IST,

IST,

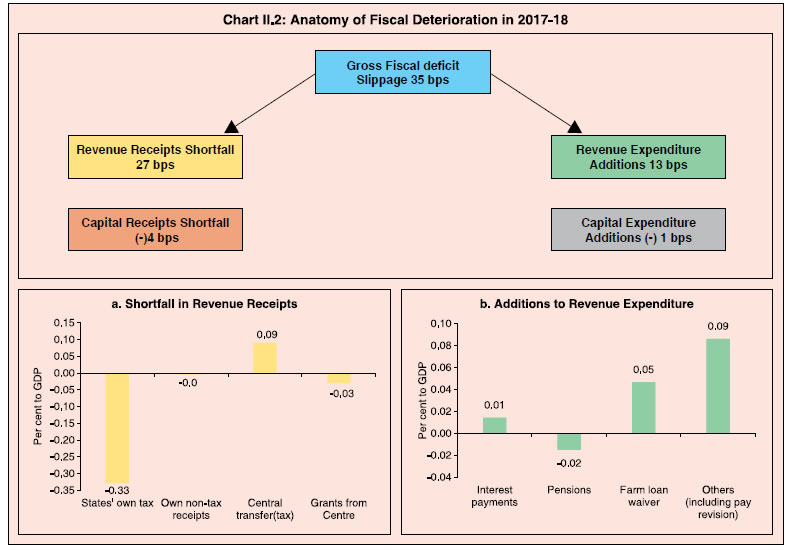

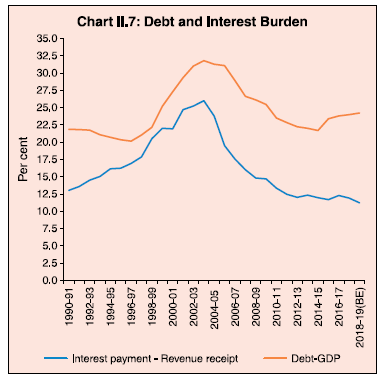

II. Fiscal Position of State Governments

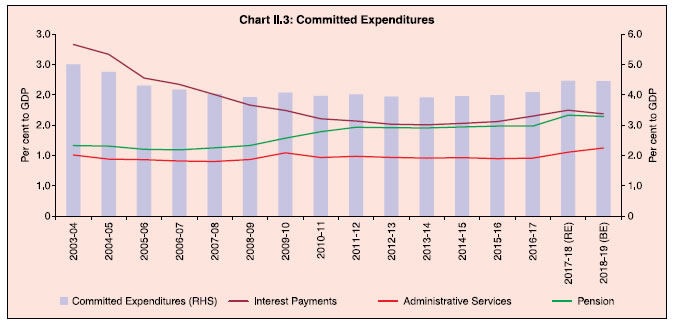

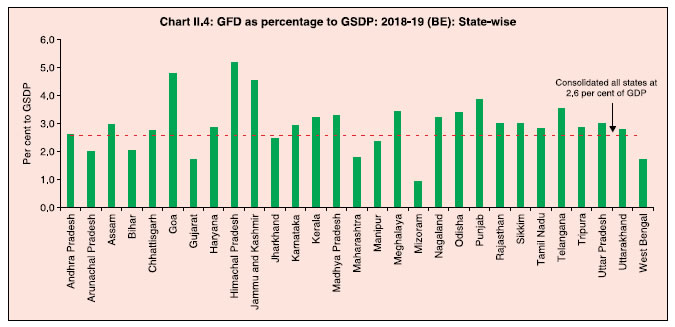

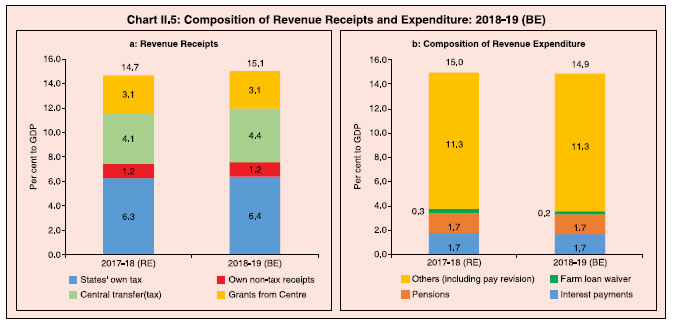

The consolidated fiscal position of states deteriorated during 2015-16 and 2016-17 to cross the Fiscal Responsibility and Budget Management (FRBM) threshold due to the Ujwal Discom Assurance Yojana (UDAY) scheme. While state finances were budgeted to improve in 2017-18, revised estimates suggest a deterioration of 35 basis points in gross fiscal deficit to gross domestic product (GFD-GDP) ratio, essentially on the revenue account. Outstanding liabilities of states continued their double digit growth with a rising share of market borrowings in 2017-18. For 2018-19, states have budgeted for a revenue surplus and GFD-GDP ratio of 2.6 per cent. Revenue mobilisation remains the key towards attaining the budgeted targets. 1. Introduction 2.1 Against the backdrop of heightened pressure on budgets in 2015-16 and 2016-17 from the Ujwal Discom Assurance Yojana (UDAY), states targeted to lower the gross fiscal deficit to 2.7 per cent of GDP in 2017-18, hoping to undershoot the 3.0 per cent norm2 (Table II.1). The revised estimates (RE) for 2017-18, however, reveal a GFD-GDP ratio of 3.1 percent, thus, crossing the Fiscal Responsibility and Budget Management (FRBM) threshold for the third consecutive year. The consolidated fiscal deficit of states is budgeted at 2.6 per cent of GDP in 2018-19 to be achieved through higher revenue collection and lower revenue expenditure. 2.2 This Chapter analyses the underlying dynamics of the RE for 2017-18 and proposals for 2018-19 against the backdrop of the actual outcomes for two years of 2015-16 and 2016-17, which are examined in section 2. In section 3, an attempt is made to drill down into variations between budgeted and revised estimates for 2017-18, while in section 4, the endeavour is to unravel the budget estimates (BE) for 2018-19. Analysis of outstanding liabilities of states covering composition, liquidity position and cash management are undertaken in section 5. Concluding observations are presented in section 6. 2. Accounts: 2015-16 and 2016-17 2.3 At the aggregate level, both fiscal and primary deficits of states continued to deteriorate in 2015-16 and 2016-17 as in the preceding two years (Chart II.1). 2.4 The gross fiscal deficit remained higher than the 3.0 per cent norm during both these years (Table II.1), largely due to UDAY (an impact of 0.7 per cent of GDP each year). The revenue deficit, which had shrunk substantially in 2015-16 from its level a year ago, worsened in 2016-17. 2.5 The deterioration of the gross fiscal deficit and the primary deficit was located primarily among non-special category (NSC) states3. While special category (SC) states improved their financial position in 2015-16, they suffered a deterioration in 2016-17 (Table II.2). With regard to the revenue deficit, SC states posted a surplus, but NSC states’ deficit expanded in 2016-17. 2.6 On the receipts side, states continued to garner support of central transfers, particularly shareable taxes4, while own tax revenues and transfers through grants moderated (Table II.3). On the expenditure side, non-developmental expenditure was flat as a proportion to GDP at around 4.6 per cent; in contrast, development expenditure continued to increase (Table II.4). Both revenue and capital expenditure increased, the latter outpacing the former on account of higher loans and advances extended to power projects under UDAY and higher capital outlay on energy, major and medium irrigation, rural development, roads and bridges. 2.7 The increase in revenue expenditure was largely reflected in items such as expenditure on natural calamities due to floods in various parts of India (West Bengal, Assam, Chennai, Rajasthan, and Gujarat), the effects of the Nepal earthquake on some parts of Bihar and UP, as well as expenditure on social security and welfare, energy, interest payment on market loans and urban development. 2.8 The consolidated finances of 29 state governments point towards a deterioration in the key deficit indicators in the RE for 2017-18 vis-à-vis the BE (Table II.1). The erosion occurred despite the discontinuation of the UDAY scheme. A slippage of 0.40 percentage points of GDP in the consolidated revenue deficit and 0.35 percentage points of GDP in the GFD occurred on account of overshooting of revenue expenditure by 13 basis points (bps), mainly due to farm loan waivers and pay revisions, exacerbated by a shortfall of revenue receipts by 27 bps mainly due to states’ own taxes declining by 0.33 per cent of GDP vis-a-vis the BE. The decline in states’ tax revenues is essentially associated with the pending accounting issues related to GST implementation. However, strict comparison with previous years is not possible due to lack of data. Also being the first year of implementation, states have not provided data on uniform basis. While most of the states have shown revenue under State GST (SGST), not all have shown revenue under the head Integrated GST (IGST) and Central GST (CGST). Very few states have explicitly shown the GST compensation cess from centre. In such a scenario, the true picture on own tax revenues due to GST will get clearer next year in the Accounts data for 2017-18. This shortfall in own tax revenues was partly offset by transfers from the Centre, which exceeded budget projections by 0.09 per cent of GDP. By contrast, the capital account helped to contain the slippage, with capital receipts up by 4 bps and capital expenditure down by 1 basis point relative to BE (Chart II.2). 2.9 While 12 out of 29 states had budgeted fiscal deficits above the 3 per cent norm in 2017-18 (BE), the RE revealed that as many as 19 exceeded the norm. In fact the year 2017-18 saw a change from the previous few years with all deficit indicators worsening for SC states than that of NSC states and most SC states recording GFDs above the 3 per cent mark (Table II.5). 2.10 Comparing the 2017-18 (RE) with 2016-17 (accounts), it is observed that while the consolidated states’ GFD at 3.1 per cent of GDP marks some consolidation over 3.5 per cent recorded in 2016-17, there was a deterioration in the revenue balance as revenue spending outpaced receipts and revenue deficit saw a more than 50 per cent growth (Table II.5 and II.6). 2.11 Expenditure on the revenue account surged in 2017-18, on both development and non-development heads. Higher spending on sectors such as housing, medical and public health and crop husbandry were the major propellers of development expenditure. Non-development expenditure was pushed up by committed expenditures – pension payments; spending on administrative services, essentially led by pay commission recommendations; and interest payments driven up by rising market borrowings as well as yields (Chart II.3). 2.12 While capital expenditure stagnated in 2017-18 (RE), capital outlay showed an impressive growth of 20 per cent over 2016-17 in respect of irrigation, flood control and transport, but declined for energy sub-sectors. The decline in overall capex reflects the termination of UDAY scheme. Capital receipts also declined due to repayment of loans and advances (Table II.6). 2.13 For 2018-19, states have budgeted for a consolidated GFD of 2.6 per cent of GDP, with 11 states planning to remain above the 3 per cent threshold (Chart II.4). Consolidation is mainly expected to accrue from the revenue balance, which is expected to post a surplus of 0.2 per cent of GDP in 2018-19 (BE) as against a deficit of 0.4 per cent in 2017-18 (RE) (Chart II.1). Capital outlay is envisaged to account for more than 100 per cent of the fiscal deficit, indicative of the inclination to bring about improvement in the quality of the deficit (Table II.7). States have also projected an increase in their reliance on market borrowings to about 91 per cent of GFD, in line with the recommendation of the fourteenth Finance Commission (FC-XIV). Revenue Receipts 2.14 Revenue receipts are expected to go up on account of central transfers and states’ own taxes comprising states’ GST and other commodity taxes (Table II.3 and Chart II.5). 2.15 Notwithstanding some uncertainty in revenues in 2017-18 associated with the GST implementation, state-wise analysis suggests better prospects going forward (Box II.1).

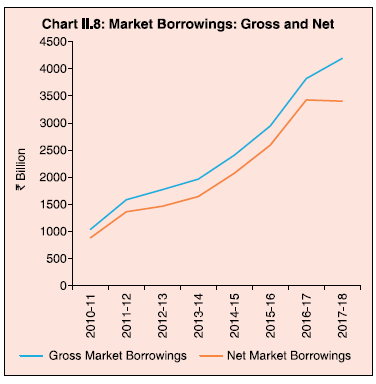

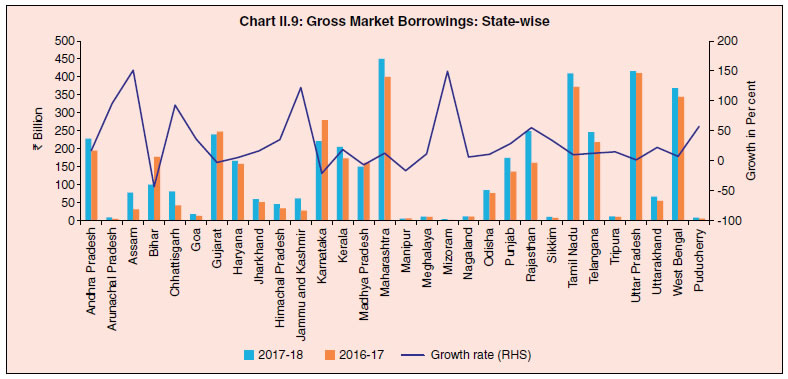

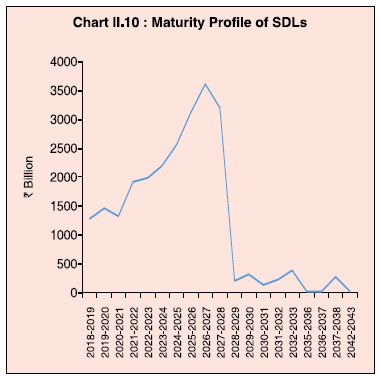

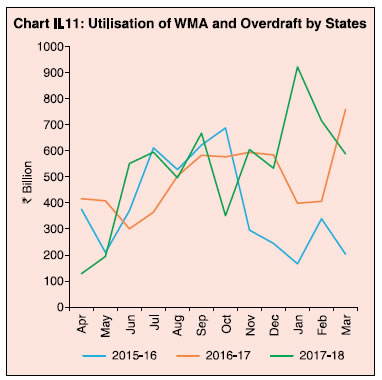

Expenditure Pattern 2.16 Surplus in the revenue account is budgeted to accrue on account of a lower increase in revenue expenditure in 2018-19 vis-a-vis 2017-18 (RE) with regard to farm loan waivers (Chart II.5). Non-development expenditure is estimated to rise in 2018-19, backed by committed expenditure on administrative services. Development expenditure, however, has been projected to moderate/decline in some sectors - rural development and relief on account of natural calamities - while higher allocations have been made for education, sports, art and culture (Table II.6). 2.17 Capital outlay is expected to grow slower at about 14 per cent in 2018-19 as against the growth of 20 per cent a year ago. Spending on energy sub-sector has been programmed to decline, while higher allocations have been made for the ‘medium and major irrigation and flood control’ subsectors. 2.18 Social sector expenditure (SSE)5 has a strong link with overall economic development, particularly in the medium to long term. SSE is budgeted to increase in 2018-19 as a proportion to aggregate expenditure over 2017-18 (RE) (Chart II.6). As a proportion to states’ respective GSDP, twelve states have budgeted to increase SSE (Statement 35 for 2018-19). 2.19 The composition of expenditure on social services points toward a shift in expenditure from education and health to other types of expenditure such as water supply and sanitation, housing and urban development, though the former accounts for around 55 per cent of total social service spending (Table II.8). Recent initiatives such as the Swachh Bharat Mission, affordable housing schemes and the smart cities mission appear to be the major drivers of this shift. 5. Outstanding Liabilities of State Governments 2.20 Outstanding liabilities of states have been growing at double digits, barring in 2014-15 (Table II.9). The issuance of UDAY bonds in 2015-16 and 2016-17, farm loan waivers and the implementation of pay commission awards led to higher debt- GDP ratio at 24.0 per cent in 2017-18 (RE) which is expected to rise to 24.3 per cent in 2018-19 (BE). State-wise data reveal that the debt-GSDP ratio increased in 2018-19 for 16 states (Statement 20). 2.21 Despite the rising path of states’ indebtedness, their interest payment to revenue receipts (IP-RR) ratio has remained unchanged on account of revenue receipts compensating for the increase in interest payments (Chart II.7). Composition of Debt6 2.22 Of this outstanding debt, market borrowings constituted 76.2 per cent at end- March 2018 and is projected to increase to 77.0 per cent at end-March 2019 (Table II.10). Within this rising debt profile, loans from banks and financial institutions stagnated at around 4 per cent and the share of the National Small Savings Fund (NSSF) continued to decline. Similarly, loans from the centre and public accounts items are also declining gradually and getting replaced by market loans. 2.23 During 2017-18, upside risks to inflation, fiscal slippages, farm loan waivers and global factors such as increasing crude oil prices and monetary policy normalisation by the US were the major factors impacting the yields on state development loans (SDLs)7. 2.24 Pursuant to the recommendation of the FC-XIV, states (barring Delhi, Madhya Pradesh, Kerala and Arunachal Pradesh) have been excluded from the National Small Savings Fund (NSSF) financing facility from 2016-17. The consequent increase in their market borrowings has imposed large redemption pressures, exacerbating the debt management burden. The share of market borrowings in financing GFD has increased from 61.4 per cent in 2015-16 to 74.9 per cent in 2017-18 (RE) and is projected to rise further to 90.6 per cent in 2018-19 (BE) (Table II.7) mainly due to the termination of the NSSF financing facility. 2.25 The number of issuances of state development loans (SDL) has almost doubled between 2012-13 and 2017-18 even as average issue size has gone up (Table II.11). 2.26 The wedge in the net and gross market borrowings indicates the increasing redemption pressure, which is likely to persist (Chart II.8). Post global financial crisis (GFC), the market borrowing of states increased mainly due to the additional fiscal space given to states as part of stimulus measures. Since states normally issue plain vanilla bonds with the maturity of 10 years, the redemption pressures increased from 2017-18, implying that the borrowings of states are expected to soar. There was no UDAY issuance during the year 2017-18. 2.27 Among the NSC states, Maharashtra (10.7 per cent), Uttar Pradesh (9.9 per cent), Tamil Nadu (9.7 per cent) and West Bengal (8.8 per cent) had the largest shares in market borrowings during 2017-18. Among the SC states, Assam (1.9 per cent), Himachal Pradesh (1.1 per cent), Jammu and Kashmir (1.5 per cent) and Uttarakhand (1.6 per cent) were the major borrowers (Chart II.9). The growth of gross market borrowing of SC states at 58.9 per cent during 2017-18 outstripped that of NSC states by a wide margin (7.0 per cent). Maturity Profile of State Government Securities 2.28 The maturity profile of states’ debt indicates near to medium-term redemption pressures, which is likely to rise continuing from current year and reach a peak in 2026-27 (Chart II.10). 2.29 At end March 2018, 67.2 per cent of the outstanding SDLs were in the residual maturity bucket of five years and above (Table II.12). About 16.7 per cent of outstanding SDLs will mature in the next three years, keeping redemption pressure high in the near future. 2.30 During 2017-18, 9 states and the Union Territory of Puducherry issued non-standard securities with a maximum maturity of 25 years. Pursuing the strategy of passive consolidation, states like Maharashtra, Tamil Nadu and Odisha undertook reissuances during 2017-18, thereby creating critical mass to enable trading of securities in the secondary market. Liquidity Position and Cash Management 2.31 Several states have been accumulating sizeable cash surpluses in recent years, involving a negative carry8 on interest rates. As on March 31, 2018 states’ outstanding intermediate treasury bills (ITBs)9 stood at ₹1,508.7 billion and the stock of auction treasury bills (ATBs)10 was placed at ₹621 billion. States’ availment of ways and means advances (WMA) and overdrafts (ODs) rose in 2017-18 in comparison to the preceding year (Chart II.11). This increase was mainly due to heavy dependence on this facility by certain states due to state specific reasons. 2.32 To sum up, states’ fiscal position deteriorated during 2015-16 and 2016-17 due to the states taking over of Discom debt under UDAY schemes. Consequently, their consolidated fiscal deficit rose above the FRBM threshold level. As per the revised estimates, GFD-GDP ratio continued to remain above the FRBM threshold during 2017-18 due to shortfall in revenue receipts and higher revenue expenditure from implementation of farm loan waivers and the pay commission recommendations on salaries and pensions. 2.33 States have budgeted for a revenue surplus in 2018-19 and a lower fiscal deficit. Going forward, fiscal risk may emanate for many states going for election during the year, continuing announcements and rollouts of farm loan waivers as well as the implementation of the pay commission awards by some states. If the likely slippage is reflected in higher borrowing requirements for 2018-19, there could be a concomitant impact on borrowing costs. Revenue mobilisation remains the key towards attaining the budgeted targets. As the GST stabilises, it should boost states’ revenue capacity and support the resumption of fiscal consolidation. The cushion provided by compensation cess by the Centre for any interim shortfall may help smooth state finances from the revenue front. Nevertheless, better fiscal marksmanship and efficiency of expenditures appear essential to providing robustness to state finances if revenue receipts end up again in shortfall relative to budgeted levels. 1 The analysis of various fiscal indicators is in proportion to GDP, unless stated otherwise. Moreover, the analysis pertains to Final Accounts for 2015-16 and 2016-17, Revised Estimates (RE) for 2017-18 and Budget Estimates (BE) for 2018-19. 2 The threshold of 3 per cent GFD-GSDP ratio was first recommended by the Twelfth Finance Commission (FC-XII) and later endorsed by both the Thirteenth Finance Commission (FC-XIII) as well as the Fourteenth Finance Commission (FC-XIV). It has also been acknowledged by state governments in their respective Fiscal Responsibility and Budget Management (FRBM) Acts. 3 Of the 29 states, there are 11 special category (SC) states and 18 non-special category (NSC) states. The SC states include Arunachal Pradesh, Assam, Himachal Pradesh, Jammu and Kashmir, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura and Uttarakhand while NSC states are Andhra Pradesh, Bihar, Chhattisgarh, Goa, Gujarat, Haryana, Jharkhand, Karnataka, Kerala, Madhya Pradesh, Maharashtra, Odisha, Punjab, Rajasthan, Tamil Nadu, Telangana, Uttar Pradesh and West Bengal. 4 The Union Government accepted the recommendations of FC-XIV to increase states’ share in the divisible pool of taxes to 42 per cent (earlier 32 per cent) from 2015-16 onwards. It altered the composition of central transfers in favour of statutory transfers from discretionary transfers made earlier. It also led to greater predictability and certainty in the quantum of funds being transferred to states; additionally, there would be an overall increase in untied funds. 5 Includes expenditure on social services, rural development, food storage, and warehousing. 6 The Reserve Bank manages the domestic debt of 29 state governments and the Union Territory of Puducherry in accordance with bilateral agreements, as provided in Section 21A of the RBI Act. 7 Detailed analysis on SDL spreads is given in Chapter III. 8 Negative carry prevails in the form of the interest rate difference between the market borrowings (SDLs) by states at a higher rate and the returns from their surplus cash investments in intermediate treasury bills (ITBs)/auction treasury bills (ATBs). Currently, the discount rate of ITBs is 200 bps below the reverse repo rate with the maximum ceiling of 5 per cent and ATBs investments by states carry returns at the market clearing cut-off yield allocated through the non-competitive route of the auction process. 9 ITBs are the bills issued to enable the State Government and the Foreign Central Bank to park their surplus cash balances. These bills are of 14 day maturity and are issued with discount. In terms of the Government of India notification dated January 30, 2017, the discount rate of 14 day ITBs has been revised to the Reverse repo rate minus 200 basis points subject to an upper ceiling of 5 per cent. 10 Auction Treasury Bills are debt instruments issued by Government of India (GOI) to meet the short term liquidity needs of the Government to bridge the gap between revenue and expenditure. Currently, the GoI issues 91-days, 182-days and 364-days Treasury Bills. |

इस पेज को शेयर करें:

आरबीआई मोबाइल एप्लीकेशन इंस्टॉल करें और लेटेस्ट न्यूज़ का तुरंत एक्सेस पाएं!

हमारा ऐप इंस्टॉल करने के लिए QR कोड स्कैन करें

पृष्ठ अंतिम बार अपडेट किया गया: