IST,

IST,

Measuring Productivity at the Industry Level - The India KLEMS Database

|

This document describes the procedures, methodologies and approaches used in the construction of India KLEMS database version 2024. The dataset includes measures of Gross Value Added (GVA), Gross Value of Output (GVO), Labour Employment (L), Labour Quality (LQ), Capital Stock (K), Capital Composition (KQ), the consumptions of Energy (E), Material (M) and Services (S) inputs, Labour Productivity (LP) and Total Factor Productivity (TFP). The database covers 27 industries comprising of the entire Indian economy. The database also provides these estimates at the broad sectoral levels (agriculture, manufacturing and services) and at the all-India levels. In the current version of the database covers the period from 1980-81 to 2022-23. The series have been constructed on the basis of data compiled from NSO, NSSO, ASI, Input-Output tables (I-O tables) and processed according to appropriate procedures. These procedures were developed to ensure harmonization of the basic data, and to generate growth accounts in a consistent and uniform way. Harmonization of the basic data has focused on several areas such as industrial classification, and aggregation levels. The production and publication of India KLEMS database are meant to support empirical research in the area of economic growth and its sources. Most importantly, the database is meant to support the conduct of policies aimed at supporting the acceleration of productivity growth in the Indian economy. The India KLEMS database, in this regard, provides a comprehensive measurement tool to monitor and evaluate productivity growth in the Indian economy. Finally, the construction of the database would also support the systematic production of reliable statistics on growth and productivity using internationally comparable methodologies based on India’s national accounts, input-output tables and labour market surveys. The work relating to compilation of India KLEMS data was being done by the India KLEMS team housed at the Centre for Development Economics, Delhi School of Economics until the end of 2020. The work has been shifted to the KLEMS Division of the Department of Economics and Policy Research of RBI since February 2021The current version of the India KLEMS Database, released hereby, is the third independent compilation of this data by the KLEMS Division in RBI, after the previous release of the data in January 2024. 1.2 Coverage: Industries and Variables In this section we describe the coverage of India KLEMS database in terms of industries and variables. The database is created for 27 industries. The industrial classification is constructed by building concordance between NIC 2008, NIC 2004, NIC 1998, NIC 1987 and NIC 1970 to generate a uniform definition of ‘industries’ since 1980-81. This classification is very close to the International Standard Industrial Classification (ISIC) revision 3. The 27 industries are aggregated to form six broad sectors, namely:

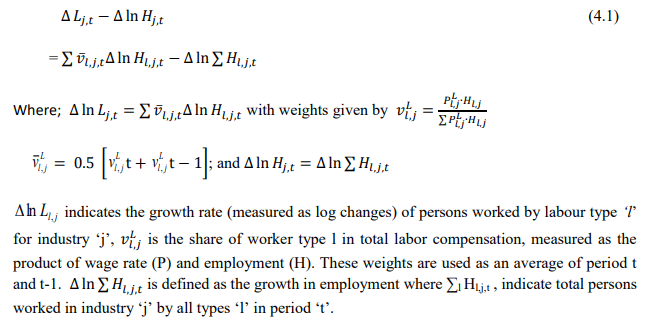

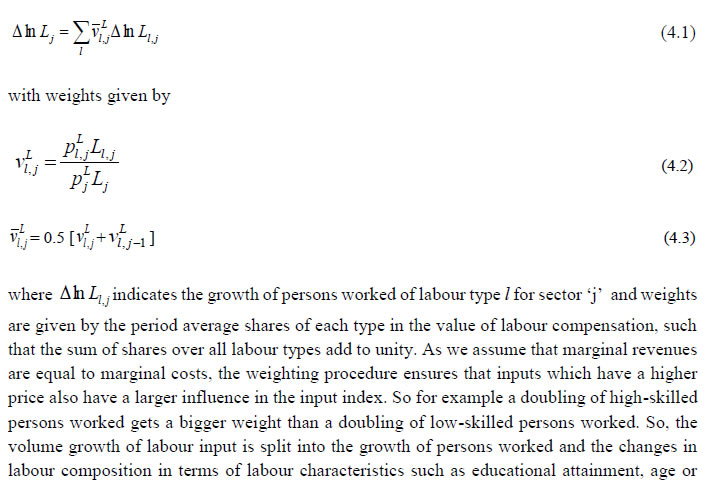

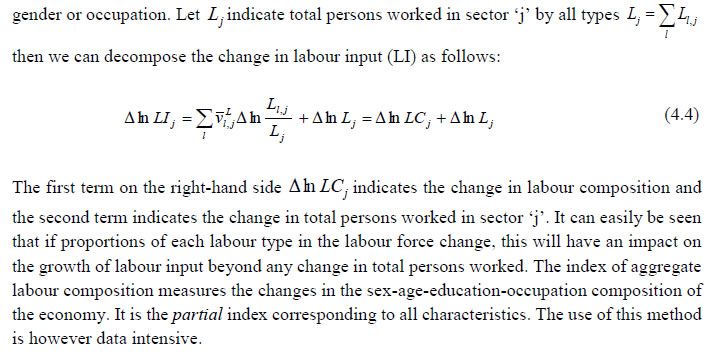

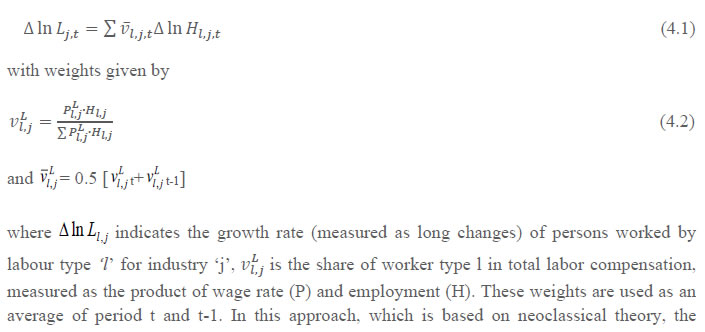

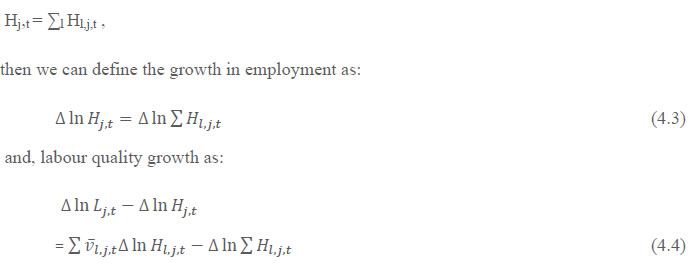

Table 1.1 provides a list of the 27 industries, including the higher aggregates. For detailed classification and concordance of study industries with NICs, readers may refer to Version 8 of the manual published in 2022. Table 1.2 provides an overview of all the series included in our database. Measures of Capital (K), Labour (L), Energy (E), Material (M) and Service (S) inputs as well as Gross Output (GO), have been constructed using National Accounts Statistics (NAS), Annual Survey of Industries (ASI), NSSO rounds and Input-Output (IO) Tables. In building annual time series on gross output, five inputs and factor income shares, various assumptions are made to fill up gaps in industry details and link series over time. As we know that NSSO rounds of unregistered manufacturing, Input Output Transaction Tables, and Employment and Unemployment Surveys by NSSO are available only for certain benchmark years, the use of information from these data sources necessitates interpolation and assumption of constant shares for building a series of output and inputs. However, as the successor of NSSO's Employment Unemployment Survey, the Periodic Labour Force Survey (PLFS) data has become available annually since 2017-18, the labour input series no longer requires any extrapolation. The labour input series is being updated under each round of India KLEMS using available survey data from PLFS only. Chapter 2: Gross Value-Added Series at the Industry Level This chapter describes the data sources and methodology used to construct the Gross Value Added (GVA) series at current and constant prices for 27 study industries for the period of 1980-81 (1980) to 2022-23(2023). The National Accounts Statistics (NAS) brought out by the NSO (National Statistics Office, Government of India) is the basic source of data for the construction of series on gross value added for INDIA KLEMS-industries. Up to 2011-12, estimates of GVA at both current and constant (2011-12) prices for all industries are obtained from Back Series of National Accounts (Base 2011-12). For years after 2011-12, they are directly obtained from NAS 2023. However, NAS estimates of value added are not available for a few India KLEMS industry groups. Therefore, we had to split some of the aggregate industry groups from NAS. Maintaining consistency with NAS, the value-added data in India KLEMS is measured at basic price. The construction of Gross valued added series involves three steps. Step 1: A concordance table between the classification used in the NAS and the 27 study industry classification used for this project has been prepared. Further, concordance between all the 27 sectors has been constructed with NIC- 1970, 1987, 1998, 2004 and 2008. Out of the 27 study industries, for 20 industries, GVA series both in current and constant prices is directly taken from NAS1. The sectors for which data are provided in NAS are Agriculture, Forestry & logging, Fishing, Mining and Quarrying, Manufacturing, Electricity, gas and water supply, Construction, Trade, Hotels & Restaurants, Railways, Transport by other means, Storage, Communication, Banking & insurance, Real estate, Ownership of Dwelling & Business Services, Public Administration & Defense and Other Services. Step 2: For manufacturing industries where direct estimates of GVA were not available from NAS, estimates have been made using additional information from ASI and NSSO unorganised manufacturing data. In these cases, GVA data is constructed by splitting the NAS data using ASI or NSSO distributions. ASI data (annual) has been used for registered and corporate manufacturing, whereas interpolated ratios from NSSO 40th (1984-85), 45th (1989-90), 51st (1994-95), 56th (2000-01), 62nd (2005-06), 67th round (2010-11) and 73rd round (2015-16) rounds have been used for Unregistered and household manufacturing segments. For unregistered manufacturing for years 2015-16 to 2022-23 the ratio obtained from 73rd round of unregistered manufacturing has been used for the splitting. Table 2.1 and Table 2.2 showcase the methodology used to split GVA of certain NAS sectors to match concordance with our classification. It is important to note that the industry-level value-added volume indices are based on NAS. NSO provides single-deflated value-added estimates for all sectors except Agriculture. Step 3: According to India KLEMS, GVA is adjusted for Financial Intermediation Services Indirectly Measured (FISIM). The detailed method of FISM adjustment is provided in earlier versions of the KLEMS manual. Chapter 3: Gross Output Series at the Industry Level This chapter describes the procedures and methodologies used in constructing the database for gross output series at the industry level over the period 1980-81(1980) to 2022-2023(2023). To construct the gross output series at industry level, we use multiple data sources namely National Accounts Statistics, Annual Survey of Industries, NSSO rounds for unorganized manufacturing and Input Output Transaction tables. The data sources and methodology used are documented below: National Accounts Statistics: The NAS is the basic source of data for the construction of time series on the gross output. For years since 2011, we have taken the estimates of GVO both at current and constant prices for all industries directly from NAS 2024. (a) Filling procedures of National Accounts series: It is to be noted that the NAS estimates of gross output for a few industry groups are at a more aggregate level, requiring splitting of the aggregates. In such cases, NAS estimates of output have been split using additional information from the Annual Survey of Industries and NSSO rounds of Unregistered Manufacturing to obtain estimates at a higher level of disaggregation. Secondly, for Unregistered manufacturing, gross output data is available in NAS from 2004-05 onwards. In this case, information from NSSO survey rounds has been used for missing years to derive output estimates of unregistered manufacturing industries at current and constant prices. As mentioned earlier, for the gross value-added series of service sectors, we obtain our estimates from NAS. However, prior to 2011-12, National Accounts did not provide any estimates of the gross output of service sectors and hence we rely on Input output transaction tables (from which the ratio of gross to value added is computed which is then applied to GVA reported in NAS) which are available at an interval of 5 years or so. This necessitates interpolation and assumption of constant shares for measuring output of services sectors. The Input Output Transaction Tables for Benchmark years of 1978-79, 1983-84, 1989-90, 1993-94, 1998-99, 2003-04 and 2007-08 are used to derive gross output series for service sectors. The construction of the gross output series at current and constant prices involves the following steps: Step 1: Measuring Gross Output of Agricultural Sector, Mining and Quarrying, and Construction NAS provides nominal and real GVO series for a) Crops and Plantation, b) Animal Husbandry c) Forestry and Logging d) Fishing. By aggregating the GVO of these four subsectors we derive the GVO of Agricultural sector. The Gross output estimates of Mining and Quarrying and Construction at current and constant prices from 1980-2023 is also directly taken from NAS. Step 2: Measuring Gross Output of Manufacturing Industries Since 2011-12, gross output data for 7 out of 13 manufacturing industries listed in table 3.1 are directly picked up from NAS. For the remaining 6 sectors output is constructed by splitting the NAS output data using ASI or NSSO distributions. ASI data (annual) has been used for registered manufacturing whereas interpolated ratios from 67th (2010-11) and 73rd (2015-16) rounds have been used for Unregistered Manufacturing segments. A list of study industries is presented in Table 3.2 showcasing the methodology used to split GVO of certain NAS sectors to match concordance with our classification for the year 2011 to 2023. Step 3: Measuring Gross Output for Services Sectors and Electricity, Gas and water supply Since 2011 -12 NAS provided estimates of GVO at current and constant prices. Prior to 2011-12 Gross Output series for Services sectors and sector Electricity, Gas and Water supply have been constructed using information from Input – Output Transaction Tables of the Indian economy published by CSO. The details method of construction of GVO back series for services is provided in earlier versions of KLEMS Data manual. Chapter 4: Labour Input Series at the Industry Level This chapter discusses the construction of labour input for 27 industries from 1980-81 to 2022-23. Labour input captures both the quantity of labour (i.e. number of persons) and quality of labour over time. Labour quality is measured based on educational qualification and wage rates of the workers within each of the 27 industries. Given the limitations of India’s employment statistics (Sivasubramonian; 2004, & Himanshu; 2011, Ghose; 2016), especially the availability of information on wages/ earnings of different category of workers across industries, the database provides only the labour quality index based on five different education categories. Labour input is measured by multiplying the number of persons employed by the index of labour quality which captures the human capital embodied in the labour, constructed separately for each industry. The 38th to 68th rounds of the Employment and Unemployment Survey (EUS) by India’s National Sample Survey Office (NSSO) conducted between 1983 and 2011-12, respectively, and all the annual Periodic Labour Force Survey (PLFS) rounds from 2017-18 to 2022-23 by National Statistical Organization (NSO) are the main sources data for estimating labour input. We use India’s decadal census and population projections based on Government of India’s various reports for estimating India’s population. Methodology The total employment, measured by the number of persons engaged in each of the 27 industries in India is computed as follows:

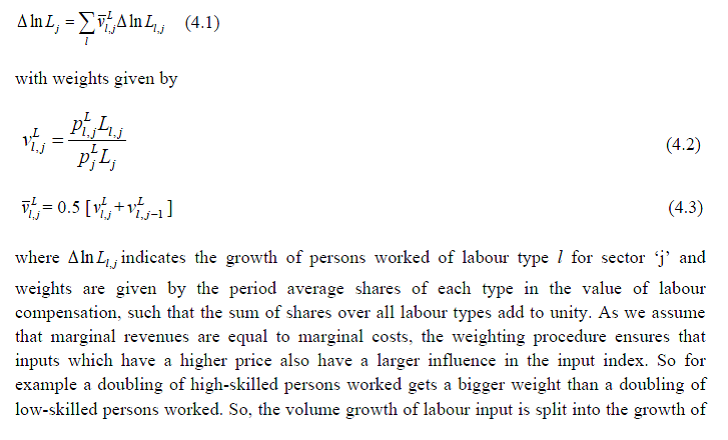

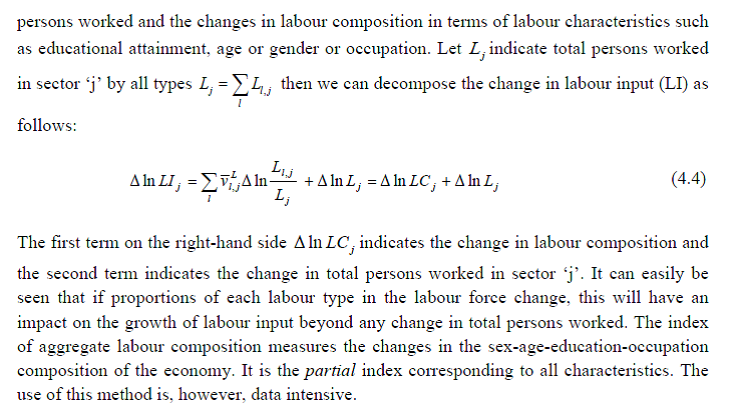

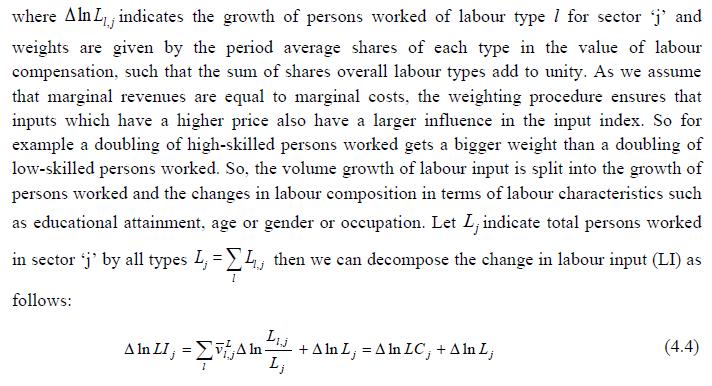

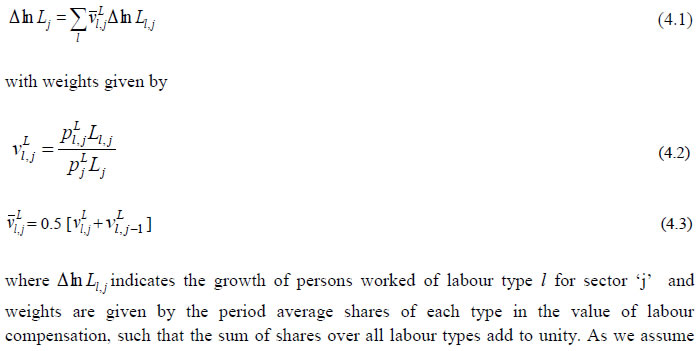

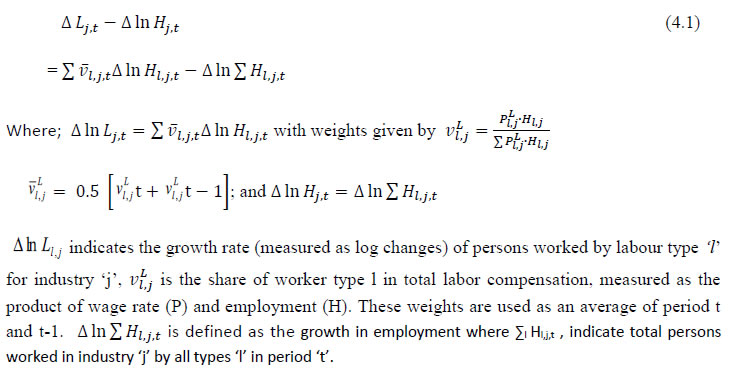

For extrapolation backward to 1980-81 to 1982-83, the interpolation of the broad industrial classifications of 32nd round (1977-78) and 38th round (1983-84) are used. Thus, the estimates from 32nd round are mainly used as control numbers. Between 2005 and 2011, we observed very high growth rate in number of employed persons series for the industry Electrical and Optical Equipment as compared to other manufacturing industries and the overall growth in employment in this industry during 2005-2011 was found to be higher than that for Construction (which seems somewhat unrealistic). It was also observed that there was a negative growth in employment in Textiles, Textile Products, Leather and Footwear although real GVA of this industry more than doubled between 2005 and 2011. To address these issues, some adjustments to the initial employment estimates for Electrical & Optical Equipment and Textiles, Textile Products, Leather and Footwear have been done.Onwards 2005, employment series for Electrical & Optical Equipment has been estimated applying annual growth rates obtained from ASI and NSSO rounds to the number of employed persons for the year 2005-06. Then, for the years 2005-06 to 2011-12, we compute the difference between estimated employment series from EUS rounds and that based on ASI & NSSO rounds for the Electrical and Optical Equipment industryand add it to Textiles, Textile Products, Leather and Footwear industry. This ensures that for the manufacturing as a whole our estimates remain the same as obtained from EUS rounds. 4.2 Estimation of Labour Quality index The quality of labour force is of considerable importance in the context of productivity measurement, and one of the widely used methodologies to capture changes in labour quality is given by Jorgenson, Gollop and Fraumeni (JGF) (1987). In growth accounting methodology of measurement of total factor productivity (TFP) when output growth is decomposed into growth of inputs and the residual TFP, then labour input is measured as an index of labour service flows. It accounts for changes in labour quality in terms of labour characteristics such as educational attainment, age (experience), gender, employment status, etc. and thus accounts for heterogeneity of the labour force. In our study, the index of aggregate labour quality measures the changes in the composition of labour in the economy. The present study has computed labour quality index by using only education characteristic in the JGF methodology. Thus, the data required for the labour quality index in the present case, is employment and earnings by education and by industry. The labour quality index has been computed using five education categories namely- up to primary, primary, middle, secondary & higher secondary, and above higher secondary. There are thus five types of persons employed for each of the 27 study industries. The quality growth rates are estimated for total persons employed in these industries in India for the 38th, 50th, 55th, 61st, 68th rounds of EUS by NSSO, and all the PLFS rounds since 2017-18. They are then indexed to 1983-84 (38th round) as the base, so as to assess the temporal changes in labour’s skill. Interpolation has been done between the major rounds for values of the intermediate years. Since the series is required from 1980-81, we have extrapolated it backwards from 1983-84 and the index is recomputed with base 1980-81 equal to 100. The following steps have been performed:

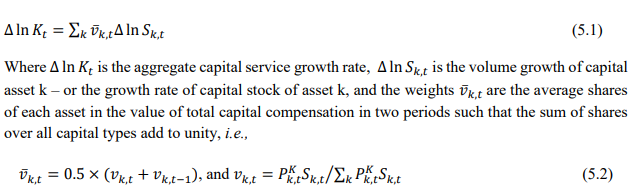

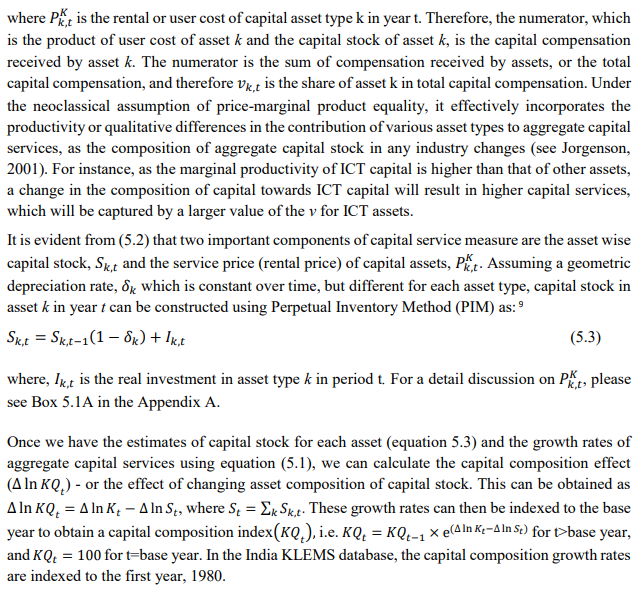

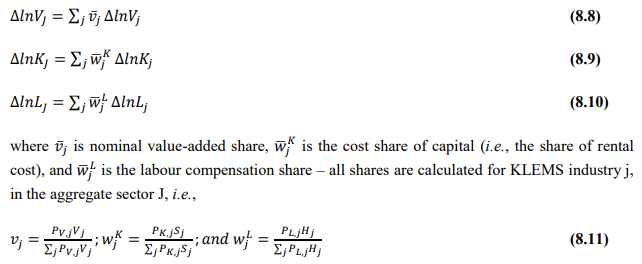

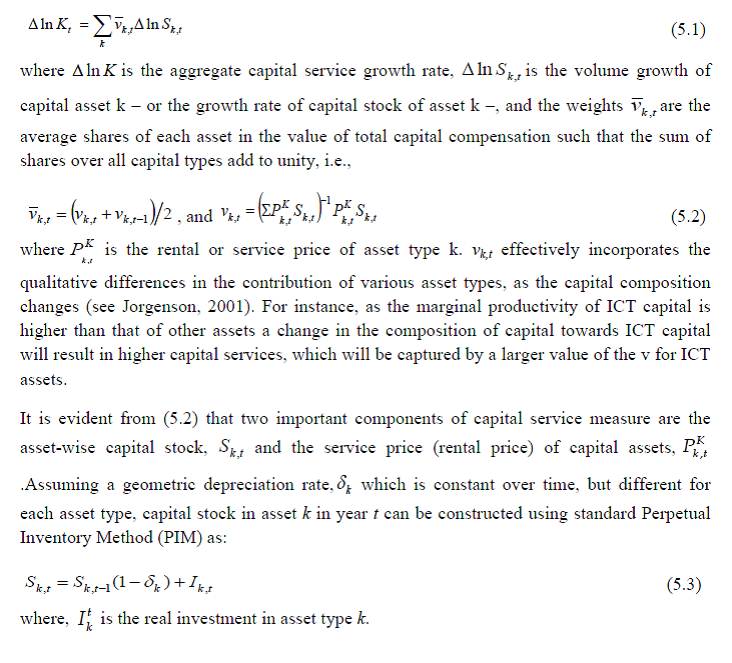

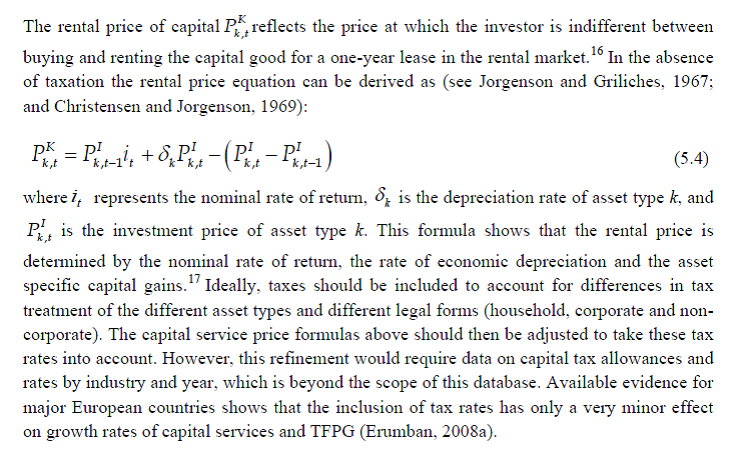

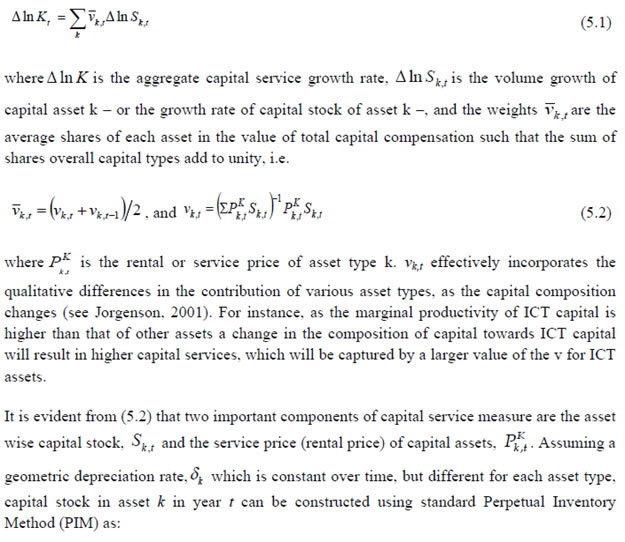

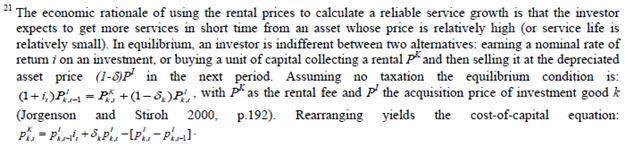

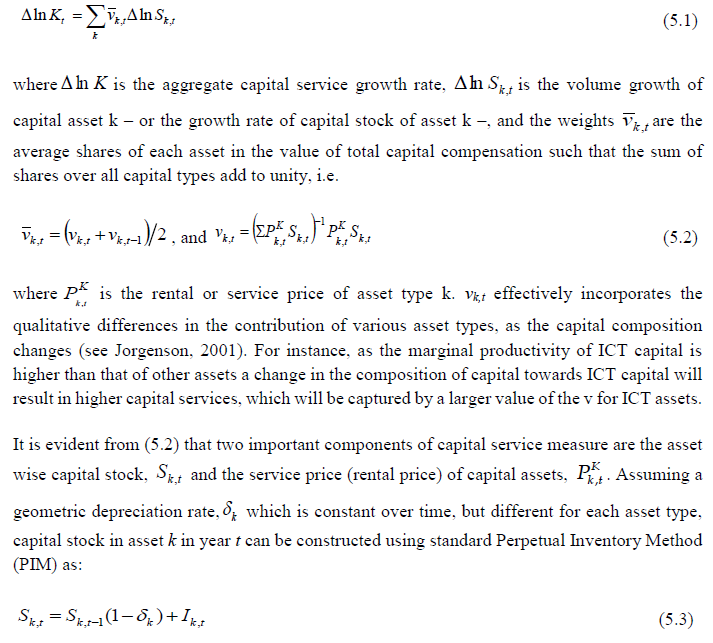

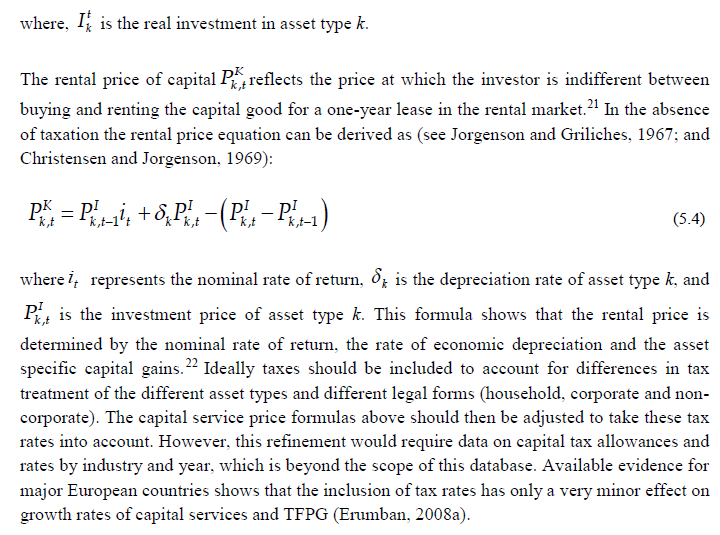

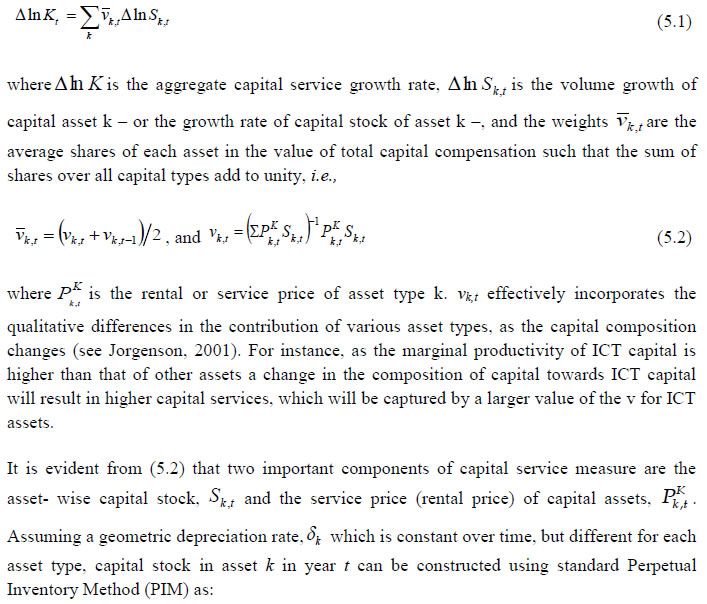

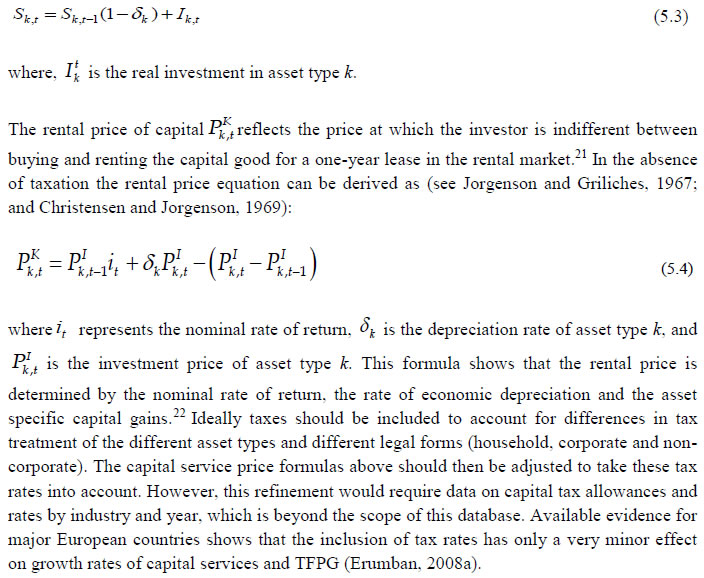

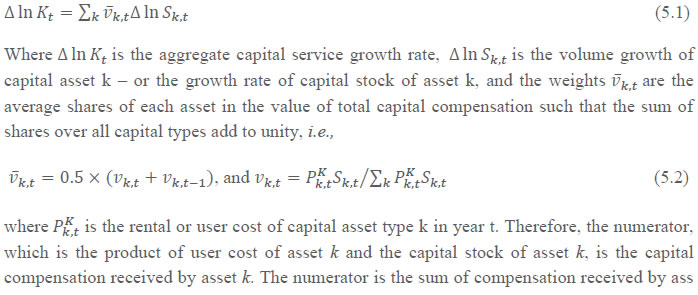

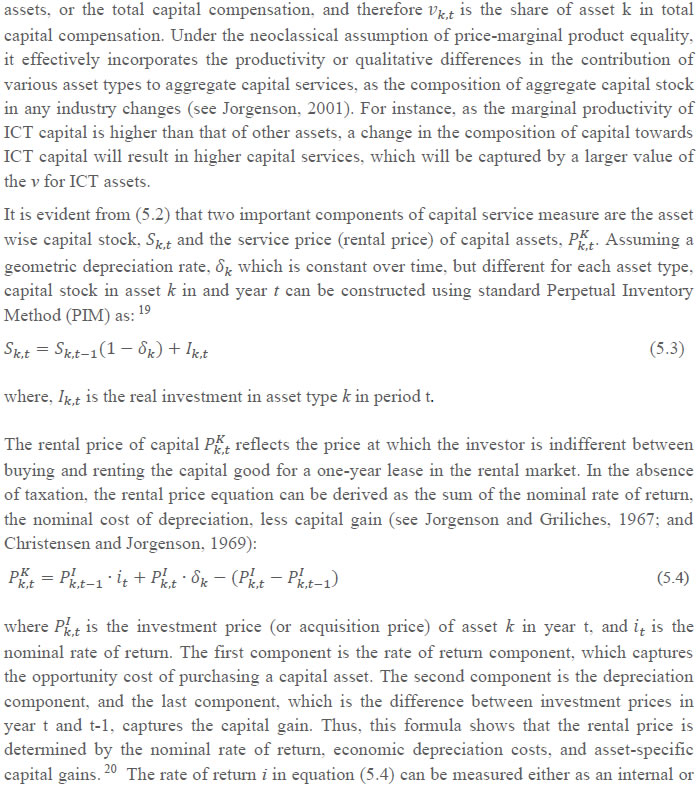

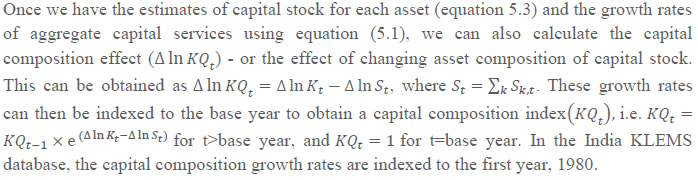

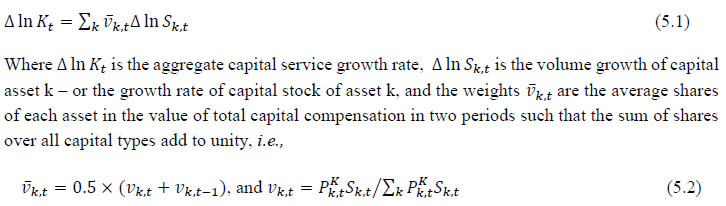

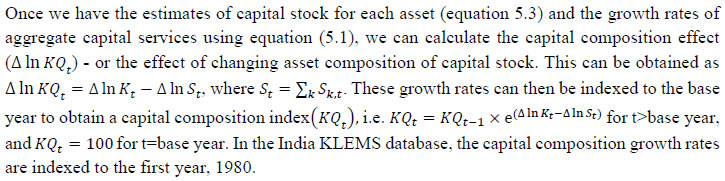

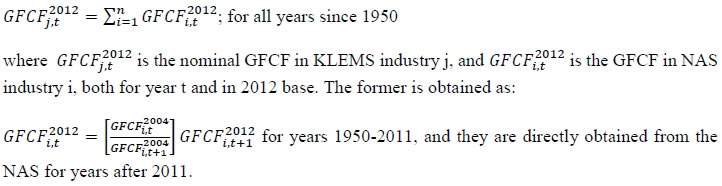

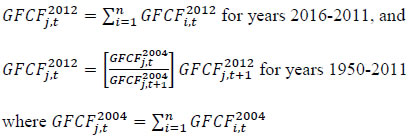

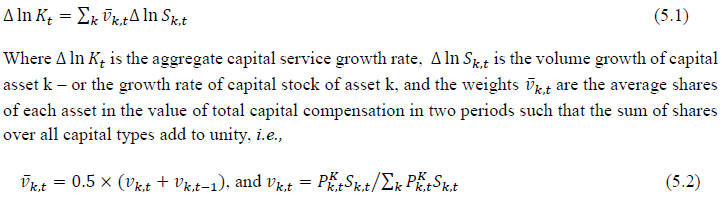

The first term of equation 4.1 indicates the changes in labour quality index, which is due to the changes in the composition of workers and the second term indicates the change in total persons employed in sector ‘j’. The index of aggregate labour quality thus measures the changes in the composition of labour in the economy The labour input (adjusted labour persons) then can be obtained by multiplying the number of persons employed by the corresponding labour quality index and the labour input growth is finally obtained by combining the growth of persons employed and the growth in the index of labour quality. Chapter 5: Capital Services Series at the Industry Level This chapter outlines the methodology employed to estimate capital Services for the 27 industries in India KLEMS database version 2024. All the productivity calculations in India KLEMS use capital services as an input to production, which is estimated using the approach developed by Jorgenson and Griliches (1967), and outlined in Jorgenson, Gollop, and Fraumeni (1987). The estimation of capital service growth rate is accomplished by first estimating capital stock for different assets, and then aggregating them across assets after correcting for the differences in their marginal productivities. Capital services account for the differences in marginal productivity between different asset types while capital stock measures only the vintages of capital, they do not account for asset heterogeneity. For instance, aggregate capital stock measures would assume that a computer's productivity is the same as that of a car. However, proper measures of capital stock would account for the decline in the efficiency of both computers and cars over their lifetime. Following an overview of the theoretical method to measure capital services (Jorgenson and Griliches,1967; JGF, 1987), the chapter discusses the specific empirical approaches we follow to implement these methods within the constraints of data availability for Indian industries. In India KLEMS, we have reported capital stock, capital services and the capital “capital composition effect”. Capital stock is reported in constant price volumes, and growth rates, while the latter two are reported in growth rates and indices. To measure capital services, using the Jorgenson and Griliches (1967) approach, we need estimates of capital stock for detailed asset types and the shares of each of these assets in total capital remuneration. The aggregate capital services growth rate is derived as a weighted growth rate of individual capital assets, the weights being the shares of each asset in the total compensation made to capital, i.e,   Since our measure of capital input takes account of asset heterogeneity, it was essential to obtain investment data by asset type. We distinguish between 3 different asset types – construction, transport equipment, and machinery (includes ICT and non-ICT machinery).10 We exploit multiple sources of information for the construction of our database on capital services. This includes the National Accounts Statistics (NAS) that provide information on broad sectors of the economy, the Annual Survey of Industries (ASI) covering the organized manufacturing sector, the National Sample Survey Office (NSSO) rounds for unorganized manufacturing and various Input-Output tables. Even though we use multiple sources of data, our final estimates are fully consistent with the aggregate data obtained from the NAS. In addition, our approach to capital measurement is consistent with international practices such as the EU KLEMS11, which ensures the possibility of international comparisons. In what follows, we discuss the various sources of data for asset wise investment and the construction of the relevant variables, in detail. (a) Asset-wise investment for broad sectors of the economy Industry-level estimates of capital input require detailed asset-by-industry investment matrices. NAS provides information on aggregate capital formation by industry of use for nine broad sectors, which, nevertheless, was not sufficient for our purpose. Therefore, we have collected more detailed data on assets and industries from the CSO12. This is the data underlying the published aggregate gross fixed capital formation by the broad industry groups, separately for public and private sectors. For those sectors for which the investment matrices were not available from CSO, we gather information from other sources (e.g. ASI for organized manufacturing and NSSO surveys for unorganized manufacturing) and benchmark it to the aggregate investment series from the National Accounts. The data used in the current version of the India KLEMS is based on the revised NAS with 2011-2012 base and is available only since 2012. Therefore, for earlier years, we extrapolate the series using growth rates from previous version of the data. Table 5.1 provides an overview of asset types available in NAS and their corresponding asset types used in our study. Investment in education and health are obtained directly from national accounts for the period after 2012, for each asset. For years before 2012, we assume the trend in the distribution of output, in order to split the total investment in the aggregates of these sectors into sub-sectors.

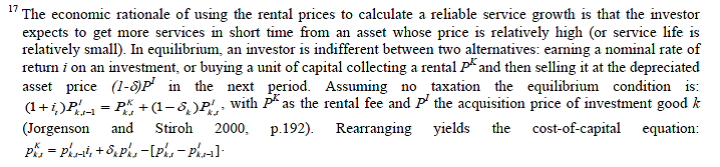

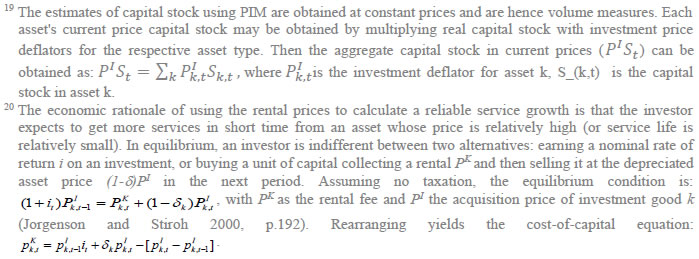

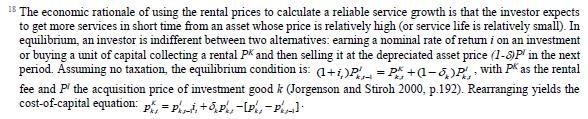

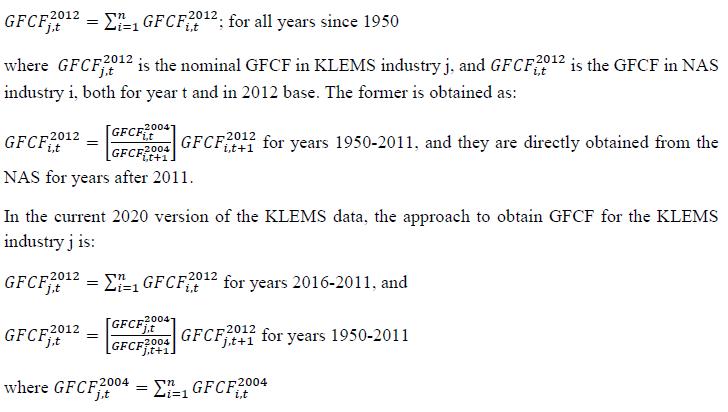

Total investment in each asset category is calculated as the sum of private and public-sector investment in each asset. Investment in transport equipment was not available separately for the private sector industries. Therefore, we distributed the NAS total machinery in the private sector using the industry distribution of machinery and transport equipment. These estimates are then subtracted from each industry’s total machinery & transport equipment data to obtain the transport equipment investment in the private sector industries. Using this approach, we could generate investment in transport equipment by industries for the period 1950-2016. We assumed the share of transport equipment in the total machinery and equipment to remain unchanged in subsequent years while estimating nominal investment in transport equipment in the similar way. The nominal investment was deflated using GFCF deflator for transport equipment (see section (c)). Since the distinction between registered and unregistered manufacturing is not available in the NAS since 2016, we used a quick fix to split these two. NAS provides a division between the corporate sector, public sector, and household sector. In the current version of the data, we consider the household sector as a proxy for unregistered and the corporate and public sector as a proxy for the registered sector. As mentioned earlier, the updates for years since 2017-18 are solely based on published aggregate GFCF data from the National Accounts. While extending the past series of detailed asset-wise investments forward for years since 2017-18 using the NAS-published headline series, we now consider the published NAS series as the benchmark since 2012. Then we apply the industry distribution of the 2012-2016 detailed series obtained previously from the CSO14. (b) Asset-wise investment for non-NAS sectors NAS provides data only for 9 broad sectors, while we have 27 industries, which necessitated further splitting of some of the NAS sectors. This includes aggregate manufacturing (registered and unregistered separately for the period 1950-2016) with 13 sub sectors; other services into 4 sub sectors; and real estate activities and business services into 2 sub sectors. The manufacturing sector investment data was disaggregated into 13 subsectors at the 2-digit level of NIC 1998 using ASI and NSSO data, which will be discussed in detail subsequently. Investment series in service sector has been split into sub sectors using two alternative approaches–value added shares, and capital/labour ratio in the higher aggregate industry. However, the final data used are based on value added shares, as we did not see any significant difference between the two. Registered (organized) Manufacturing: In order to split the aggregate capital formation in organized manufacturing sector into 13 study sectors, we use the ASI. ASI defines GFCF as actual additions (newly purchased, second hand and own construction) minus deductions plus depreciation adjustment for discarded assets during the year. This approach is based on a single year’s sample and helps to avoid potential huge negative investment series and is also consistent with published ASI GFCF series. The yearly detailed volumes beginning 1964-65 were used to derive the gross fixed capital formation by asset type directly. For the years 1964-1978, the relevant data are obtained from published detailed volumes. For the period, 1983-84 to 2004-05, ASI has generated detailed tables from Block C of ASI schedule that contain data on fixed assets. Data for the missing years are interpolated using changes in investment based on book value method15. Table 5.2 provides an overview of the asset categories available in ASI, and the relevant asset categories in our study to which they are attributed. Though ASI provides investment in land, for reasons of NAS consistency we exclude it from our database. Once investment in each of these assets and industries are generated using ASI data, we apply this industry-asset distribution to the published aggregate NAS GFCF series for organized manufacturing sector. It may also be noted that from 1960-61 to 1971-72, ASI data are for the census sector and from 1973-74 onwards they are for the factory sector. In order to make these two series comparable over years, we convert the data prior to 1972 to factory sector using the factory/census ratio in 1973. Thus, after these adjustments, we obtain investment data for 13 manufacturing sectors, by asset types, consistent with the NAS aggregate for registered manufacturing. This approach was accurate for the period 1950-2016 when the NAS provided aggregate registered manufacturing GFCF data. For the years after 2016, since when NAS does not provide registered manufacturing aggregate, we proxy registered manufacturing by the sum of public sector and corporate sector. Unregistered (unorganized) Manufacturing: The data required for creating the gross investment series for the 13 sectors of the unorganized manufacturing sector are obtained from various rounds of NSSO surveys on unorganized manufacturing. We use 6 rounds of NSSO surveys that cover the period 1989-2016. These are 45th round (1989-90), 51st round (1994-94), 56th round (2000-01), 62nd round (2005-06), 67th round (2010-11) and 73rd round (2015-16). Unit level data has been aggregated to 13 industries using the appropriate concordance. NSSO provides net addition to owned assets during the reference year within the block of fixed assets, and we use this as a measure of our investment. The investment series arrived at for six rounds were interpolated to obtain the annual time series of unorganized gross fixed capital formation by asset type. As in the case of registered sector, once the investment by asset types across industries are constructed, the asset-industry distribution is applied to the published NAS aggregate GFCF in unregistered manufacturing to obtain NAS consistent GFCF by asset type and industries. (c) Investment Prices by Asset Types In order to compute asset wise capital stock using PIM (equation 5.3) and rental price (see Box 5.1A in the Appendix), we require asset wise investment price deflators. Since CSO has provided us with investment data by industries and assets both in current and constant prices, we could derive the price deflators with base 2011-2012. For years before 2011, prices were spliced using 2004-2005 base investment deflators. These deflators are directly used for all the three asset categories we have. Since there was no separate asset wise data available for transport equipment in 2017-2018, the investment deflator for transport equipment from 2016-2017 was extrapolated using the trend in the investment price of total machinery & equipment, obtained from NAS. (d) Initial Stock, Depreciation Rates and Rate of Return For the implementation of PIM to estimate asset wise capital stock, we require an estimate of initial benchmark stock (see Erumban, 2008b for an in-depth discussion on this issue). NAS provides estimates of net capital stock since 1950 for all the broad sectors in its Statement 17: Net Fixed Capital Stock by industry of use. We take the NAS estimate of real net capital stock in 1950 (in 1999-2000 prices) as our benchmark stock for all non-manufacturing sectors, and for manufacturing sectors the same is taken for the year 1964.16 However, since the NAS estimate is available only for broad sectors and for aggregate capital, we use our industry-asset distribution of GFCF in order to create net fixed capital stock estimates by asset type for all the 27 sectors. The approach to split asset-wise capital stock is changed in the 2020 version of the India KLEMS database. Instead of using the GFCF distribution, we use the distribution of net capital stock by assets, available from the detailed asset data obtained from the CSO. Since the initial stock depreciates over the years, the impact of this change in distribution on the capital stock will vanish over the years at the individual asset level. However, as it changes the distribution of assets in the total capital stock, these compositional changes tend to have a visible impact on the aggregate capital stock, causing a historical revision of capital stock growth rates in some industries (esp. transport and storage, education, hotels and restaurants, electricity, transport equipment, etc.). NAS also provides detailed tables on assumed life of assets used for computing capital stock, for private units, administrative units as well as departmental and non-departmental units by asset types.17 We use these estimates of lifetime to derive appropriate depreciation rates for non-ICT assets, using a double declining balance rate. Following the NAS, we assume 80 years of lifetime for buildings, 20 years for transport equipment, and 25 years for machinery and equipment (see Appendix 26.2; CSO, 2007). The final depreciation rates used in the study are given in Table 5.3 by asset type. Subsequently, we build our capital stock series by asset types for all the 27 industries using our GFCF series from 1950 (1964) onwards for the non-manufacturing (manufacturing) sectors. Our measure of capital input is arrived using equation (5.1), for which we also require estimates of rental prices (see Box 5.1A in the Appendix). Assuming that the flow of capital services is proportional to the capital stock at individual asset level, aggregate capital flows can be obtained using a Translog quantity index by weighting growth in the stock of each asset by the average shares of each asset in the value of capital compensation, as in (5.1). The rate of return (i) in equation (5.4) represents the opportunity cost of capital, and can be measured either as internal (or ex post) rate of return, or as an external (ex ante) rate of return.18 The present version of the database uses an external rate of return, proxied by average of return on government securities and prime lending rate obtained from the Reserve Bank of India19. Therefore, we use a real rate, which is net of capital gain. Hence, the capital gain component in equation is excluded while estimating rental price using external rate of return, obtaining  Where r is the real rate of return, nominal interest rate adjusted for consumer price inflation rate. The consumer price indices (CPI) are obtained from IMF and World Bank. The measures of capital input available in India KLEMS are based on only three asset categories, construction, machinery, and transport equipment. Therefore, it does not consider the enormous and distinct role of ICT capital in contributing to productivity and growth. The absence of ICT estimates in the database is driven by insufficient data on investment in ICT assets, such as hardware, software, and communication equipment in the National Accounts. However, during recent years, NAS has extended its asset coverage to include software and ICT equipment. Erumban and Das (2016) have made some estimates for the aggregate economy using input-output tables for ICT equipment and relying on NAS for software investment. Similarly, Erumban and Das (2020) have made some initial estimates of ICT capital by industries, which still remains a challenging task. Nevertheless, now that more data is available from NAS, it is possible to explore this further, and future extensions of the database may explore this. Similarly, following the SNA 2008 guidelines, the NAS now provides estimates of intangible capital such as intellectual property and research and development (R&D), which may be a useful extension to the capital input database. Two additional challenges are arising since the new system of national accounts. The first is the lack of separate data on registered and unregistered manufacturing, which poses challenges in using ASI and NSSO data to split aggregate manufacturing data into 13 industry groups. Instead of the registered and unregistered split, CSO now provides a division between the household and corporate sectors. We currently address this challenge by considering the household sector as unregistered manufacturing and the sum of public and corporate sectors as a registered sector. The second challenge is the lack of separate data on transport equipment and machinery assets in the new series of national accounts, which follows United Nation's System of National Accounts (SNA)-2008. Although, for the time being, we adopt ad-hoc approaches to fix this, it cannot be adopted on a long-term basis, which might necessitate combining transport equipment and machinery to one single asset. Finally, as mentioned earlier, the debate on whether it is appropriate to use an external rate of return or an internal rate of return is unsettled in the literature. It may be worth exploring estimates of capital using the internal rate of return. Appendix A: Some Discussions on the Estimation of Capital Services

Chapter 6: Intermediate Input Series at the Industry Level In this section, we describe the basic approach we have used to derive the volume series of Intermediate Inputs namely –Energy input (E), Material input (M) and Services input (S). The methodology for measuring industry output, intermediate inputs and value added was developed by Jorgenson, Gallop and Fraumeni (1987) and extended by Jorgenson (1990 a). The cornerstone of this approach is a time series of input output (IO) tables which gives the flows of all commodities in the economy, as well as payments to primary factors. Following a similar approach as explained in Jorgenson et al. (2005, Chapter 4) and Timmer et al. (2010, Chapter 3), the time series on intermediate inputs for the India KLEMS project have been constructed. Definition of EMS: As in EU KLEMS, this study identifies three main categories of Intermediate inputs. They are classified as follows:

The following five energy types (and products) have been classified as the Energy input:

The following fourteen input items have been classified as the Service input:

All other intermediate inputs barring the above mentioned nineteen inputs are classified as material input. The methodology for computation of Intermediate Input Series for 27 Industries from 1980-2023 at current and constant prices is explained in steps. Step 1: Concordance is done between IOTT and study industries

Step 2: Obtaining estimates for Material, Energy and Service Inputs for 27 Industries, in benchmark years

Thus, for each of the benchmark year, estimates are obtained for Material, Energy and Service Inputs that has been used to produce Gross output in the 27 different India KLEMS Industries. Step 3: Projecting a time series (1980 to 2019) of proportions of Material, Energy and Service Inputs in Total Intermediate Inputs for each of the 27 industries

There exists some abnormal fluctuation in the proportions of Material Inputs, Energy Inputs, and Service Inputs in Total Intermediate Inputs for benchmark years. In that case, we drop that specific benchmark proportion and linearly interpolate of the adjacent benchmark proportions to estimate proportion for intervening years. For the industry ‘Wood & Wood Products’, we estimated proportions of Material Inputs, Energy Inputs, and Service Inputs in Total Intermediate Inputs from SUT 2015-16 instead of Input Output Transaction Table 2015-16. For the industry group ‘Coke, Refined Petroleum and Nuclear Fuel’, we estimated proportions of Material Inputs, Energy Inputs, and Service Inputs in Total Intermediate Inputs from ASI data instead of Input Output Transaction Table. This has been done because the relevant proportions differed significantly between the input-out tables and ASI, and the latter is believed to be making a more correct assessment of energy inputs used in the Coke and Petroleum products industry. Step 4: Consistency with NAS The projection of intermediate input vector, using IOTT in Step 3 needs to be consistent with the estimated output from NAS.

1. For Benchmark years: Ratio of Total Intermediate inputs from NAS to that from IOTT is adjusted proportionately to the absolute value of Energy Inputs/Material Inputs/Service Inputs obtained from IOTT. 2. For Intervening Years: The interpolated proportions of Energy Inputs, Material Inputs and Services Inputs obtained from IOTT, is applied directly to the total intermediate inputs from NAS to get each inputs share. Steps 1-4: This gives a time series of Material, Energy, and Service Inputs for 27 study Industries from 1980 to 2023 at current prices. Steps 5 and 6 below, explain the methodology for computation of Intermediate Input Series for 27 study Industries from 1980 to 2023 at constant price. The approach followed here is to first form the aggregates of materials, energy and services at current price for each study industry from the benchmark Input Output tables and then develop deflators of Materials, Energy and Service Inputs for each of the 27 study Industries separately. Step 5: Constructing Deflators of Materials, Energy and Service Inputs for 27 study Industries separately

Step 6: Computing Time Series on Intermediate Input for 27 study Industries from 1980-2023, Constant prices

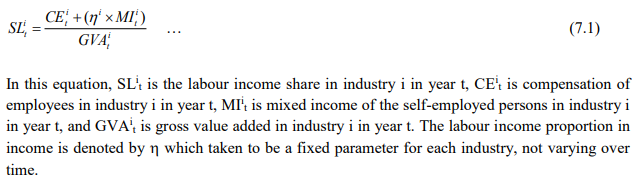

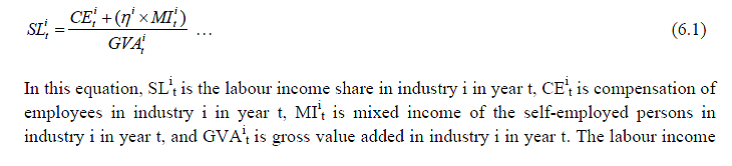

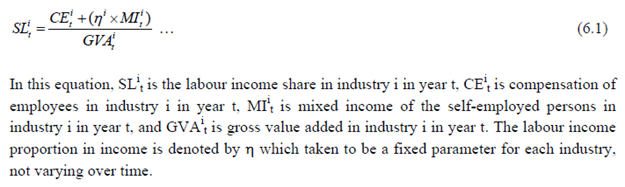

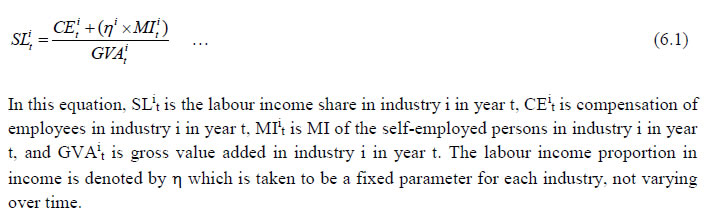

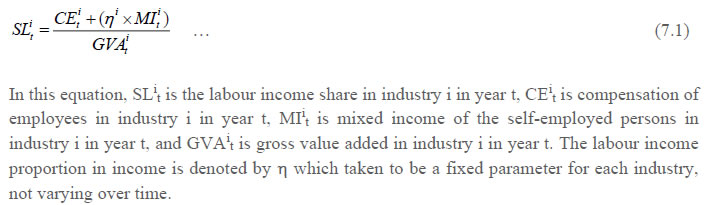

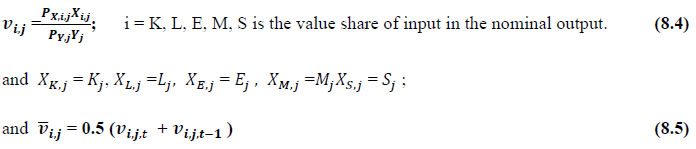

Thus, we have a time series of Material, Energy and Service Inputs for 27 study Industries at constant prices. Chapter 7: Factor Income Share Series at the Industry Level The distribution of income between capital, labour and intermediate inputs, is an important element in growth accounting because income shares, under conditions of competitive markets, can be used to measure the contributions each factor makes towards output growth. 7.1 Methodology for Measuring Labour Income Share Series Under the assumption of constant returns to scale with two factors of production i.e., labour and capital, the sum of the labour income share and capital income share is 1. The labour income share is defined as the ratio of labour income to GVA. Capital income share is accordingly obtained as one minus labour income share. There are no published data on factor income shares in Indian economy at a detailed disaggregate level. National Accounts Statistics (NAS) of the CSO publishes the NDP series comprising of compensation of employees (CE), operating surplus (OS) and mixed income (MI) for the NAS industries. The income of the self-employed persons, i.e., mixed income (MI) is not separated into the labour component and capital component of the income. Therefore, to compute the labour income share out of value added, one has to take the sum of the compensation of employees and that part of the mixed income which are wages for labour. The computation of labour income share for the 27 study industries involves two steps. First, estimates of CE and MI have to be obtained for each of the 27 study industries from the NAS data which are available only for the NAS sectors (see Table 7.1). Second, the estimate of mixed income has to be split into labour income and capital income for each industry for each year (except for those industries for which the reported mixed income is zero, for instance, public administration). Basis data sources used for the computation of labour income share are NAS, ASI and unit level data of survey of unorganized manufacturing enterprises. These data sources are used to obtain estimates of CE, OS and MI for each of the 27 study industries. For splitting the labour and non-labour components out of the mixed income of self-employed, the unit level data of NSS employment-unemployment survey are used along with the estimates of CE, OS and MI basically obtained from the NAS. a) Construction of Labour Income Share Series in Gross Value Added The estimation of labour income share for the 27 study industries has been done in two steps, as discussed below. Step 1: Estimation of CE, OS and MI for the 27 study Industries NAS provides estimates of compensation of employees (CE), operating surplus (OS) and mixed income (MI) for the 9 NAS industries in different annual Sequence of National Accounts reports. For some industries under study, for instance (i) Agriculture, forestry & logging and fishing, (ii) Mining & Quarrying, (iii) Electricity, gas and water supply and (iv) Construction, the required data are readily available from NAS. For others, the estimates available in NAS have to be distributed across the study industries using ASI data. The NAS estimates of factor incomes (CE) for registered manufacturing is split into KLMES 13 industries (3-15) in proportion to the reported ASI data on emoluments for various industries. Estimate of factor incomes for ‘other services’ in NAS has been split into estimates for (i) Education, (ii) Health and Social Work, and (iii) Other Community, Social and Personal Services including Renting of Machinery and Business Services, and Private Household with Employed Persons. Before 2011-12, NAS provides estimates of factor incomes for registered manufacturing and unregistered manufacturing, but not for individual manufacturing industries. However, 2011-12 onwards NAS disaggregated the manufacturing sector in corporate sector and household sector. The NAS estimates of factor incomes for registered manufacturing and corporate sector have to be split into various manufacturing industries considered in the study (13 in number) using ASI data. The reported CE in NAS for registered manufacturing and corporate sector has been distributed into those 13 industries in proportion to the reported ASI data on emoluments for various industries. In a similar way, using ASI data, the estimate of OS for registered manufacturing and corporate sector has been distributed. Emoluments are subtracted from gross value added for various industries yielding capital income. The share of different industries in aggregate capital income of organized manufacturing indicated by the ASI data is used to split the estimate of OS for registered manufacturing and corporate sector reported in the NAS. The methodology applied for unregistered manufacturing and household sector is similar. The published results and unit level data of survey of unorganized manufacturing industries have been used for this purpose. The estimates of wage payments (to hired workers) in different industries have been used to split (proportionately) the estimate of CE in the NAS for aggregate unregistered manufacturing. The estimated wage payment is subtracted from the estimated value added to obtain an estimate of capital income and mixed income of the self-employed in various unorganized manufacturing industries. The estimate of MI provided in NAS for unregistered manufacturing and household sector has then been proportionately distributed across industries using the estimate of capital income and mixed income of the self-employed in various industries that could be formed on the basis of published results and unit level data of survey of unorganized manufacturing industries. Unlike the ASI data for organized manufacturing, the data for unorganized manufacturing enterprises are available for only select years. The proportions mentioned above could therefore be computed only for those select years (data for six rounds have been used; these are for 45th Round (1989-90), 51st Round (1994-95), 56th Round (2000-01), 62nd Round (2005-06), 67th round (2010-11) and 73rd Round (2015-16)). It has accordingly, been necessary to resort to interpolation/ extrapolation to obtain the relevant proportions for other years. Step 2: Splitting of MI into Labour Income and Capital Income As explained above, the income share of labour is computed as:  The derivation of the GVA series for different industries has been briefly explained in Chapter 2. The derivation of CE and MI series has been explained in step I above. Therefore, only the estimation method of η needs to be described. The estimation of η has been done with the help of NSS survey-based estimates of employment of different categories of workers (number of persons and days of work) and wage rates (which has been described briefly in chapter 4) coupled with estimates of MI, basically obtained from the NAS. Two approaches have been taken to get an estimate of η, and the labour income share series for different industries finally adopted in the study makes use of an average of the estimates of η obtained by the two approaches. In the first approach, an estimate of labour income of self-employed workers has been made for each study industry for eight years, 1983-84, 1987-88, 1993-94, 1999-00, 2004-05, 2009-10, 2011-12 and 2015-16 on the basis of the estimated number of self-employed, wage rate of self-employed and the number of days of work per week. The industry-wise estimates of number of self-employed, wage rate of self-employed and the number of days of work per week have been made from unit records of NSS employment-unemployment survey (major rounds) of 1983, 1993-94, 1999-00, 2004-05, 2011-12, and PLFS from 2017-18 onwards. The estimates of the number of self-employed, wage rate of self-employed and the number of days of work per week provide an estimate of the annul labour income of self-employed workers which is divided by the mixed income of self-employed (derived from NAS) to get an estimate of η. For five industries, the ratio in question has been computed and applied. For the other 22 industries, the ratio in question has been computed after clubbing the industries into 11 industry groups.21 In the latter case, a common ratio computed for group of industries has then been applied to constituent industries. The list of industries or industry groups for which η has been estimated is given in Table 7.2. In the second approach, the NSS data are used to compute the following ratio: the ratio of labour income of self-employed workers to the labour income of regular and casual workers. Let this be denoted by θ. Then, the estimate of CE provided in the NAS is multiplied by θ to obtain an estimate of the labour income component out of the MI reported in the NAS. The labour component of MI divided by total MI gives an estimate of η. In case the estimated labour component of MI exceeds the estimate of MI, the estimate of η has been taken as unity. Examining the estimates obtained by the first approach, it was found that the estimated labour income share out of mixed income varied significantly among the estimates for the seven years for which the ratio in question has been estimated. The estimates of η obtained by the second approach has the problem that in a number of cases, the estimated labour component of MI exceeds the estimate of MI given in the NAS, and therefore η is taken as one. The method finally adopted is as follows: (a) The average value of η has been computed for each industry or industry group by taking the estimates for the years 1983-84, 1987-88, 1993-94, 1999-00, 2004-05, 2009-10, 2011-12 and 2015-16. This has been done separately for the estimates based on approach-1 and those based on approach-2. (b) The estimates of η obtained for each industry or industry group by the two approaches have then been averaged. (c) Having obtained an estimate of η, equation 7.1 given above has been applied to compute the labour income share. Construction of Factor Income Share Series in Gross output The income share of labour, capital and intermediate inputs in Gross output has been computed using the following steps:

The splitting of unorganized sector factor incomes into individual industries has been done using unorganized survey results. The proportions computed for 1983-84 has been applied for the period 1980-81 to 1983-84. While there were surveys of unorganized manufacturing enterprises in 1978-79 the survey results have not been used for estimation of factor incomes in different industries of the unorganized manufacturing sector. Chapter 8: Growth Accounting Methodology

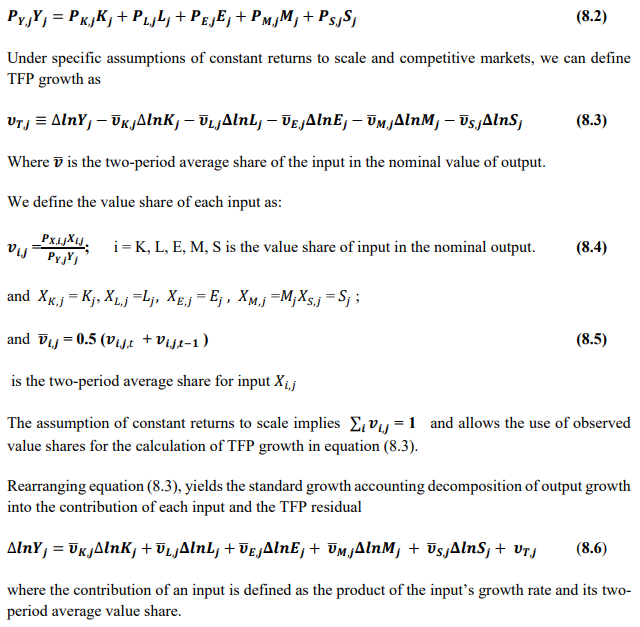

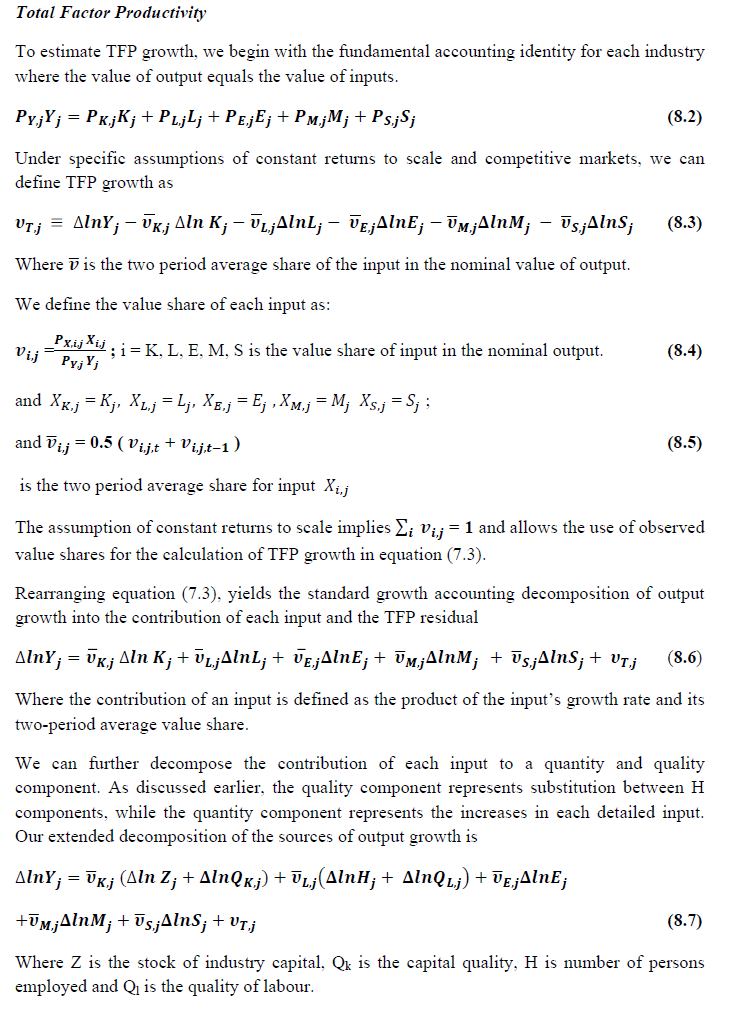

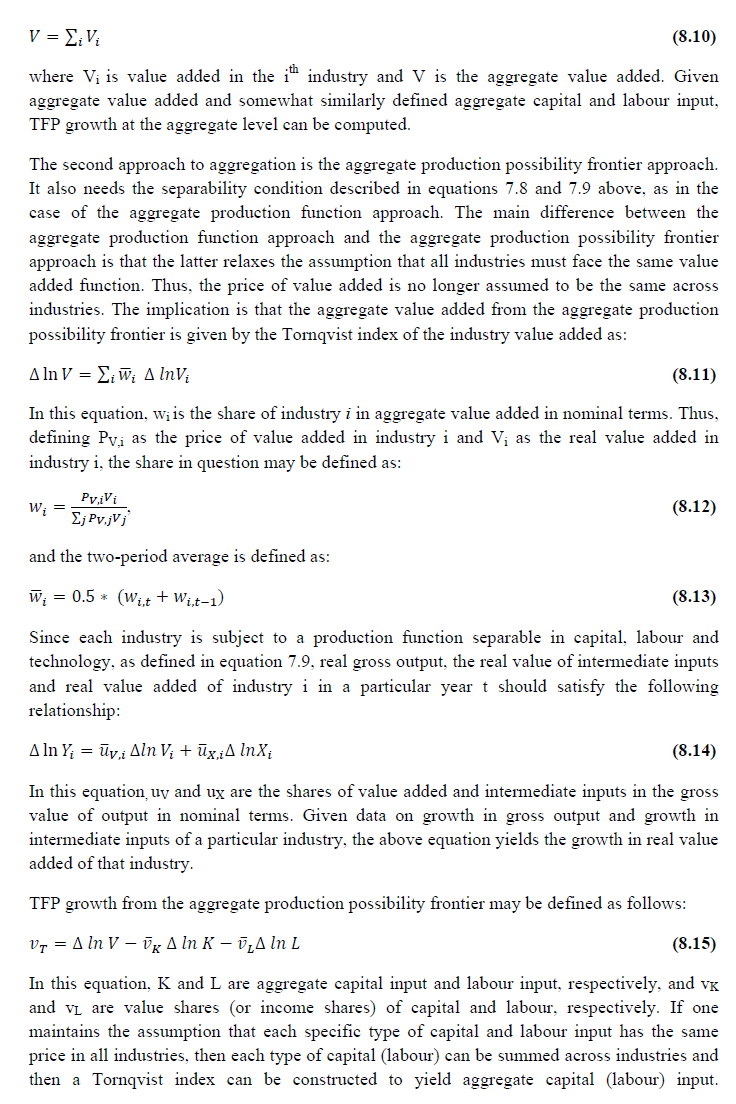

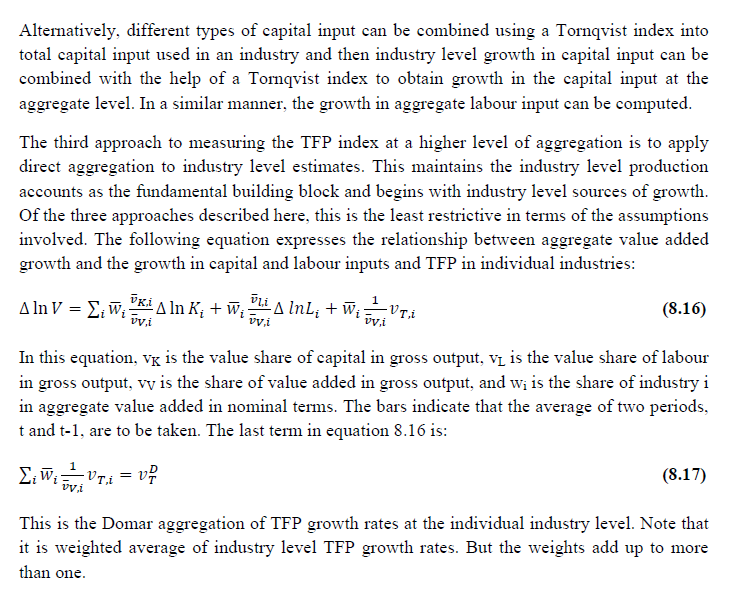

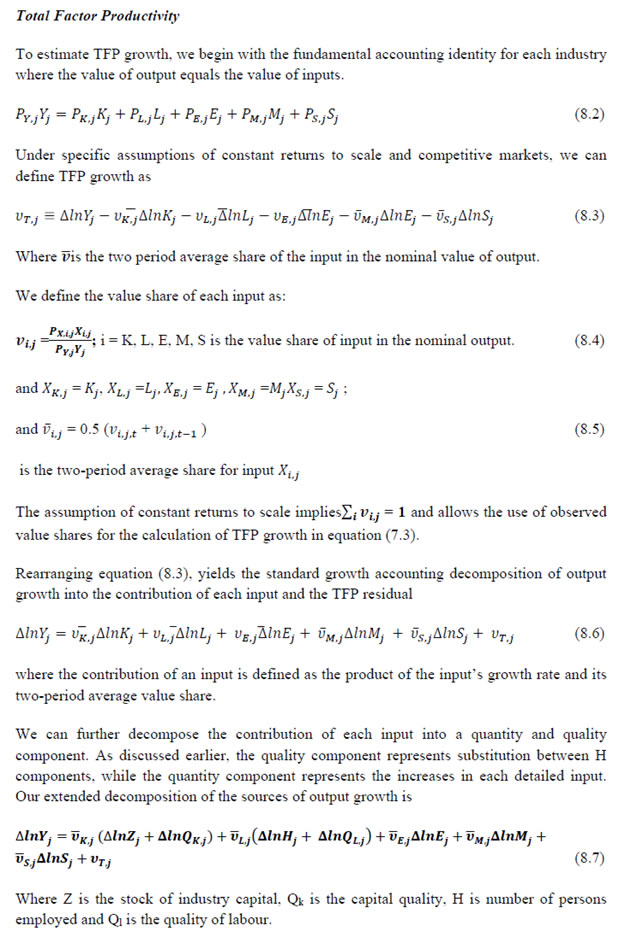

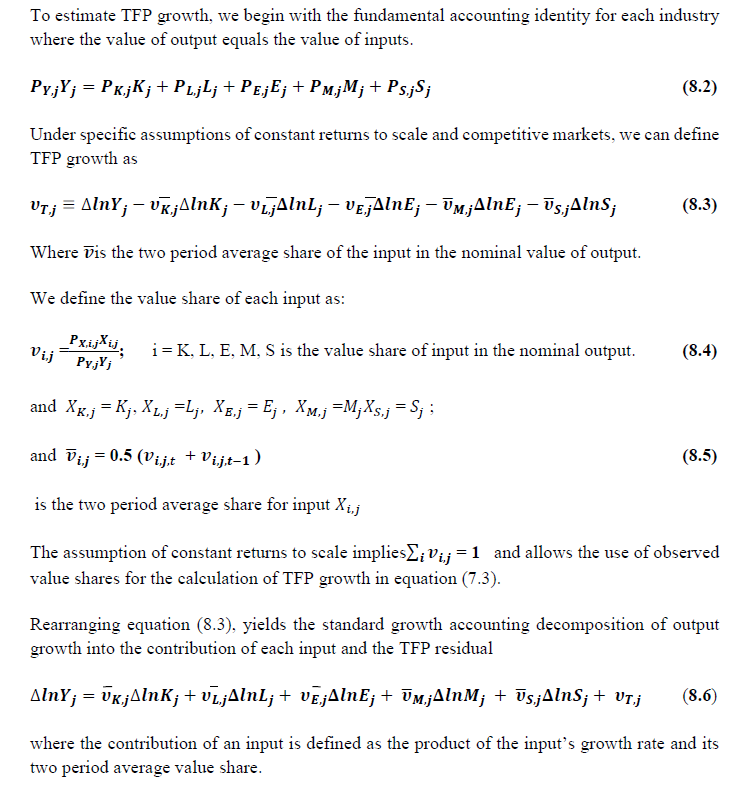

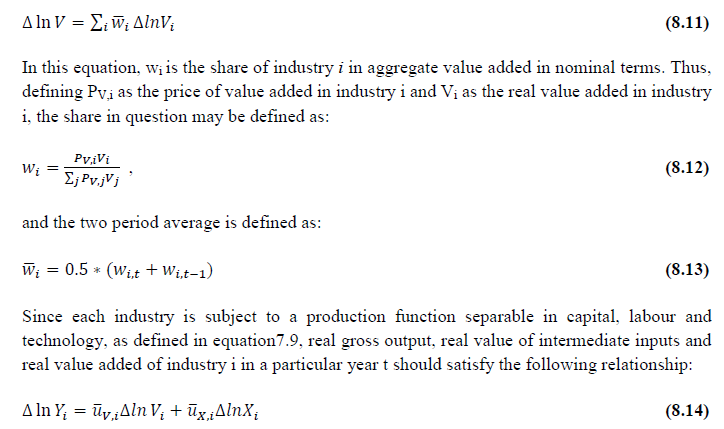

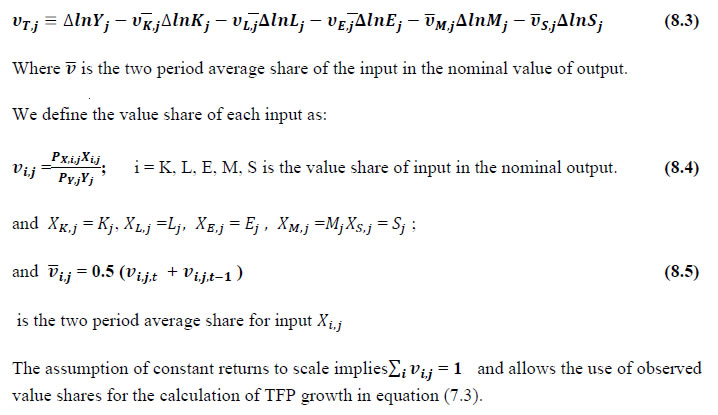

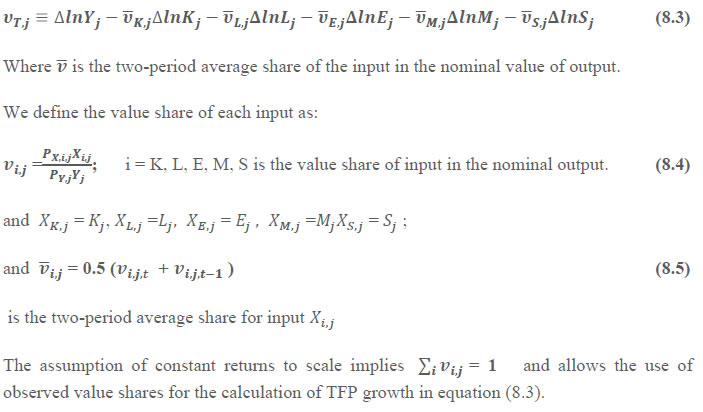

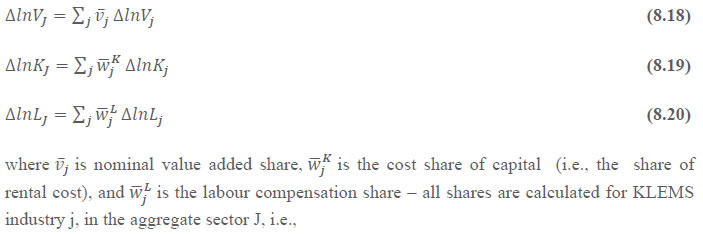

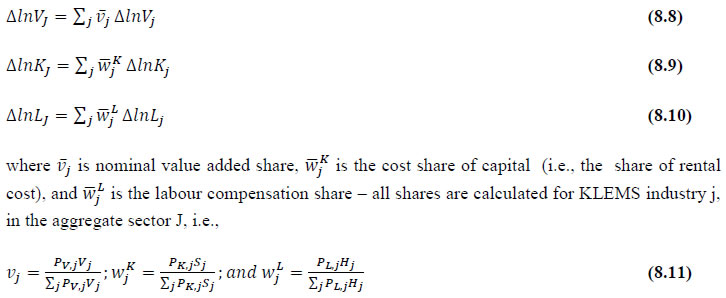

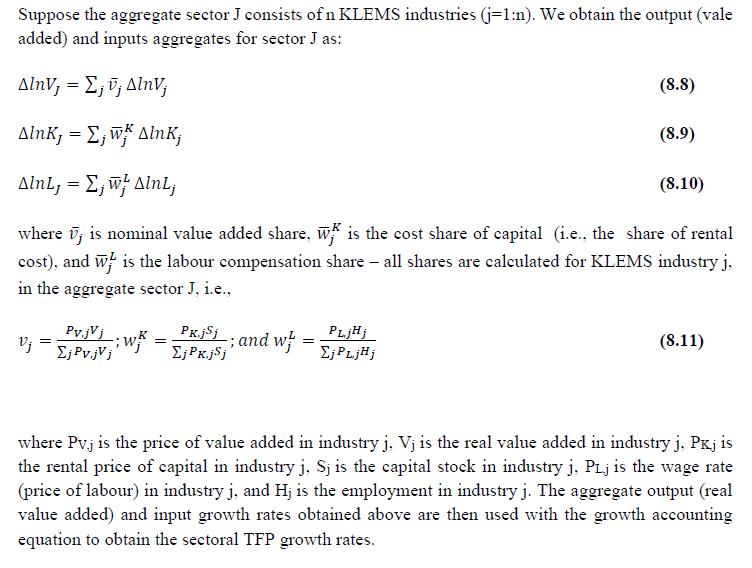

This chapter deals with the methodology of measurement of total factor productivity (TFP) growth for individual industries in the KLEMS framework and the aggregation from industry level productivity measures to measures for broad sectors and the economy as a whole. The methodology of analysis of sources of gross output growth at the individual industry level and sources of GVA (Gross Value Added) or GDP growth at the broad sector level and economy level will also be presented in this chapter 8.1 Methodology for Measuring Productivity Growth at the Industry level The production function Our measurement of TFP growth for different industries of the Indian economy is based on a gross output production function for each industry j:  Y is industry gross output, L is labour input, K is capital input and E, M and S are intermediate inputs-namely energy, material and services and T is an indicator of technology for industry j. All variables are indexed by time (t subscript is suppressed). There are several things to note about the production function - (1) all variables are aggregates of many components that have been discussed in the earlier report/chapters; (2) we assume that the industry production function is separable in these aggregates; (3) time (indicator of technology) enters the production function symmetrically and directly with inputs. An important feature of the gross output approach is the explicit role of intermediate inputs. In our study, we have considered three intermediate inputs - energy, material and services and this is important as we may find that intermediate inputs are the primary component of some industries outputs22. Failure to quantify intermediate inputs leads us to miss both the role of key industries that produce intermediate inputs and the importance of intermediate inputs for the industries that use them. To estimate the contributions of total factor productivity, and inputs to industry level output growth, based on the above-mentioned production function, we construct real values of inputs and output, using industry level price data for capital, labour and intermediate inputs, and output. e.g., PYj; PLj, PKj; PEj. PMj, PSj. The industry price of an input varies across industries due to compositional effects as industries expend different shares of their investment on each type of asset. The same is true for all inputs. Total Factor Productivity To estimate TFP growth, we begin with the fundamental accounting identity for each industry where the value of output equals the value of inputs.  We can further decompose the contribution of each input into a quantity and quality component. As discussed earlier, the quality component represents substitution between H components, while the quantity component represents the increases in each detailed input. Our extended decomposition of the sources of output growth is given as follows:  Where Z is the stock of industry capital, Qk is the capital quality, H is number of persons employed and Ql is the quality of labour. The data series at individual industry level constructed for gross value added and gross output, labour input, capital input, intermediate inputs and factor income shares (described in Chapters 2, 3, 4, 5, 6 and 7, respectively) are used to estimate TFPG during the period 1980 to 2019. Labour input is measured by using total person worked along with the labour quality index (see Chapter 4 for a detailed discussion). The series on growth rate in capital services forms the measure of growth in capital input (discussed in Chapter 5). TFPG estimation is done by using the gross output function framework23 (i.e. equation 8.7). 8.2 Methodology for Aggregation across Industries We also provide the TFPG for aggregate economy and two broad sectors, viz. manufacturing and services24. However, the method of estimation of TFP growth for individual industries described in section 8.1 cannot be readily applied to a higher level of aggregation. The main problem is that gross value of output cannot be added across industries to generate a measure of output at a higher level of aggregation, say for the economy or of any of the broad sectors. Therefore, it becomes necessary to consider appropriate methods of aggregation across industries consistent with the gross output function specification of technology at the individual industry level. We use the Törnqvist index25 for aggregating across the broad sector and total economy. Taking this approach, computations are made for the manufacturing sector, the services sector, and for the aggregate economy. These aggregates are obtained using Törnqvist aggregate of growth rates of real value added, capital input, and labour input. Below, we briefly describe the Törnqvist index. Suppose the aggregate sector J consists of n KLEMS industries (j=1:n). We obtain the output (vale added) and inputs aggregates for sector J as:  where PV,j is the price of value added in industry j, Vj is the real value added in industry j, PK,j is the rental price of capital in industry j, Sj is the capital stock in industry j, PL,j is the wage rate (price of labour) in industry j, and Hj is the employment in industry j. The aggregate output (real value added) and input growth rates obtained above are then used with the growth accounting equation to obtain the sectoral TFP growth rates. 1 From both aggregated 9 NAS sectors Gross Domestic Product by economic activity statement along with the disaggregated statements of these 9 NAS sectors. 2 In the EUS, the persons employed are classified on the basis of their activity status into usual principal status (UPS), usual principal and subsidiary status (UPSS), current weekly status (CWS) and current daily status (CDS) for quinquennial rounds. UPSS refers to a person’s employment status based on what he/she might have been engaged in over a period of 365 days preceding the date of survey. 3 See Table 7 on pg. no 371 of Economic Survey 2021-22, Government of India (https://www.indiabudget.gov.in/budget2022-23/economicsurvey/doc/echapter.pdf). 4 See Table 8 on pg. 44 on https://main.mohfw.gov.in/sites/default/files/Population%20Projection%20Report%202011-2036%20-%20upload_compressed_0.pdf 5 This is also the mid-point of financial year. 6 For more detailed discussion on extrapolation and interpolation of the series, readers may refer to KLMES data manual version 2022 released by RBI on its website. 7 In PLFS, the earnings by self-employed are also provided, but for consistency with other rounds we have used the same procedure of Mincer equation even for this round. In EU KLEMS (Timmer, et.al., op cit; p 67) it is assumed that the earnings of the self-employed is equal to the earnings of ‘regular' employees. 8 For detailed explanation of Heckman two-step process, one may refer to the previous year manual  10 This version of the database does not make a distinction between ICT and non-ICT assets, as the industry level data on ICT assets are weak. An attempt to estimate aggregate economy level ICT capital can be found in Erumban and Das (2015). 11 See O’ Mahony and Timmer (2009) for a description of EU KLEMS database 12 This data is not publicly available. However, CSO has been kind to compile this data for the India-KLEMS project. 13 In some years transport equipment was provided as part of the machinery and equipment, categorized as ‘tools, transport equipment and other fixed assets. In such cases, we use transport/tools, transport and other fixed asset ratio in the nearest year to separate transport equipment. 14 A detailed discussion on how the series prior to 2011-2012 were adjusted to match the subsequent series is provided in Box 5.2A in the Appendix. 15 Gross investment is estimated as the difference between book value of asset in period t and in period t-1 and add depreciation in period t to that. 16 This choice is driven by the fact that the first year of availability of ASI data is 1964-65. 17 National Accounts Statistics-Sources and Methods, Chapter 26, CSO (2007), 18 We do not intend to delve into the controversies over the use of internal vs. external rate of return in the context of productivity measurement. This database uses See Erumban (2008a and b) for a discussion on these issues. 19 Reserve Bank of India, Handbook of Indian Statistics, Annual volumes. 21 The estimation is done at group level rather than individual industries on the consideration that the group level estimates will be more reliable. 22 Consider, the semi-conductor (SC) industry, which is a key input to the computer hardware industry. Much of the output is invisible at the aggregate level because semi-conductor products are intermediate inputs to other industries rather than deliverables to final demand - consumption and investment goods. Moreover, SC plays a role in the improvements in quality and performance of other products like-computers, communication equipment and scientific instruments. Failure to account for them leads us to miss the role of key industries that produce intermediate inputs and importance of intermediate inputs for the industries that use them. (Jorgenson, Ho and Stiroh (2005), Productivity, volume 3). 23 It should be pointed out that an alternate set of estimates of TFPG obtained by using the value-added function framework is also provided in the India KLEMS dataset for which real gross value added is taken as the measure of output and only the two primary inputs are considered, namely labour input and capital input 24 More sophisticated methods of aggregation, such as the application of production possibility frontier approach or the application of direct aggregation is done in research papers written on the basis of the KLEMS dataset prepared. Such estimates of TFP growth are not a part of the database. 25 There exists other approaches to aggregate across broad sectors and industry, a detailed discussion on them can be found in KLEMS data manual version 2020 released by RBI on its website |

|||||||||||||||||||||||||||||||||||

Estimates of Productivity Growth for the Indian Economy

|

There is a major data gap in terms of availability of a consistent series on productivity for the Indian economy, though many individual researchers have estimated productivity for different sectors and the overall economy for specific time periods using different methodologies. In order to address this data gap, the Reserve Bank had funded a project in the Indian Council for Research on International Economic Relations (ICRIER) on productivity measurement following the EU-KLEMS (Capital, Labour, Energy, Material and Services) methodology. The research work under the project was carried out by a team comprising Dr. Deb Kusum Das, Professor Suresh Aggarwal, Dr. Abdul Azeez Erumban, Ms Sreerupa Sengupta, Ms Kuhelika De and Shri Pilu Chandra Das under the overall guidance of Professor B. N.Goldar. The team was also guided by an Advisory Committee under the chairmanship of Professor K.L.Krishna and with Dr. Isher Ahluwalia, Prof. K.Sundaram, the late Prof. Suresh Tendulkar, Dr. Ramesh Kolli, Prof. T C Anant, Dr. R.Radhakrishna, Prof. Dale Jorgenson, Prof. Marcel Timmer, Dr. Bart Van Ark, Prof. Mary O’Mahony and the undersigned as members. The research team has since submitted three reports delineating the methodology of productivity measurement in the KLEMS framework and estimates of productivity growth along with the time series data for the period 1980-81 to 2008-09. With the objective of making this data and methodology available to the broader community of researchers and analysts, the current Report on “Estimates of Productivity Growth for the Indian Economy” is being released by the Reserve Bank of India. The abridged version of the Report, based on the original three Reports, has been prepared by an internal team of officers led by Smt. Balbir Kaur and comprising Shri Rajib Das, Smt. Sangita Misra, Shri Alok Ghosh, Ms Alice Sebastian and Shri Anoop K. Suresh. The Reserve Bank of India takes this opportunity to thank ICRIER and the research team for this useful endeavour, the Advisory Committee for their guidance and all those, both within the RBI and outside, who have contributed to the project in different ways. It may, however, be emphasised that the data on productivity and related analysis given in this report reflect the research output of the India KLEMS research team and, therefore, do not represent an official series on productivity by the Reserve Bank of India. Given the enormous data challenges and differences in methodology in this area, the researchers may ensure adequate caution in the use of the data. Deepak Mohanty Research Advisor Team Members The Report titled “Estimates of Productivity Growth for Indian Economy” presents the work carried out by the India KLEMS project at ICRIER in collaboration with the Reserve Bank of India. The research project has computed a time series database on productivity growth for the Indian economy and has, thus, tried to fill in an important data gap in this area. Some of the distinguishing features of the project are described below:

Some of the major findings of the Report are outlined below:

As regards labour productivity, the median growth for the economy as a whole was observed to be 4.1 per cent during 1980-2008, with higher growth rates in manufacturing industries, the electricity sector and certain services. When it comes to the growth rates of various inputs, labour input (Index of persons employed multiplied by index of labour composition) grew the fastest in construction and some service industries, while the agriculture sector remained a laggard. The growth rate of capital services in the economy was 6.5 per cent per year. It was the highest at 8.8 per cent in the broad sector of manufacturing and the lowest at 3.5 per cent in the agriculture sector. As regards the trend rates of growth for intermediate inputs, enormous heterogeneity is observed across industries in the range of 12.8 per cent (for post & telecommunication) to 2.3 per cent (for agriculture). The findings of this research project confirm the dominant role of input accumulation vis-à-vis productivity growth in explaining India’s economic growth. Productivity Growth is studied extensively because it is a contributory factor in the improvement of living standards. In recent years, leading researchers in productivity have turned their attention to the measurement and analysis of productivity at the disaggregate industry level that covers the entire economy of selected countries. While much of the earlier research was based on a value added version of the production function, ignoring the explicit role of intermediate inputs in the production process, recent work on productivity for several countries has been based on the Gross Output version of the production function for all individual industries comprising the economies. It is against this backdrop that the KLEMS research project was undertaken in September 2009 with two major objectives:

The KLEMS research project has computed productivity growth estimates through two different approaches: (1) using a value added production function, incorporating labour and capital inputs for the Indian economy and for 26 sectors for the period 1980-2008 and (2) gross output methodology of computing productivity and incorporating primary inputs of capital (K) and labour (L) along with the intermediate inputs of energy (E), materials (M) and services (S). In estimating productivity growth, the quality aspects of two inputs—labour and capital—have been explicitly addressed. Two dimensions of the labour input were distinguished—labour persons and educational attainment of the workforce—so that the contribution of education to value added growth at the individual industry level could be assessed. With regard to capital input, three asset types were distinguished: (i) construction (structures), (ii) transport equipment and (iii) machinery and equipment. Taking into account the differences in the length of life (depreciation) of the three asset types, measures of capital services were derived for each sector/industry. For measurement of capital input for the economy as a whole, ICT capital was also taken into account. Along with the productivity estimates, the project has also generated new datasets on labour, capital and the three intermediate inputs—energy, material and services—for each of the years over the time period that allow greater accuracy in the estimation of productivity growth at the industry level as well as the economy and its broad sectors. The database for the study is prepared for use in the growth accounting methodology for estimating total factor productivity. Growth accounting allows a decomposition of output growth into the contribution of the different inputs and total factor productivity. The period covered is from 1980-81 (1980) to 2008-09 (2008). The industrial classification used for the study is along the lines of EU KLEMS1 so as to ensure comparability with other studies under the KLEMS project, where each economy is divided into 26 industries, as shown in Table 1.1. (In particular, the input-output (IO) tables could be aggregated to only 26 industries.)

The industrial classification was constructed by building concordance between NIC2 2004, NIC 1998, NIC 1987 and NIC 1970 so as to ensure continuous time series from 1980 to 2008. The database for 26 industry disaggregation consists of Agricultural sector (1), Mining and Quarrying sector (1), Manufacturing industries (13), Electricity, Gas and Water supply (1), Construction (1) and Services sector (9) comprising both market and non-market services. Measures of capital (K), labour (L), energy (E), material inputs (M) and service inputs (S) as well as gross output (GO) and value added (VA), were constructed using National Account Statistics (NAS), Annual Survey of Industries (ASI), NSSO rounds and input-output (IO) tables. For certain industries, annual data from NAS and ASI were used to compute time series on gross output. However, NSSO rounds of unregistered manufacturing, Employment and Unemployment Surveys by NSSO and input-output tables are available only for benchmark years. This necessitated interpolation and assumption of constant shares for construction of time series for gross output (unregistered manufacturing, services sector), intermediate inputs and labour inputs. An overview of earlier productivity research in India is attempted in Chapter 2 to provide a background on both issues and methodologies that have been addressed in past studies. The Indian literature on productivity measurement is quite vast. In Chapter 3, the methodology for computing total factor productivity (as well as labour productivity) growth rates at the industry, sector and economy levels is discussed. The chapter outlines three different aggregation procedures for arriving at the economy-level productivity growth rates. The different sources used for the construction of data series and the methodology adopted for the construction of both value added and gross outputs series are explained in Chapter 4. The various sub-sections of Chapter 5 outline the methodology adopted for the construction of labour input, capital input and intermediate inputs—energy (E), material (M) and services (S). The productivity growth estimates derived using the compiled data series on gross value added, gross output, labour, capital, and Intermediate inputs are presented in Chapter 6. Chapter 7 discusses estimates of labour productivity and total factor productivity growth for six broad sectors and the economy. Chapter 8 presents a summary of the findings and conclusions derived from the study. Chapter 2: Overview of Productivity Research in India The Indian literature on productivity measurement is quite vast, and is growing fast. The quality of research has improved steadily over the years. While the bulk of the past productivity research has been on the manufacturing/ industrial sector (Ahluwalia, 1985, 1991; Goldar, 1986, 2004), there have been several studies on productivity growth in agriculture and services, and the economy as a whole. The Indian productivity literature, particularly the studies on manufacturing, has been reviewed by Goldar (2011b), Goldar and Mitra (2002) and Krishna (1987, 2006, 2007), among others. This chapter presents a brief overview. 2.2 Productivity in manufacturing Chronologically, productivity studies on Indian manufacturing can be divided into three groups. The first generation studies, which include the studies undertaken by Reddy and Rao (1962), Banerji (1975), Goldar (1986) and Ahluwalia (1985), came up with estimates of TFP growth that indicate that TFP growth in Indian manufacturing in the period 1951 to 1979 was slow or negative. The second-generation studies drew attention to the biases in productivity estimates arising from the use of value added function and particularly the use of single deflated value added. Two prominent studies belonging to this group are Balakrishnan and Pushpangadan (1994) and Mohan Rao (1996). These studies contested the assertion made by Ahluwalia (1991) that there was a marked acceleration in TFP growth in manufacturing after 1980 which was attributed to liberalisation of economic policies. Ahluwalia had relied on the single‐deflation (SD) procedure. The more appropriate double‐deflation (DD) procedure by Balakrishnan and Pushpangadan resulted in TFPG estimates that contradicted Ahluwalia’s claim. Mohan Rao’s results based on (i) double deflation in the case of value added production function and (ii) gross output production function as well as those of Pradhan and Barik (1998) using the Gross Output function lend support to the contention of Balakrishnan and Pushpangadan that there was no turnaround in productivity growth in manufacturing in the 1980s3. The third-generation studies have mostly focussed on the impact of industry and trade policy reforms on industrial productivity growth in the post‐reform period (i.e., the period since 1991). The third-generation studies have, in most cases, used the gross output function for the measurement of TFP. These studies take services as an input along with capital, labour, materials and energy to estimate total factor productivity growth in Indian manufacturing. The overall conclusion one may draw from the findings of these studies is that there has been no improvement in the rate of TFP growth in Indian manufacturing in the post‐reform period compared to the growth rate achieved in the 1980s. Rather, TFP growth has slowed down. Trivedi et al (2011) for instance report that the TFP growth rate in manufacturing was 1.88 per cent per annum during 1980 to 1991 and 1.05 per cent per annum during 1992 to 2007. As regards the unorganised manufacturing sector, there have been only a couple of productivity studies. Most of them report a downward trend in TFP (Prakash (2004), Unni et al. (2001), Kathuria et al. (2010)). 2.3 Productivity in Agriculture Estimates of TFP growth are available for aggregate agriculture, crop sector, livestock sector and even individual crops such as rice, wheat, maize and sugarcane. Estimates have also been worked out at the state level for major crops. Concerns have been expressed on the basis of available evidence that agricultural growth is becoming unsustainable as a result of resource (soil) degradation. Mukherjee and Kuroda (2003) report that the growth rates in TFP in Indian agriculture were 1.45 per cent per annum during 1973‐80, 2.33 per cent per annum during 1981‐88 and 1.21 per cent per annum during 1989‐93. Between 1973 and 1993, the average rate of growth in TFP was 2.02 per cent per annum. There have been several productivity studies on specific sub‐sectors of services. The Indian Railways, for example, has been studied by Sailaja (1988) and Alivelu (2006). Similarly, productivity in Indian airlines has been studied by Hashim (2003), productivity in the insurance industry by Sinha (2007), and productivity of the information technology industry by Mathur (2007). In comparison with other sub‐sectors of services, a much larger number of studies on productivity and efficiency have been undertaken for banks, e.g., De (2004) and Sinha and Chatterjee (2008). The estimates of TFP growth presented in two studies (Goldar and Mitra 2010; Virmani, 2004) indicate that there was a marked acceleration in TFP growth in services after 1980 (Table 2.1).

2.5 Inter‐Sectoral Perspective Bosworth et al. (2007) present sources of economic growth during 1960‐2004, for the three sectors, namely, agriculture, industry and services, as well as the total economy. Going by their estimates (Table 2.2) the productivity performance of the services sector was the best in the sub‐periods 1960‐80 and 1980‐2004. Overall, the performance was unsatisfactory in all three sectors during the first sub‐period. The estimates of productivity presented in Bosworth and Maertens (2010) show a pattern very similar to that in Bosworth et al., (2007). The growth rate of TFP in services exceeded that in industry and agriculture in the periods 1980‐90, 1990‐2000 and 2000‐2005 (Figure 2.1). The gap in the TFP growth rates between services and other sectors was relatively greater in the period 1990 to 2000. A similar pattern is observed in the estimates of TFP growth in agriculture, industry and services reported by Verma (2008). Figure 2.1: Total factor productivity growth, India, by broad sectors of the economy  2.6 Productivity Studies for the Aggregate Economy Four major recent studies on sources of growth of the Indian economy are by Dholakia (2002), Sivasubramonian (2004), Virmani (2004), and Bosworth, et al. (2007)4. Table 2.3 shows the estimates of TFP growth for the aggregate economy obtained in various studies. The broad conclusion one may draw from the productivity growth estimates presented in the studies is that the rate of TFP growth in the Indian economy accelerated sharply after 1980. Also, there is an indication that the rate of growth in TFP in the post‐reform period has been higher than that achieved in the 1980s. The acceleration in TFP growth at the aggregate economy level seems to be rooted in the improved productivity performance of the services sector.