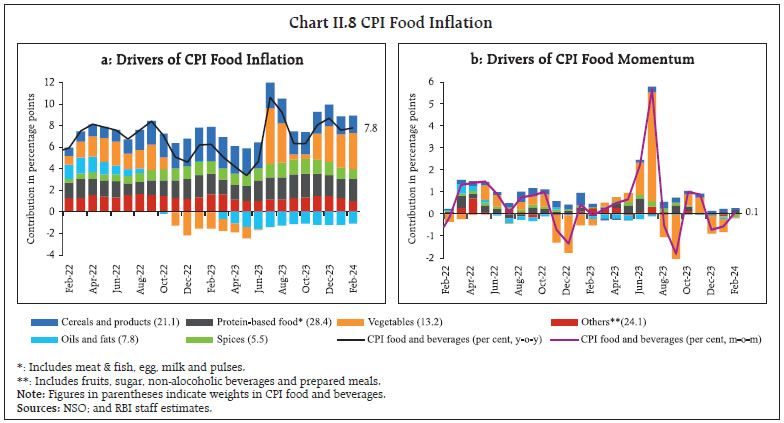

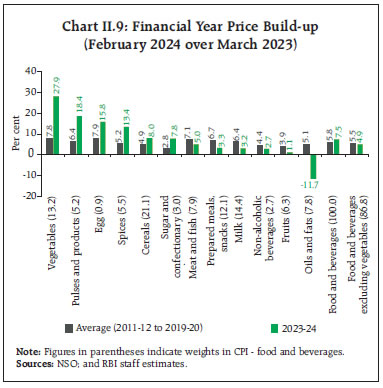

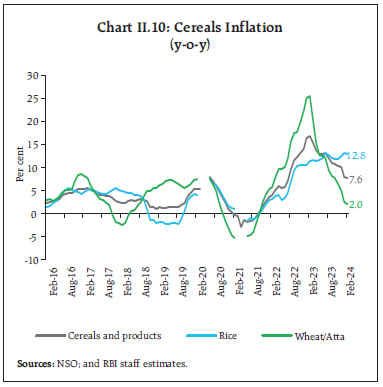

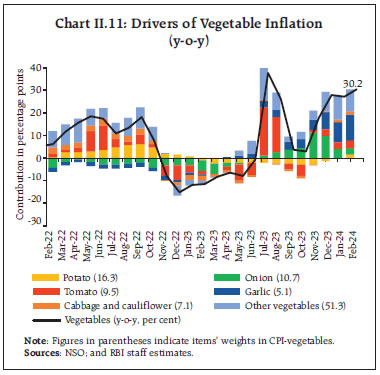

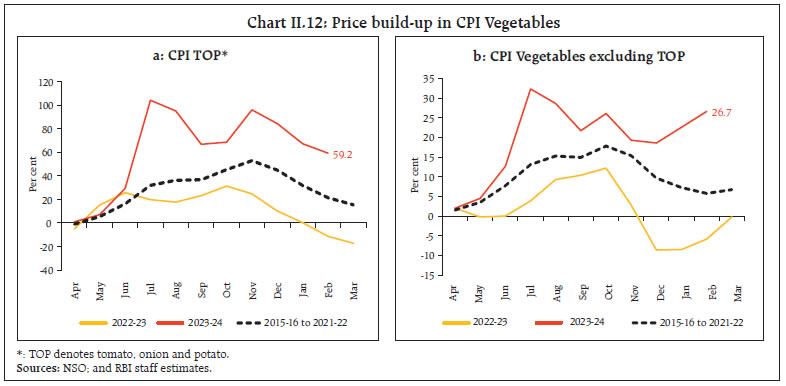

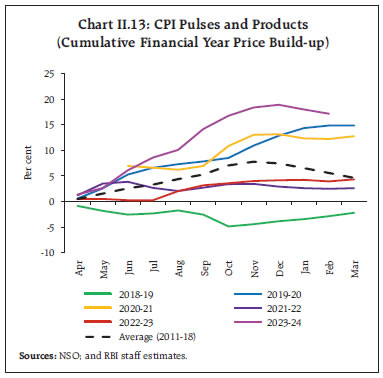

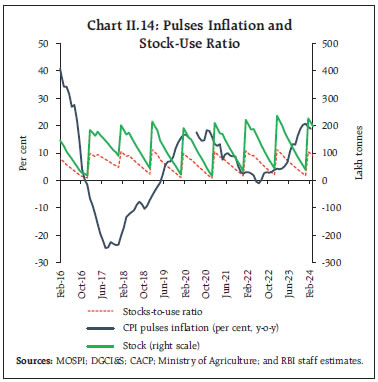

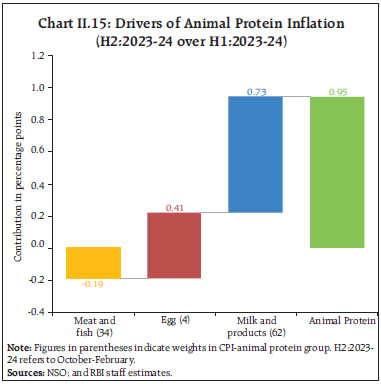

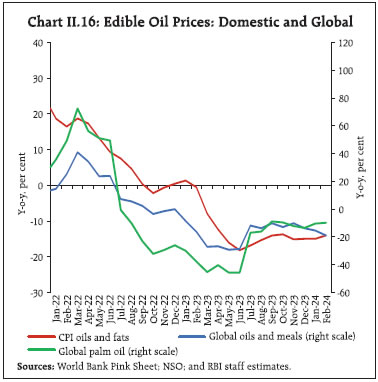

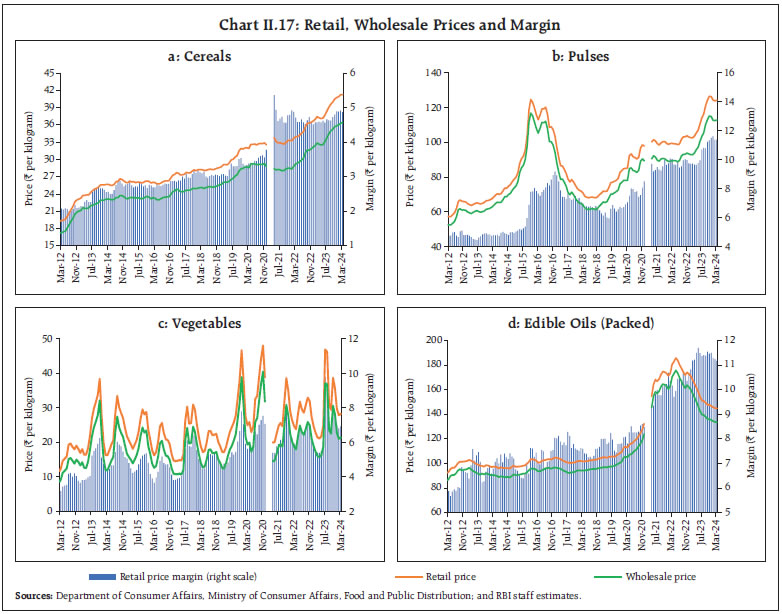

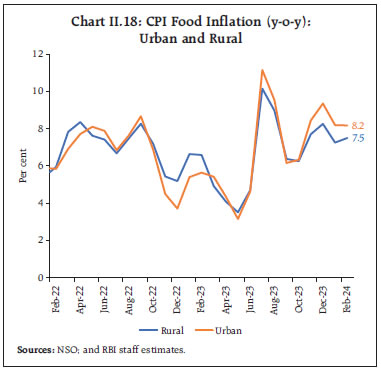

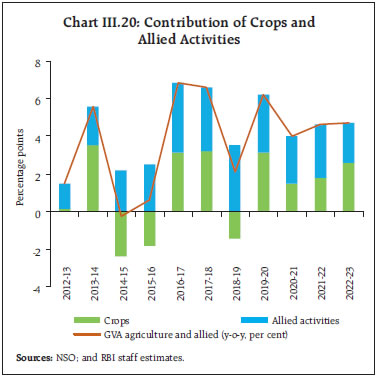

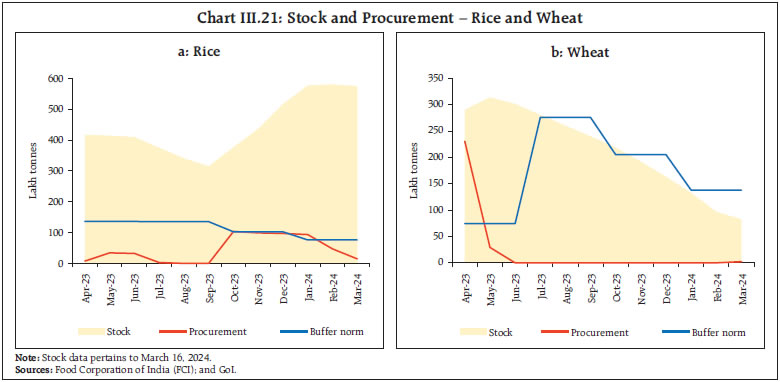

With the gradual moderation in international commodity prices since September 2022, the contribution of imported components11 to headline inflation turned negative from the end of 2022, driven by y-o-y decline in the prices of edible oils, energy, electronic goods parts and polymer (Chart II.7c). Deflation in international commodity prices of precious metals (gold; silver), energy (LPG; crude oil), palm kernel, electronic goods parts and polymer prices abated since July 2023; as a result, the contribution of imported inflation in pulling down headline inflation lessened to (-)0.5 percentage points in October 2023 from (-)2.9 percentage points in June 2023, and broadly remained stable thereafter. CPI Food Group Food and beverages (weight of 45.9 per cent in the CPI basket) inflation, which increased sharply in July-August 2023 due to a spike in vegetables prices caused by excess rainfall/floods and supply disruptions, moderated in September-October with the normalisation of supply chains and fresh crop arrivals. The softening was short-lived, however, and food inflation picked up again in November-December and remained elevated at 7.8 per cent in February 2024, primarily driven by increase in inflation of vegetables, pulses, as well as from an uptick in egg, meat and fish inflation in February. Food inflation excluding vegetables, however, moderated from 6.8 per cent in September 2023 to 4.9 per cent in February 2024, on the back of easing of inflation in cereals, milk, spices and prepared meals. Oils and fats sub-group has been in deflation since February 2023 (Chart II.8). Though vegetable prices dominated the overall food price build-up during 2023-24 so far, pulses, eggs, spices, cereals and sugar also registered substantial price increases, much higher than historical patterns. This was, however, offset by meat and fish, prepared meals, milk, non-alcoholic beverages and fruits which experienced lower price build-up this year than their pre-COVID long-term averages. Moreover, oils and fats registered significant price decline. As a result, price build-up in food excluding vegetables was lower than that in the pre-COVID period (Chart II.9).   The relatively shallower winter easing in vegetables prices during November 2023-February 2024 was primarily driven by lower market arrivals due to unseasonal rainfall in some parts of the country; above-normal temperatures owing to prevailing El-Niño conditions turning unfavourable for winter crop yields; lower production of some vegetables like garlic; and higher demand during the festival season. Moreover, deficient production in kharif pulses [(-) 6.6 per cent as per the second advance estimates (SAE) of 2023-24 over final estimates (FE) of 2022-23] on top of a decline in year-on-year (y-o-y) production in 2022-23 contributed to the hardening of inflation in pulses. The observed price pressures in the food and beverages group, however, was not broad-based as inflation remained below 4 per cent for items weighing almost 50 per cent in the food basket in February 2024. Inflation in cereals (weight of 9.7 per cent in the CPI and 21.1 per cent in the food and beverages group) moderated from 10.9 per cent in September 2023 to 7.6 per cent in February 2024 (Chart II.10). While rice prices, on a y-o-y basis, remained in double digits, prices of wheat (y-o-y) witnessed a sustained moderation since March 2023. Rice prices (y-o-y) were elevated as supply conditions remained tight despite restrictions on rice exports due to lower production [(-) 1.4 per cent based on the SAE of 2023-24 over FE of 2022-23]. Comfortable buffer stocks of rice (7.6 times the norm as of March 16, 2024) along with price stabilisation measures, including extension of 20 per cent duty on exports of parboiled rice; fixing the minimum export prices (MEP) of basmati rice at US$ 950 per tonne; increased offloading under the Open Market Sale Scheme (OMSS); and a targeted sale of newly launched ‘Bharat Rice’ at a fixed price (₹29 per kg) are likely to improve domestic availability and enable ebbing of price pressures in the medium term. In the case of wheat, price stabilisation measures including tightening of stock limits with respect to traders/wholesalers and retailers; the increased offloading of stocks under the OMSS; the sale of newly launched ‘Bharat Atta’ at a fixed retail price (₹27.5 per kg); and the ban/restriction on wheat exports since May 2022 helped contain inflation. The hike in the minimum support price (MSP) of wheat by 7.1 per cent in the rabi marketing season (RMS) of 2024-25 and an improved acreage by 1.2 per cent in the 2023-24 rabi season augurs well for higher wheat production and domestic supply. The SAE of 2023-24 indicates an increase in production of wheat by 1.3 per cent over the FE of 2022-23.  Vegetables (weight of 6.0 per cent in the CPI and 13.2 per cent in the food and beverages group) price inflation moderated in September-October 2023 but increased in November 2023-February 2024 due to less than usual winter easing in prices, above-normal temperatures, and cold waves in some parts of northern India (Chart II.11). Among key vegetables, onion prices increased sharply in November 2023 with a y-o-y inflation of 86.3 per cent driven by lower kharif acreage and fall in production [(-)15.7 per cent in 2023-24 as per the first advance estimates (FAE) over FE of 2022-23] due to erratic rainfall, on top of a production shortfall in the previous year. Onion prices fell in December 2023-February 2024 as price stabilisation measures such as imposition of 40 per cent export duty, followed by prohibition of exports, increased procurement, and offloading of onions at a fixed retail price (₹25 per kg) from select outlets helped improve domestic availability and contain price pressures. Tomato prices recorded y-o-y deflation in September-October 2023 after the surge in July-August due to floods and supply bottlenecks in some parts of the country. Inflationary pressures, however, recurred in November due to unseasonal rainfall which damaged crops. Potato prices, however, remained in deflation since February 2023 till January 2024 on account of higher production last year (an increase of 7.1 per cent in 2022-23 over FE of 2021-22). Production in 2023-24 experienced some shortfall [(-)1.9 per cent in 2023-24 as per the FAE over FE of 2022-23]. Potato prices increased in February, on a y-o-y basis, primarily due to an adverse base effect. Vegetables excluding TOP (tomato; onion; and potato) category like garlic, cauliflower and cabbage also witnessed lower than usual price correction during November 2023-February 2024, thereby emerging as major drivers of vegetables inflation (Chart II.11). More specifically, the lower production of garlic [(-) 0.8 per cent in 2023-24 as per the FAE over 2022-23 on top of (-) 8.1 per cent in 2022-23 over 2021-22] resulted in sustained price pressures leading to triple digit inflation since September 2023 – reaching 264.3 per cent in February 2024. As a result, vegetable price build-ups across TOP and non-TOP categories turned out to be much larger than usual in the financial year so far (Chart II.12).   Inflation in fruits (weight of 2.9 per cent in the CPI and 6.3 per cent within the food and beverages group), recorded a sustained increase since June 2023, peaking at 11.1 per cent in December 2023 before moderating to 4.8 per cent in February 2024. Elevated inflation in fruits, despite higher production (1.7 per cent in 2023-24 as per the FAE over FE of 2022-23), was driven primarily by apple due to lower than usual correction in its prices in November 2023-February 2024. Inflation in groundnut prices also remained in double digits during July-December 2023 on account of lower production. The primary source of plant-based protein i.e., pulses (weight of 2.4 per cent in the CPI and 5.2 per cent in the food and beverages group) recorded a sharp increase in prices. Double digit inflation since June 2023 was primarily driven by lower production of tur [(-) 21.5 per cent in 2022-23 over 2021-22 and an increase of only 0.8 per cent in 2023-24 as per the SAE over 2022-23], urad [(-) 5.2 per cent in 2022-23 over 2021-22 and (-) 14.4 per cent in 2023-24 as per the SAE of 2023-24 over 2022-23] and moong [(-) 17.6 per cent in 2023-24 as per the SAE of 2023-24 over 2022-23] (Chart II.13). The knock-on effect of lower production is also reflected in lower stock-to-use ratio (Chart II.14). Price pressures in pulses eased marginally and inflation moderated to 18.9 per cent in February 2024 following supply-side measures including extension of ‘free’ import policy for urad and tur till March 31, 2025; removal of minimum import price restrictions on yellow peas till March 2024 and sale of subsidised chana dal under the brand 'Bharat Dal'.   Prices of animal-based protein items increased marginally during October 2023-February 2024 as increase in prices of milk and products (weight of 6.6 per cent in the CPI and 14.4 per cent within the food and beverages group) and eggs (weight of 4.0 per cent within the group) were partially offset by moderation in meat and fish (weight of 3.6 per cent in CPI and 7.9 per cent within the food and beverages group) prices (Chart II.15). Inflation in prices of milk and products has consistently moderated since its 9-year peak of 9.6 per cent in February 2023 on the back of higher milk production as well as easing feed and fodder costs. Prices of eggs, however, have exhibited high momentum since September 2023 reflecting seasonal demand and higher exports. On the other hand, prices of meat and fish eased more than usual in the second half of 2023-24 due to higher production against lower than anticipated demand. In February 2024, however, inflation in meat and fish picked up sharply due to lower supply of broiler on account of bird flu in Andhra Pradesh as well as adverse base effects. Prices of oils and fats (weight of 3.6 per cent in the CPI and 7.8 per cent within the food and beverages group) remained in deflation throughout 2023-24 (April-February) due to lower international prices and higher domestic production of oilseeds during the 2022-23 season (8.9 per cent in 2022-23 over FE of 2021-22) (Chart II.16). Extension of lower import duty on crude palm, sunflower and soyabean oil till March 2025 is likely to keep inflation low despite an estimated shortfall in oilseeds production [(-) 9.2 per cent in 2023-24 as per the SAE of 2023-24 over FE of 2022-23]. Ghee and butter price inflation moderated, reflecting pass-through of easing milk price inflation and favourable base effect.  Inflation in prices of sugar and confectionery (weight of 1.4 per cent in the CPI and 3.0 per cent in the food and beverages group) hardened during October-February 2023-24 on lower kharif production [(-) 9.0 per cent as per the SAE of 2023-24 over FE of 2022-23], following higher year-on-year production in 2022-23, and an increase in the fair and remunerative price (FRP) of sugarcane by ₹10 per quintal for 2023-24. Nevertheless, supply measures to ensure domestic availability, including extension of export restrictions, ban on the use of sugarcane juice and syrup for ethanol production and imposition of 50 per cent export duty on molasses used for ethanol production w.e.f. January 2024 are likely to contain inflationary pressures.  Among other food items, inflation in spices remained in double digits, primarily driven by jeera on account of adverse weather conditions and stagnant production. Spices inflation has, however, gradually moderated since October 2023 as month-on-month (m-o-m) price pressures in jeera eased and turned negative in December 2023 due to higher acreage and production (49 per cent as per FAE of 2023-24 over FE of 2022-23). Prices of prepared meals have moderated gradually, reflecting the pass-through of lower input costs of edible oils and liquified petroleum gas (LPG). Retail Margins Retail price margins – the difference of retail and wholesale prices12 – for cereals increased during September 2023-March 2024. After recording a sustained increase from September 2023 to January 2024, pulses price margins stabilised from February onwards. Retail price margins in edible oils softened in the recent period, primarily due to a moderation in the margin in refined oils. Retail price margins of TOP vegetables had moderated from its peak recorded in July 2023 due to softening of tomato prices during mid-August 2023. The margins, however, hardened again in November 2023 with a pick-up in wholesale prices of onions. Aided by supply-side measures to control the rise in onion prices, the retail price margins of TOP vegetables have started to soften from December 2023 onwards (Chart II.17).   Sectoral and Spatial Distribution of Food Inflation CPI food inflation pressures were seen across both rural and urban areas, with urban food inflation outpacing its rural counterpart (Chart II.18). At the same time, volatility in food inflation13 in urban areas was higher than in rural areas. This was mainly driven by protein, fruits, and vegetables. Spatially, food inflation pressures are softening – the number of states/UT with food inflation higher than 6.0 per cent in the period 2023-24 (April-February) has decreased to 20 vis-à-vis 27 in the corresponding period a year ago (Table II.1).

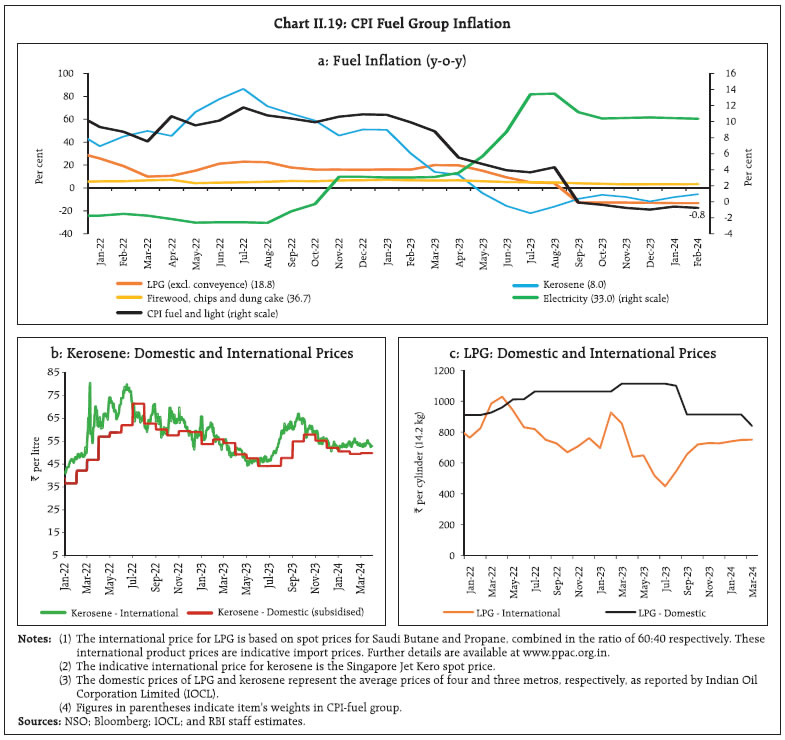

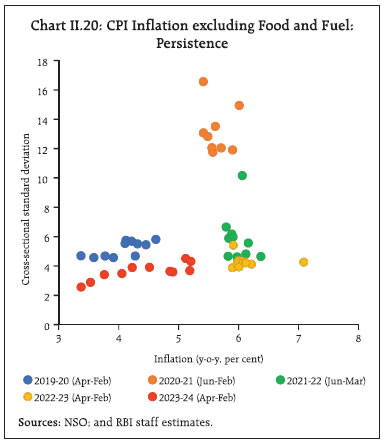

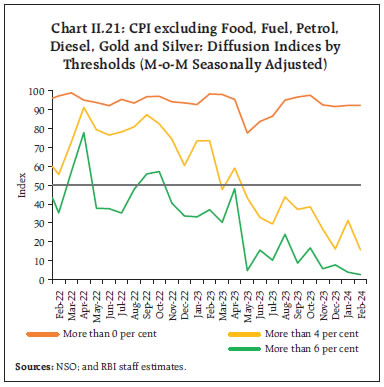

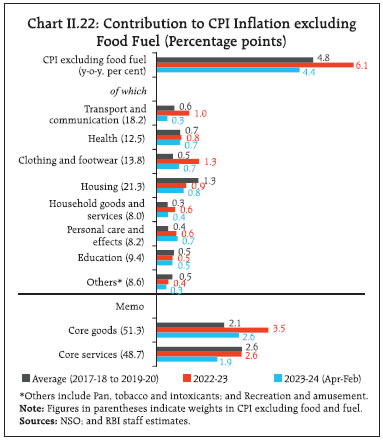

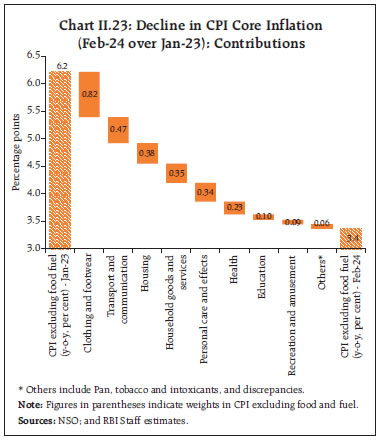

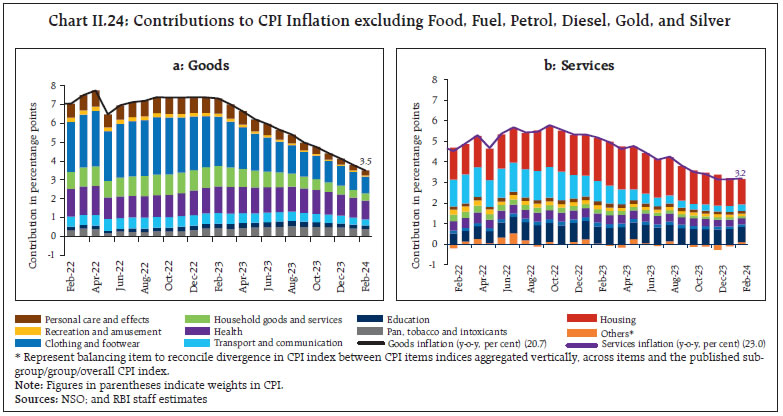

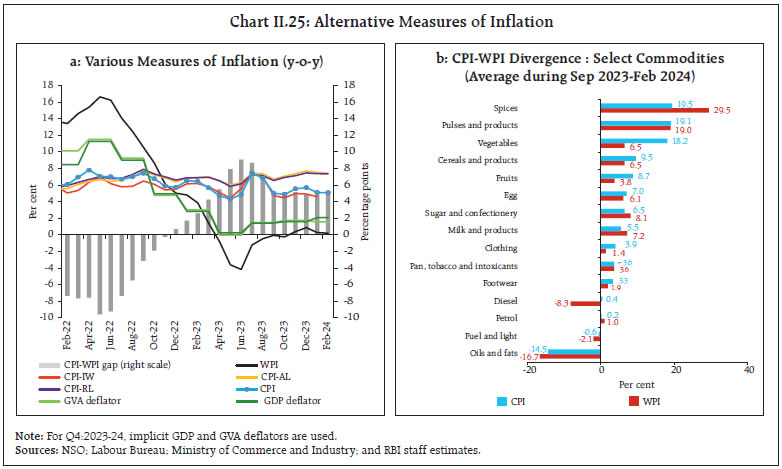

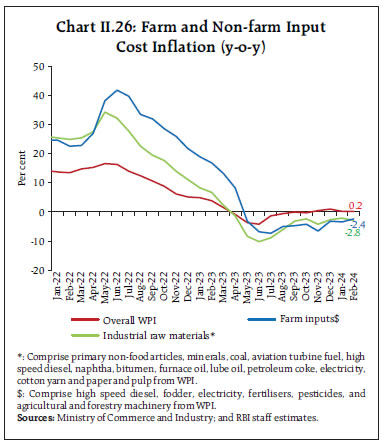

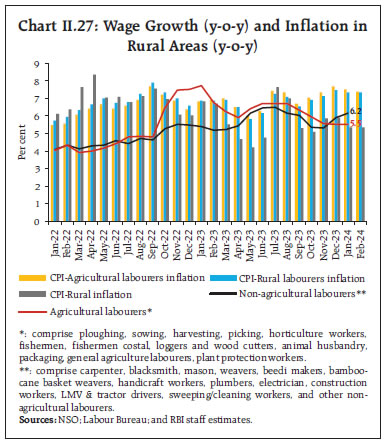

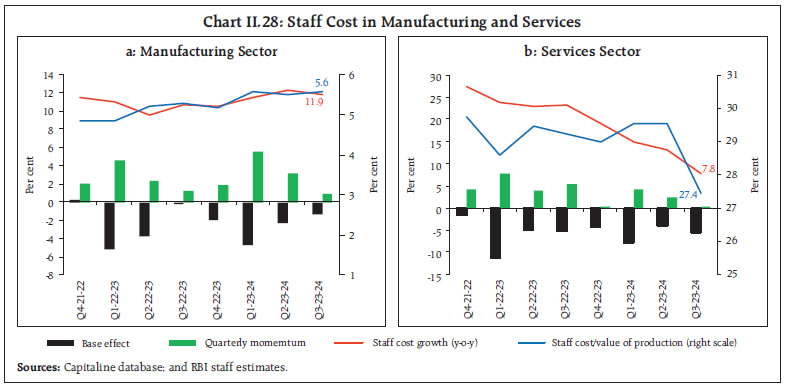

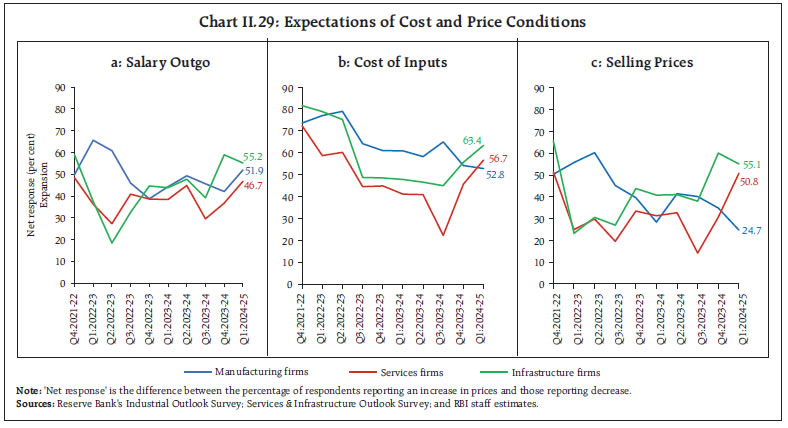

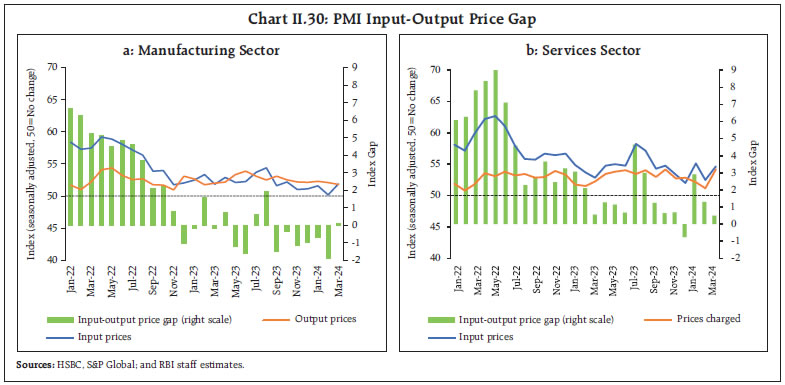

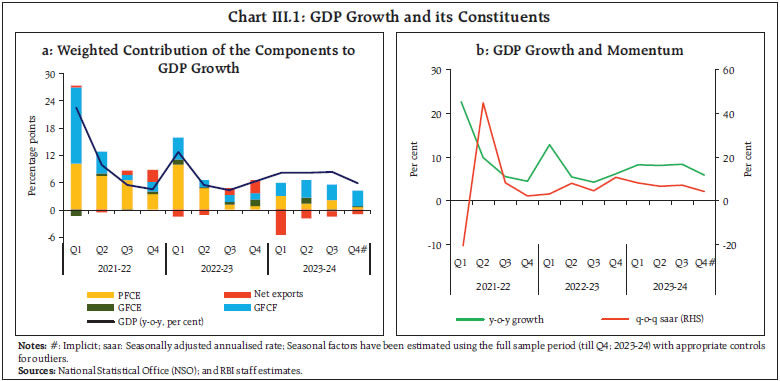

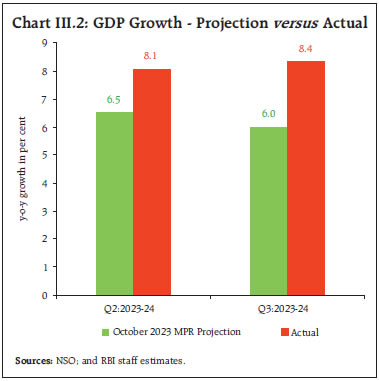

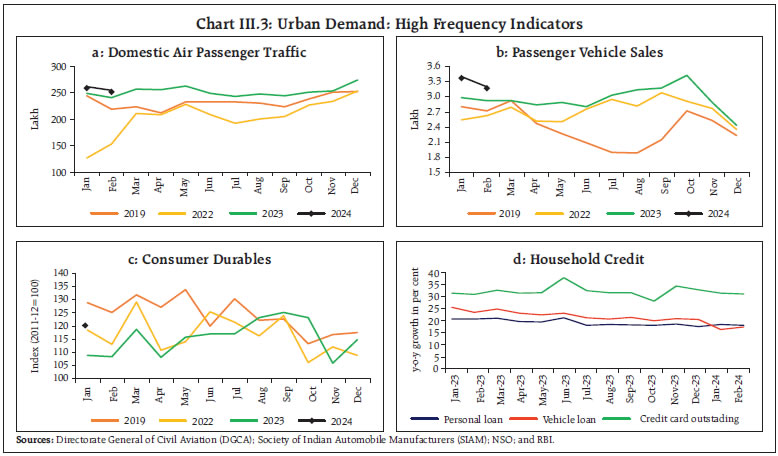

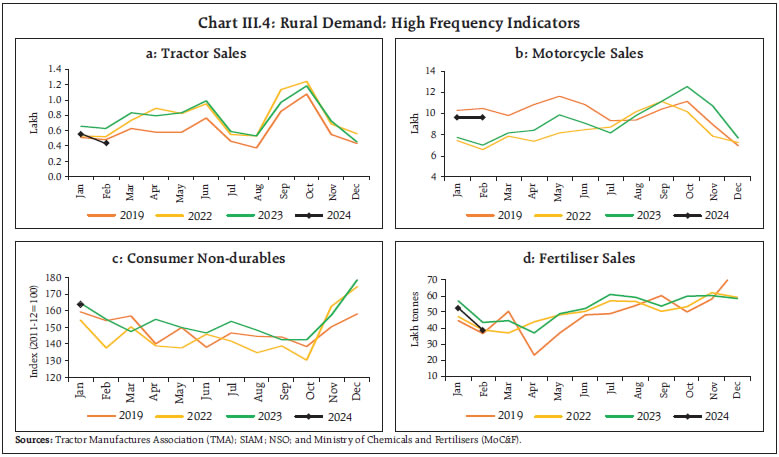

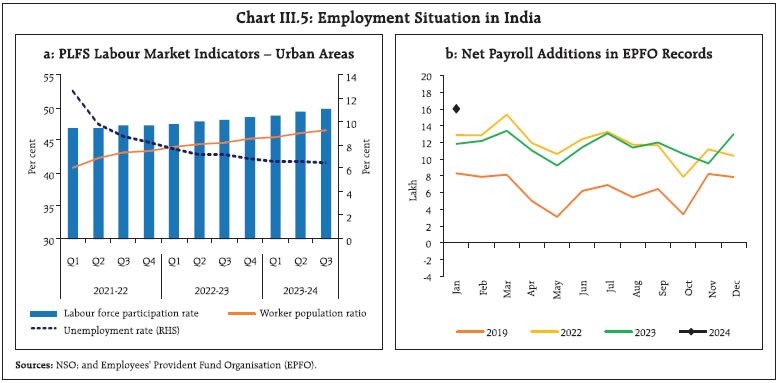

CPI Fuel Group CPI fuel slipped into deflation of (-) 0.1 per cent in September 2023 from 4.3 per cent in August, and remained in the deflationary zone till February 2024. Its primary driver has been the substantial reduction in domestic liquified petroleum gas (LPG) prices by ₹200 per cylinder at the end of August, alongside a y-o-y decline in kerosene prices aided by softening international prices, and a slowdown in price increases (y-o-y) in firewood and chips. Electricity price increases, on a y-o-y basis, moderated from a record 13.5 per cent in August 2023 to 10.4 per cent in February 2024 (Chart II.19). Core CPI (CPI excluding Food and Fuel) Disinflation in core (CPI excluding food and fuel) continued during H2 of 2023-24, softening from 4.9 per cent in August 2023 to 3.4 per cent in February 2024 – the lowest rate of core inflation in the current CPI series (2012=100)15. Other exclusion-based measures of underlying inflation, which remove volatile items such as petrol, diesel, gold, and silver in addition to food and fuel, also witnessed sharp and sequential moderation during this period (Table II.2) along with lower cross-sectional variation in inflation rates (Chart II.20). The sharp broad-based softening of core price momentum in H2 is observed in the collapse in CPI threshold diffusion indices (DIs). CPI excluding food, fuel, petrol, diesel, gold and silver DIs for price increases of greater than 6 per cent (saar) and 4 per cent (saar) slipped deeper into the contraction zone during September-December 2023, indicating sequentially lower incidence of price increases beyond the 6 per cent and 4 per cent saar thresholds.  The rebound of the 4 per cent threshold DI in January 2024 was transient as it corrected in February to slide further into the contraction zone along with collapse of the 6 per cent threshold DI to low single digits (Chart II.21). Both core goods and services categories experienced significant easing in 2023-24 so far (April-February). Barring personal care and effects, which was impacted by pick-up in gold prices, the contribution of all other sub-groups/groups to core inflation fell (Chart II.22). Out of the 2.8 percentage points moderation in core from its recent peak in January 2023, 82 bps was contributed by clothing and footwear sub-group. In addition, transport and communication accounted for 47 bps; housing contributed 38 bps; household goods and services, and personal care and effects contributed around 35 bps each (Chart II.23).   Decomposing CPI excluding food, fuel, petrol, diesel, gold, and silver inflation into its goods (with a weight of 20.7 per cent in the headline CPI) and services (weight of 23.0 per cent) components shows softening in both the categories, mainly led by goods. While core goods inflation moderated by around 190 bps from 5.4 per cent in August 2023 to 3.5 per cent in February 2024, core services inflation fell by around 105 bps from 4.2 per cent to 3.2 per cent during the same period. The key drivers of the softening in goods inflation were clothing and footwear, household goods, health and personal care and effects (excluding gold and silver) (Chart II.24a). In the case of services, housing (primarily house rent), transportation fares (bus/tram/taxi fare, air fare) and communication services drove the moderation in inflation (Chart II.24b).   Trimmed mean measures16 also indicated an easing of underlying inflation pressures, with weighted median inflation registering a decline of around 160 bps from 5.2 per cent in August 2023 to 3.6 per cent in February 2024 (Table II.3). Other Measures of Inflation CPI inflation for agricultural labourers (CPI-AL) and rural labourers (CPI-RL) exceeded CPI headline inflation during September 2023-February 2024 due to higher food and fuel inflation. Inflation in terms of CPI for industrial workers (CPI-IW), on the other hand, was below the headline CPI during September 2023 - January 2024, primarily on account of fuel inflation being significantly lower in CPI-IW vis-à-vis headline CPI. After staying in deflationary territory between April and October 2023, wholesale price index (WPI) inflation turned positive in November 2023 on the back of a pick-up in food prices along with unfavourable base effects. On account of an uptick in CPI inflation and WPI inflation turning positive, inflation measured by deflators for gross value added (GVA) and gross domestic product (GDP) further hardened in Q3:2023-24 (Chart II.25a).  On the whole, WPI inflation remained far below headline CPI inflation during September 2023-February 2024, driven down by deflation in non-food manufactured products in WPI. In terms of similar categories, WPI inflation in food (particularly cereals, vegetables, fruits and egg), and clothing and footwear ruled below corresponding CPI groups/subgroups. Deflation in edible oil and fuel prices was deeper in the WPI. On the other hand, inflation in spices, sugar, milk, and petrol was higher in the WPI than in the CPI (Chart II.25b).  Costs, as measured by WPI inflation in industrial raw materials and farm inputs, had entered negative territory in April-May 2023 and remained muted during September 2023-February 2024 on account of sustained easing of international commodity prices (Chart II.26). Prices of industrial inputs such as high-speed diesel (HSD), aviation turbine fuel (ATF), bitumen and petroleum coke were also in deflation during November 2023-February 2024. The other contributory factors were non-food articles, particularly cotton and oilseeds, the prices of which continued to decline due to easing in international prices and lower demand. Minerals price inflation, however, remained positive during this period, driven by metallic minerals, particularly iron ore due to increased global demand, and copper due to both rising demand and limited supply owing to constraints on new mining projects worldwide, increased taxes and environmental regulations. Farm input prices deflated during September 2023-February 2024 due to decline in prices of HSD, fodder, pesticides, and fertilisers. The price of WPI electricity – a key input in both industrial and farm inputs – remained in deflation for most part of H2:2023-24 due to low rise in prices of coal coupled with favourable base effects.  Nominal rural wages increased by 5.9 per cent in January 2024, driven by wage growth in the non-agricultural rural sector (Chart II.27). While an increase in agricultural wages was recorded primarily in irrigation, harvesting and animal husbandry, the increase in non-agricultural wages was broad-based across major activities in the rural sector. In the organised sector, staff cost growth (y-o-y) remained steady for manufacturing firms among listed companies in Q3:2023-24, while it decelerated for services firms. The share of staff cost in the value of production for manufacturing was broadly stable, whereas it fell steeply in Q3 for the services sector (Chart II.28).   As per the firms polled in the Reserve Bank’s enterprise surveys17, the pace of salary outgo, cost of inputs and selling prices is expected to rise steeply for services sector in Q1:2024-25. On the other hand, pace of growth in selling prices is likely to soften for manufacturing and infrastructure sectors even though inputs costs for infrastructure sector and salary outgo for manufacturing sector would rise at a faster rate in Q1 (Chart II.29).   After witnessing a dip in January 2024, one year ahead business inflation expectations18 increased by 9 basis points to 4.46 per cent in February on account of mild increase in cost pressures and sales expectations. As per the purchasing managers’ index (PMI), barring a transient dip in February, the input prices momentum of manufacturing firms rose during December 2023-March 2024 due to increase in prices of cotton, iron, machinery tools, plastics, chemical, paper and textiles. The growth in output prices, however, remained stable with a marginal decline in February-March leading to input-output price gap turning positive in March. For services sector, the pace of increase in input prices remained volatile with a sharp pick-up in March 2024 due to food, labour costs, cosmetics and medical equipment. The prices charged by service firms rose more than input prices in March 2024 which led to a further narrowing of the input-output price gap (Chart II.30). Inflation has seen substantial moderation from elevated levels in the summer of 2022 but is still above the target. With core disinflation being broad based across goods and services, risks to the 'last mile' of disinflation process may emanate from incidence of unpredictable supply side shocks, which include adverse climate events and their impact on agricultural production; and geo-political tensions and its spillovers to trade and commodity markets. The combination of monetary policy action and stance, and proactive supply side measures have helped steer the disinflation process in the face of considerable uncertainties. This approach would need to be sustained to ensure a durable return of inflation to the target, thereby setting strong foundations for the high growth trajectory that is underway. _________________________________________________________________________________ 1 Headline inflation is measured by year-on-year (y-o-y) changes in the all-India consumer price index (CPI) produced by the National Statistical Office (NSO). 2 Core CPI, i.e., CPI excluding food and fuel is worked out by eliminating the groups ‘food and beverages’ and ‘fuel and light’ from the headline CPI. 3 A change in CPI year-on-year (y-o-y) inflation between any two months is the difference between the current month-on-month (m-o-m) change in the price index (momentum) and the m-o-m change in the price index 12 months earlier (base effect). For more details, see Box I.1 of the MPR, September 2014. 4 The CPI diffusion index, a measure of dispersion of price changes, categorises items in the CPI basket according to whether their prices have risen, remained stagnant or fallen over the previous month. The higher the reading above 50, the broader is the expansion or generalisation of price increases; the further is the reading below 50, the broader is the price decline across items. 5 Threshold diffusion indices capture the dispersion of price increases in CPI basket beyond the specified saar thresholds of 4 per cent and 6 per cent. 6 Historical decomposition estimates the contribution of each shock to the movements in inflation over the sample period (Q4:2010-11 to Q4:2023-24) based on a vector autoregression (VAR) with the following variables (represented as the vector Yt) – crude oil prices (US$ per barrel); exchange rate (INR per US$), asset price (BSE Sensex), CPI; the output gap; rural wages; the policy repo rate; and money supply (M3). All variables other than policy repo rate are y-o-y growth rates. The VAR can be written in reduced form as: Yt =c + A Yt-1 + et; where et represents a vector of shocks. Using Wold decomposition, Yt can be represented as a function of its deterministic trend and sum of all the shocks et. This formulation facilitates decomposition of the deviation of inflation from its deterministic trend into the sum of contributions from various shocks. 7 The CPI weighting diagrams use the modified mixed reference period (MMRP) data based on the 2011-12 Consumer Expenditure Survey conducted by the National Sample Survey Office (NSSO). Under MMRP, data are collected on expenditures incurred for frequently purchased items – edible oil, eggs, fish, meat, vegetables, fruits, spices, beverages, processed foods, pan, tobacco and intoxicants – during the last seven days; for clothing, bedding, footwear, education, medical (institutional), durable goods, during the last 365 days; and for all other food, fuel and light, miscellaneous goods and services including non-institutional medical services, rents and taxes, data relate to the last 30 days.  9 Item specific price shocks greater than one standard deviation were considered for computing frequency and duration as price changes less than one standard deviation could largely reflect idiosyncratic factors specific to individual items. 10 The low duration for CPI housing could be on account of staggered house rent data collection over six months among the sampled units under the Repeat House Rent Survey procedure used for compiling the house rent index. 11 Global commodities that drive domestic prices include petroleum products, coal, electronic goods, gold, silver, chemical products, metal products, textiles, cereals, milk products, and vegetables oils – these together have a weight of 36.4 per cent in the CPI basket. 12 Item level retail and wholesale prices are aggregated at respective subgroups using item level CPI weights. Data for January-March 2021 have been excluded due to changes in price collection mechanism and item varieties by DCA. 13 Estimated using GARCH process. 14 Accounted for the unification of Daman and Diu with Dadra & Nagar Haveli and the formation of Ladakh as a UT 15 A core inflation print of 3.4 per cent was also seen in October 2019. 16 While exclusion-based measures drop a fixed set of volatile items (for example, food and fuel) in each period; trimmed measures exclude items located in the tails of the inflation distribution - items displaying changes more than the specified threshold in prices each month are excluded from each side, and the items dropped differ from month to month. 17 Industrial Outlook Survey; and Services and Infrastructure Outlook Survey. 18 Based on the monthly Business Inflation Expectations Survey (BIES) of the Indian Institute of Management, Ahmedabad. The survey polls a panel of business leaders primarily from the manufacturing sector about their inflation expectations in the short and medium term. Domestic economic activity remained resilient in H2:2023-24 with investment demand firming up at a robust pace. Manufacturing activity strengthened further, and construction activity stayed firm. Consumer and business optimism remains buoyant. Headwinds from geopolitical tensions, rising geoeconomic fragmentation, volatility in global commodity prices, and escalation of Red Sea disruptions, however, pose risks to the outlook. After a strong performance in H1:2023-24, the momentum of domestic economic activity remained resilient in H2, driven by strong aggregate demand. Fixed investment firmed up at a robust pace with the government’s continued thrust on infrastructure building. Private corporate investment is gaining vitality. Private consumption held up well in urban areas, although its overall growth moderated. India’s exports recouped some ground which, in conjunction with deceleration in imports growth, led to a lower drag from net external demand on aggregate demand in H2. Overall, real gross domestic product (GDP) expanded strongly by 7.6 per cent year-on-year (y-o-y) in 2023-24, with 8.4 per cent growth in Q3 – the third successive quarter of over eight per cent growth. On the supply side, manufacturing activity continued to gain traction in H2, supported by lower commodity prices, diversifying global supply chains and easing logistic costs due to improving infrastructure. Buoyancy in construction activity contributed to services sector momentum. Real gross value added (GVA) posted a growth of 6.9 per cent y-o-y in 2023-24. Headwinds from geopolitical tensions, rising geoeconomic fragmentations, volatility in global commodity prices, and escalation of Red Sea disruptions, however, pose risks to the outlook. Aggregate demand conditions exhibited buoyancy in Q3:2023-24 (Chart III.1 and Table III.1). Its momentum – quarter-on-quarter (q-o-q) seasonally adjusted annualised rate (saar) – remained strong in Q3.  GDP Projections versus Actual Outcomes The October 2023 Monetary Policy Report projected real GDP growth at 6.5 per cent for Q2:2023-24, 6.0 per cent for Q3 and 5.7 per cent for Q4. The actual growth for Q2 turned out to be higher at 8.1 per cent led by sharper than expected expansion in gross fixed capital formation (GFCF) (Chart III.2). In Q3 also, the actual growth at 8.4 per cent overshot the projection due to more than expected increase in GFCF and moderation in drag from net exports. Data for Q4:2023-24 are scheduled to be released by the National Statistical Office (NSO) on May 31, 2024.  III.1.1 Private Final Consumption Expenditure Growth in private final consumption expenditure (PFCE) – the mainstay of aggregate demand – improved to 3.5 per cent in Q3 after a dip in Q2 and contributed 2.2 percentage points to overall GDP growth. Steady urban consumption, coupled with improving income levels in the informal sector, are supporting private consumption. For the full year 2023-24, PFCE growth moderated to 3.0 per cent from 6.8 per cent in 2022-23, partly reflecting sensitivity to financial conditions (Box III.1). High frequency indicators of urban demand exhibited sustained expansion in H2:2023-24 (Chart III.3). Domestic air passenger traffic, passenger vehicle sales and household credit posted robust growth. Consumer durables expanded at a modest pace in Q3, but recorded double digit growth in January. Sustained buoyancy in the services sector along with corporate salary hikes are supporting urban demand. Rural demand is gaining pace gradually as exhibited by high frequency indicators, although it lags urban demand. Motorcycle sales expanded at a rapid pace in H2:2023-24, while sales of tractors and fertilisers remained subdued after high growth last year. Consumer non-durables registered moderate growth in Q3 and contracted marginally in January (Chart III.4). The demand for work under the Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) declined in H2, suggesting improvement in non-farm employment in rural areas and recovery in informal sector activity. Agricultural credit growth remained robust, notwithstanding lower estimates of rabi production.   The labour force participation rate (LFPR) and employment rate (ER) reflect improvement in labour market conditions. As per the Periodic Labour Force Survey (PLFS), LFPR at all India level for persons aged 15 years and above (usual status) improved to 59.8 per cent (56.1 per cent last year) and the unemployment rate dropped to 3.1 per cent (3.6 per cent last year) during 2023 (January-December). The latest quarterly PLFS indicate that LFPR for person aged 15 years and above (current weekly status) increased to 49.9 per cent in Q3:2023-24 in urban areas, the highest since the survey’s inception. The unemployment rate in urban areas during Q3 dropped to 6.5 per cent, the lowest in the PLFS series (Chart III.5a). The Employees’ Provident Fund Organisation (EPFO) payrolls data also point to strengthening of formal employment in Q3 as net payroll additions rose by 12.5 per cent y-o-y in Q3 and by 35.4 per cent y-o-y in January 2024 (Chart III.5b).