IST,

IST,

Consumer Confidence Survey

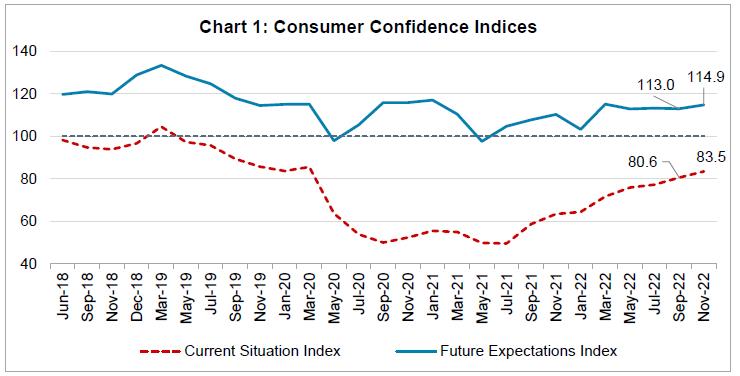

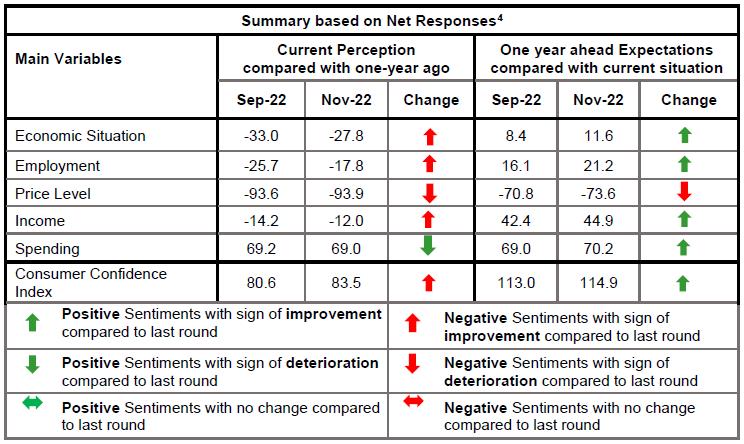

Today, the Reserve Bank released the results of its Consumer Confidence Survey (CCS)1 for the November 2022 round. The survey obtains current perceptions (vis-à-vis a year ago) and one year ahead expectations on general economic situation, employment scenario, overall price situation and own income and spending across 19 major cities. The latest round of the survey was conducted during November 02 to 11, 2022, covering 6,089 responses. Highlights:

Note: Please see the excel file for time series data.3  1 The survey results reflect the respondents’ views, which are not necessarily shared by the Reserve Bank. Results of the previous survey round were released on the Bank’s website on September 30, 2022. 2 CSI and FEI are compiled on the basis of net responses on the economic situation, income, spending, employment and the price level for the current period (as compared with one year ago) and a year ahead, respectively. CSI and FEI = 100 + Average of Net Responses of the above parameters. 3 Unit-level data for previous rounds of the survey are available on the Database on Indian Economy (DBIE) portal of the Bank (web link: https://dbie.rbi.org.in/DBIE/dbie.rbi?site=unitLevelData) 4 ‘Net response’ is the difference between the percentage of respondents reporting optimism and those reporting pessimism. It ranges between -100 and 100. Any value greater than zero indicates expansion/ optimism and values less than zero indicate contraction/ pessimism. |

ఈ పేజీని షేర్ చేయండి:

భారతీయ రిజర్వ్ బ్యాంక్ మొబైల్ అప్లికేషన్ను ఇన్స్టాల్ చేయండి మరియు తాజా వార్తలకు త్వరిత యాక్సెస్ పొందండి!

మా యాప్ను ఇన్స్టాల్ చేయడానికి QR కోడ్ను స్కాన్ చేయండి

పేజీ చివరిగా అప్డేట్ చేయబడిన తేదీ: