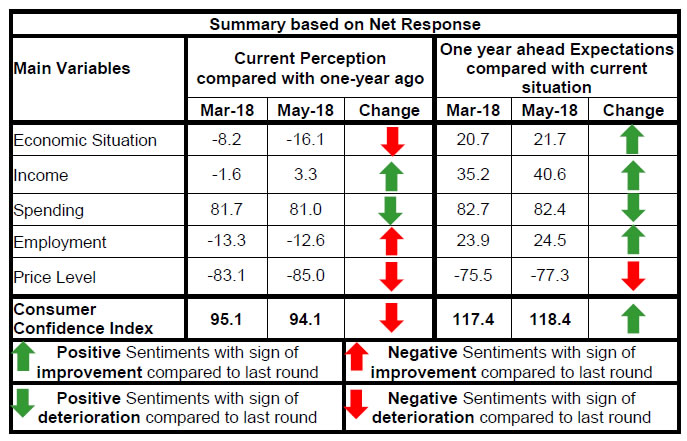

आज, रिजर्व बैंक ने मई 2018 चक्र के उपभोक्ता विश्वास सर्वेक्षण (CCS)1 के परिणाम जारी किए। ये सर्वेक्षण 6 मेट्रोपॉलिटन शहरों – बेंगलुरु, चेन्नई, हैदराबाद, कोलकाता, मुंबई और नई दिल्ली - में आयोजित किए गए थे; तथा इसमें सामान्य आर्थिक स्थिति, रोजगार परिदृश्य, समग्र मूल्य स्थिति और पारिवारिक आय और व्यय के संबंध में 5,077 पारिवारिक इकाइयों की धारणाओं और अपेक्षाओं के लिए प्रतिक्रियाएं प्राप्त की गईं। विशेष: I. मई 2018 में उपभोक्ता विश्वास मार्च 2018 के स्तर के लगभग बराबर रहा; यद्यपि निराशावादी क्षेत्र में मौजूदा स्थिति सूचकांक (CSI)2 एक बिंदु से नीचे गिरा, भविष्य की प्रत्याशाओं के सूचकांक (FEI) में मामूली वृद्धि दिखी (चार्ट 1)। नोट: कृपया टाइम सिरीज़ डेटा के लिए एक्सेल फ़ाइल देखें। II. मौजूदा अवधि के लिए सामान्य आर्थिक स्थिति पर पारिवारिक इकाइयों की धारणाएँ पिछले चक्र के मुक़ाबले बदतर हुई है क्योंकि 48 प्रतिशत उत्तरदाताओं का मानना था कि स्थिति पिछले एक वर्ष में अधिक खराब हुई है; हालांकि, आगामी वर्ष की प्रत्याशाओं में उनके पिछले चक्र के स्तर की तुलना में सुधार दिखा है (तालिका 1)। III. यद्यपि पारिवारिक इकाइयाँ रोजगार की वर्तमान स्थिति के बारे में निराशावादी रहे, भविष्य के लिए उनकी प्रत्याशाएँ मामूली रूप से बेहतर थीं (तालिका 2)। IV. कीमतें परिवारों के लिए चिंता का विषय बनी रहीं, और अगले वर्ष के लिए उनके दृष्टिकोण काफी हद तक अपरिवर्तित थे। (तालिका 3 और 4)। V. उत्तरदाताओं की धारणाएं उनकी वर्तमान आय के संबंध में लगभग 5 प्रतिशत अंक के सुधार के साथ सकारात्मक हुईं, और अगले एक वर्ष के लिए उनके दृष्टिकोण में भी इसी तरह का सुधार हुआ (तालिका 5)। VI. अगले एक साल में अपने खर्च में वृद्धि की उम्मीद रखने वाले परिवारों का अनुपात पिछले दौर से लगभग अपरिवर्तित रहा (तालिका 6)। VII. गैर-आवश्यक (या विवेकाधीन) वस्तुओं पर खर्च के संबंध में परिवारों की प्रतिक्रियाएँ व्यय के समान या निम्न स्तर की ओर स्थानांतरित हुईं, संभवतया ये कीमतों पर धारणा और दृष्टिकोण पर निराशा को दर्शाता है (तालिका 8)। | Table 1: Perceptions and Expectations on General Economic Situation | | (Percentage responses) | | Survey Round | Current Perception | One year ahead Expectation | | Improved | Remained Same | Worsened | Net Response | Will Improve | Will Remain Same | Will Worsen | Net Response | | Dec-16 | 45.7 | 24.1 | 30.3 | 15.4 | 66.3 | 16.6 | 17.1 | 49.2 | | Mar-17 | 35.6 | 24.4 | 40.0 | -4.5 | 52.1 | 21.4 | 26.5 | 25.6 | | May-17 | 36.4 | 25.9 | 37.7 | -1.3 | 52.4 | 23.5 | 24.1 | 28.3 | | Jun-17 | 32.4 | 27.7 | 39.9 | -7.5 | 48.6 | 25.9 | 25.5 | 23.1 | | Sep-17 | 34.6 | 24.7 | 40.7 | -6.2 | 50.8 | 22.8 | 26.3 | 24.5 | | Nov-17 | 28.9 | 23.3 | 47.9 | -18.9 | 45.2 | 24.1 | 30.6 | 14.6 | | Dec-17 | 36.8 | 25.8 | 37.4 | -0.6 | 54.4 | 22.7 | 22.9 | 31.5 | | Mar-18 | 33.7 | 24.5 | 41.8 | -8.2 | 48.3 | 24.0 | 27.6 | 20.7 | | May-18 | 31.9 | 20.1 | 48.0 | -16.1 | 49.5 | 22.7 | 27.8 | 21.7 |

| Table 2: Perceptions and Expectations on Employment | | (Percentage responses) | | Survey Round | Current Perception | One year ahead Expectation | | Improved | Remained Same | Worsened | Net Response | Will Improve | Will Remain Same | Will Worsen | Net Response | | Dec-16 | 31.0 | 29.8 | 39.2 | -8.3 | 57.3 | 24.1 | 18.6 | 38.7 | | Mar-17 | 32.6 | 28.4 | 39.0 | -6.4 | 52.8 | 24.5 | 22.7 | 30.1 | | May-17 | 32.5 | 28.3 | 39.2 | -6.8 | 52.7 | 26.7 | 20.7 | 32.0 | | Jun-17 | 30.8 | 30.3 | 38.9 | -8.1 | 49.6 | 29.3 | 21.2 | 28.4 | | Sep-17 | 30.1 | 26.3 | 43.7 | -13.6 | 49.9 | 24.0 | 26.1 | 23.8 | | Nov-17 | 27.5 | 25.7 | 46.8 | -19.2 | 45.1 | 27.5 | 27.4 | 17.8 | | Dec-17 | 30.3 | 28.4 | 41.3 | -11.0 | 53.1 | 25.9 | 21.1 | 32.0 | | Mar-18 | 29.9 | 26.9 | 43.2 | -13.3 | 49.5 | 25.0 | 25.5 | 23.9 | | May-18 | 31.5 | 24.4 | 44.1 | -12.6 | 49.5 | 25.5 | 25.0 | 24.5 |

| Table 3: Perceptions and Expectations on Price Level | | (Percentage responses) | | Survey Round | Current Perception | One year ahead Expectation | | Increased | Remained Same | Decreased | Net Response | Will Increase | Will Remain Same | Will Decrease | Net Response | | Dec-16 | 73.9 | 18.3 | 7.7 | -66.2 | 69.5 | 16.0 | 14.5 | -55.0 | | Mar-17 | 85.8 | 9.1 | 5.1 | -80.7 | 81.0 | 10.4 | 8.6 | -72.4 | | May-17 | 83.3 | 11.3 | 5.4 | -78.0 | 79.7 | 11.5 | 8.8 | -70.9 | | Jun-17 | 85.2 | 11.4 | 3.4 | -81.8 | 76.1 | 13.8 | 10.1 | -66.0 | | Sep-17 | 87.7 | 8.7 | 3.6 | -84.1 | 81.0 | 12.5 | 6.5 | -74.5 | | Nov-17 | 89.9 | 7.1 | 3.0 | -86.9 | 82.9 | 10.4 | 6.7 | -76.2 | | Dec-17 | 89.9 | 7.1 | 3.0 | -86.9 | 80.1 | 12.4 | 7.5 | -72.6 | | Mar-18 | 86.7 | 9.8 | 3.6 | -83.1 | 82.1 | 11.4 | 6.6 | -75.5 | | May-18 | 88.2 | 8.6 | 3.2 | -85.0 | 83.1 | 11.1 | 5.9 | -77.3 |

| Table 4: Perceptions and Expectations on Rate of Change in Price Level (Inflation)* | | (Percentage responses) | | Survey Round | Current Perception | One year ahead Expectation | | Increased | Remained Same | Decreased | Net Response | Will Increase | Will Remain Same | Will Decrease | Net Response | | Dec-16 | 57.8 | 18.0 | 24.2 | -33.5 | 62.4 | 17.1 | 20.6 | -41.8 | | Mar-17 | 80.5 | 12.5 | 7.0 | -73.5 | 79.9 | 13.8 | 6.3 | -73.6 | | May-17 | 82.0 | 10.0 | 8.0 | -74.0 | 82.6 | 10.9 | 6.5 | -76.1 | | Jun-17 | 79.9 | 11.5 | 8.5 | -71.4 | 78.7 | 13.5 | 7.9 | -70.8 | | Sep-17 | 80.6 | 10.4 | 9.0 | -71.5 | 78.6 | 14.1 | 7.2 | -71.4 | | Nov-17 | 82.9 | 9.0 | 8.1 | -74.8 | 80.4 | 12.1 | 7.5 | -72.9 | | Dec-17 | 80.4 | 12.8 | 6.8 | -73.6 | 76.9 | 17.0 | 6.1 | -70.8 | | Mar-18 | 79.9 | 13.2 | 6.9 | -73.0 | 80.2 | 13.4 | 6.4 | -73.8 | | May-18 | 79.2 | 13.5 | 7.3 | -71.9 | 78.0 | 16.5 | 5.5 | -72.5 | | *Applicable only for those respondents who felt price has increased/price will increase. |

| Table 5: Perceptions and Expectations on Income | | (Percentage responses) | | Survey Round | Current Perception | One year ahead Expectation | | Increased | Remained Same | Decreased | Net Response | Will Increase | Will Remain Same | Will Decrease | Net Response | | Dec-16 | 27.1 | 47.1 | 25.8 | 1.3 | 54.8 | 33.5 | 11.7 | 43.1 | | Mar-17 | 27.7 | 47.3 | 25.0 | 2.7 | 51.8 | 36.5 | 11.7 | 40.1 | | May-17 | 28.2 | 48.0 | 23.8 | 4.4 | 52.8 | 38.1 | 9.1 | 43.6 | | Jun-17 | 23.8 | 53.8 | 22.4 | 1.4 | 47.1 | 43.5 | 9.4 | 37.7 | | Sep-17 | 26.6 | 46.8 | 26.6 | -0.1 | 48.5 | 39.0 | 12.5 | 36.1 | | Nov-17 | 24.4 | 47.6 | 28.0 | -3.6 | 45.6 | 41.8 | 12.6 | 33.0 | | Dec-17 | 25.2 | 50.7 | 24.1 | 1.1 | 50.7 | 39.1 | 10.3 | 40.5 | | Mar-18 | 23.5 | 51.5 | 25.1 | -1.6 | 46.9 | 41.3 | 11.7 | 35.2 | | May-18 | 27.2 | 48.9 | 23.9 | 3.3 | 50.8 | 38.9 | 10.3 | 40.6 |

| Table 6: Perceptions and Expectations on Spending | | (Percentage responses) | | Survey Round | Current Perception | One year ahead Expectation | | Increased | Remained Same | Decreased | Net Response | Will Increase | Will Remain Same | Will Decrease | Net Response | | Dec-16 | 73.5 | 20.8 | 5.6 | 67.9 | 78.3 | 15.8 | 5.9 | 72.4 | | Mar-17 | 84.4 | 13.4 | 2.1 | 82.3 | 88.5 | 8.3 | 3.1 | 85.4 | | May-17 | 83.4 | 14.9 | 1.6 | 81.8 | 86.0 | 11.9 | 2.0 | 84.0 | | Jun-17 | 81.3 | 17.2 | 1.5 | 79.8 | 83.5 | 13.7 | 2.8 | 80.7 | | Sep-17 | 83.2 | 15.0 | 1.8 | 81.5 | 85.8 | 12.3 | 2.0 | 83.8 | | Nov-17 | 85.6 | 13.1 | 1.3 | 84.2 | 86.8 | 11.0 | 2.3 | 84.6 | | Dec-17 | 83.9 | 14.3 | 1.8 | 82.1 | 84.7 | 12.5 | 2.9 | 81.8 | | Mar-18 | 83.5 | 14.7 | 1.8 | 81.7 | 85.0 | 12.6 | 2.4 | 82.7 | | May-18 | 83.2 | 14.5 | 2.3 | 81.0 | 84.8 | 12.8 | 2.4 | 82.4 |

| Table 7: Perceptions and Expectations on Spending- Essential Items | | (Percentage responses) | | Survey Round | Current Perception | One year ahead Expectation | | Increased | Remained Same | Decreased | Net Response | Will Increase | Will Remain Same | Will Decrease | Net Response | | Dec-16 | 76.9 | 18.4 | 4.7 | 72.2 | 77.5 | 14.9 | 7.7 | 69.8 | | Mar-17 | 85.8 | 11.1 | 3.1 | 82.7 | 87.0 | 9.2 | 3.8 | 83.2 | | May-17 | 85.7 | 11.6 | 2.8 | 82.9 | 86.9 | 9.6 | 3.5 | 83.4 | | Jun-17 | 82.2 | 15.3 | 2.5 | 79.7 | 81.9 | 13.5 | 4.6 | 77.2 | | Sep-17 | 85.0 | 12.6 | 2.4 | 82.6 | 86.1 | 10.9 | 3.0 | 83.1 | | Nov-17 | 86.8 | 11.3 | 1.9 | 85.0 | 86.2 | 10.7 | 3.2 | 83.0 | | Dec-17 | 85.2 | 13.0 | 1.8 | 83.4 | 85.2 | 10.9 | 4.0 | 81.2 | | Mar-18 | 83.9 | 13.8 | 2.3 | 81.5 | 84.8 | 12.3 | 3.0 | 81.8 | | May-18 | 85.0 | 12.4 | 2.7 | 82.3 | 84.8 | 11.7 | 3.5 | 81.3 |

| Table 8: Perceptions and Expectations on Spending- Non-Essential Items | | (Percentage responses) | | Survey Round | Current Perception | One year ahead Expectation | | Increased | Remained Same | Decreased | Net Response | Will Increase | Will Remain Same | Will Decrease | Net Response | | Dec-16 | 37.3 | 44.7 | 18.1 | 19.2 | 49.6 | 35.8 | 14.7 | 34.9 | | Mar-17 | 48.9 | 36.4 | 14.7 | 34.2 | 57.8 | 30.3 | 11.8 | 46.0 | | May-17 | 51.9 | 34.6 | 13.5 | 38.3 | 59.9 | 31.1 | 9.0 | 50.9 | | Jun-17 | 51.6 | 35.5 | 13.0 | 38.6 | 56.3 | 32.6 | 11.1 | 45.2 | | Sep-17 | 54.0 | 34.4 | 11.7 | 42.4 | 60.2 | 30.6 | 9.2 | 50.9 | | Nov-17 | 56.5 | 32.5 | 11.0 | 45.5 | 60.6 | 31.1 | 8.3 | 52.3 | | Dec-17 | 51.1 | 36.6 | 12.3 | 38.8 | 57.3 | 33.6 | 9.1 | 48.2 | | Mar-18 | 54.5 | 32.5 | 12.9 | 41.6 | 61.2 | 29.4 | 9.4 | 51.8 | | May-18 | 52.1 | 32.9 | 15.1 | 37.0 | 57.3 | 32.8 | 9.9 | 47.4 |

|  IST,

IST,