IST,

IST,

Master Circular - Collection of Direct Taxes- OLTAS

|

RBI/2008-2009/81 July 1, 2008 To All Agency Banks Dear Sir, Master Circular – Collection of Direct Taxes- OLTAS Please refer to our master circular RBI/2007/66 dated July 02, 2007 on the above subject which was issued with a view to facilitating quick reference to all the extant instructions issued on the subject at one place. We have now updated the master circular incorporating important instructions issued by us till end June, 2008. A copy of the same is enclosed for your information. This circular may also be downloaded from our website /en/web/rbi/notifications/master-circulars 2. Please acknowledge receipt. Yours faithfully, (P.M.Rajagopal) Master Circular on Collection of Direct Taxes 6. With a view to improving customer service to direct taxpayers, special attention was drawn to the following provisions of ‘Accounting System for Direct Taxes’ : (RBI/2004/135 (DGBA.GAD.No.1142 /42.01.001/2003-04) dated April 2, 2004) (i) Issue of Token : While instructions issued by Reserve Bank regarding the issue of paper token as an acknowledgement of payments are very clear, it is observed that a large number of authorised branches do not issue such tokens. In many places, there are informal arrangements wherein the taxpayer is asked to collect the challan after a specific date from the bank branches. In some cases, the receipted challans are not kept securely and are placed in an open box. The customers are allowed to freely pick up their challans without any identification. In the case of challans deposited with cheque or draft, the receipted challans will be issued only on realisation of the amount of cheque or draft and hence the paper token should indicate the date on which the receipted copies of the challans would be kept ready so that the assessee makes an arrangement to collect the receipted challan on the date given in the token. (ii) Receipted Challan: The receipted challan should be made available to the assessee within 4-5 days, based on the local Clearing arrangements. The branches should ensure that this stipulated waiting period must not be exceeded and any deviation in this regard will be viewed seriously by Reserve Bank. The receipted challans should be handled with care and in a secured manner till they are handed over to the assessee across the counter on presentation of the relevant paper token. Under no circumstance, the receipted challan should be kept in open box accessible to customers. (iii) Double Date Stamp on Receipted Challan: It is reiterated that the challan should bear two dates i.e. the 'Date of tender' of challans and instruments and the 'Date of realisation' of proceeds of the instruments as specified in Annexure-V of the Pink Booklet. (iv) Acceptance of Clearing Cheques: It is observed that some of the banks are reluctant to accept cheques drawn on other banks while receiving taxes resulting in practice of Chartered Accountants/Tax Consultants tendering their own cheques on behalf of their clients. As accepting cheques drawn on other banks will greatly facilitate the customers, banks are advised not to turn back customers who tender challans with cheques drawn on other banks. (v) Do's and Don’ts : A list of Do's and Don'ts as given in the Annexure-IV of the Pink Booklet were not being supplied to the bank staff dealing with the Direct Tax collection work as required. The same may be issued to the branches. (RBI/2004/131 (DGBA.GAD.No.1008/42.01.034/2003-04) dated April 1, 2004, RBI/2004/145 7.1 A High Powered Committee (HPC) was constituted by Reserve Bank for setting up OLTAS in January 2003. The HPC set up a Sub-Committee to suggest the Accounting Procedure for Online Tax Accounting System. The Accounting procedure duly approved by CGA and CAG was introduced for OLTAS w.e.f June 01, 2004.The new accounting procedure (Annexure) was forwarded to all agency banks on April 16, 2004. The salient features of the new accounting procedure are the introduction of a single copy challan with tear-off taxpayer’s counterfoil, branding of acknowledgement stamp with unique serial number known as Challan Identification Number (CIN) on the single copy challan and on taxpayer’s counterfoil. Tax payers are now able to view the tax paid by them by logging on to http://tin-nsdl.com. Further, the new file structure required by Income Tax Department was also forwarded to Agency banks for developing suitable software for the OLTAS. 7.2 Under the new procedure banks were advised to issue acknowledgement in respect of challans tendered with clearing cheques/drafts (i.e. other than cash and transfer cheques/drafts) only after the realization of such cheques/ drafts. Banks were further advised to issue paper token in respect of such challans indicating the date of tender and the date on which the counterfoil will be kept for delivery. The receiving banker was advised to return the tear-off portion of taxpayers’ counterfoil on realization of such cheques/ drafts after branding with the rubber stamp acknowledging the payment with Challan Identification Number (CIN) comprising of the following: 7.3 The tear off portion of the challans accompanied with cash or cheques drawn on the same receiving branch may be returned to the taxpayer on the same day with necessary acknowledgement by branding with the rubber stamp prescribed above. 7.4 All the non-computerised/ non- networked branches were advised to ensure that data pertaining to those branches be transmitted from its nearest computerized/networked branch to the Nodal branch and from Nodal branch to Link Cell electronically so that complete data pertaining to all the authorized branches of a bank throughout India are seamlessly transmitted to the Tax Information Network (TIN) hosted by NSDL. 7.5 It was further advised that the new accounting procedure under OLTAS will replace the existing procedure in so far as the sending of scrolls and challans to the Income Tax Department is concerned. It was also advised that except for the changes proposed in the OLTAS Accounting Procedure forwarded to banks, the instructions contained in the Pink booklet “Accounting System for Direct Taxes” (Updated upto June 30, 1999) will continue to be in force. 7.6 Further, need for transmitting data online to TIN in addition to the normal practice of sending paper scrolls and challans to the ZAO and Income Tax department was also emphasised. 7.7 It was suggested to banks that their Link Cells at Nagpur may be connected to TIN (NSDL) at Mumbai with a dedicated leased line to ensure secure two way communication. 8. Transmission of data to NSDL - Validation Checks 8.1 Various types of errors noticed by National Securities Depository Ltd. (NSDL)/Income Tax Department in the data uploaded by banks have been advised to the banks. In particular, data entry errors noticed in respect of PAN/TAN Number, incorrect nodal scroll branch data, assessment year, absence or incorrect tax-payer's name, CIN Numbers, major head codes and amounts were brought to the notice of banks. 8.2 To counter the lacunae observed, it has been decided that each bank will incorporate the following validation checks with immediate effect in the OLTAS software for all Record Types: (iii) Name field is always mandatory and it should have a combination of alphanumeric and dots only and it should be of more than one character (the name string should not be of dots and numeric or both. Alphabets must be there in main string). It is mandatory to transmit the full name of tax payer irrespective of the fact that PAN/TAN has been mentioned on the challan. (iv) ZAO code number of a collecting branch is permanent and details of ZAO code numbers are available in the pink booklet published by the Reserve Bank. Nodal Branches must ensure that this ZAO code number is correctly mentioned in Record Type 01 and is not altered under any circumstances. It is advised that all the banks should save the code in the ZAO field in their OLTAS software as instances have been brought to the notice of RBI/Government where the same branch is mentioning different ZAO code on different dates of transmission. 8.3 In addition to the above validation checks, the following supervisory steps have to be taken by banks: (i) Branch Managers of the collecting branches must ensure correctness of the name and amount captured from the challans. For this ‘maker-checker’ system of data entry must be adopted in all the bank branches. (ii) All collecting branches must compulsorily transmit Record Type 01 and Record Type 02 (Summary Record), if there is collection on that day. In branches where there has been no collection during the day, only Record Type 02 (NIL statement) is to be transmitted to the Nodal Branch. This would enable the TIN to accurately monitor the implementation of OLTAS. (v) All the banks at Link Cell level should maintain an error record of action taken on error records transmitted to TIN. This would ensure that all records which had initially been rejected by TIN due to some deficiencies are compulsorily retransmitted to TIN after removal of lacunae within 48 hours. (vi) It is observed that the banks are entering wrong major head codes i.e. interchanging payments received under Major Head 020 for Corporation Tax or Major Head 021 for Income tax other than Corporation Tax. This leads to avoidable misclassification of payments and affects the reconciliation of accounts between the Income Tax Department and ZAO. In case of a valid PAN, the above validation can be implemented in the OLTAS software i.e. if 4th character (from the left) is ‘C’ then Major Head code must be 020. 8.4 Income Tax Department has also informed us that while transmitting assessment year data, banks were required to transmit the first part for normal as well as block assessment years; for example for the normal assessment year 2005-2006 the bank is required to transmit 2005 and for a block assessment year like 1997-2005, the year 1997 should be transmitted. 9. Sending daily scrolls by e-mail to ZAOs (RBI/2006/295(DGBA.GAD.No.H-11140/42.01.034/2005-06 dated February 2, 2006) Banks were advised of the revised format of electronic Nodal Branch Daily Main Scroll for Direct Tax Collection. The revised format (Annex III) is to be used to send the Daily Main Scroll electronically to all ZAOs pending receipt of physical challans/scrolls from all receiving branches. 10. Abolition of Sub-Agency Arrangements for Collection of CBDT Dues (RBI/2004/326(DGBA.GAD.No.3278-3311/42.01.034/2004-05) dated Dec. 31, 2004) It was observed that one of the major reasons for non-uploading of data under OLTAS is the existence of Sub-Agency arrangements with another prominent bank in the locality where the Sub-Agency bank concerned does not have sufficient number of branches for having its own Nodal Branch as per the norm then prescribed by CBDT. Due to non-compatibility or for other reasons, the data in respect of challans received by collecting branches under sub agency arrangements were not uploaded to TIN by the Principal Agency banks in many cases. With a view to avoiding delay and problems arising out of the sub-agency arrangements, it has been decided in consultation with Directorate of Income Tax (Systems), New Delhi to discontinue the Sub-Agency arrangement altogether. Banks were advised to designate their own Nodal branches wherever their branches were functioning under sub-agency arrangements. 11. Funds Settlement - Reporting to RBI, CAS Nagpur (RBI/2005/466 (DGBA.GAD.No.H. 5801 /42.01.034/ 2004-05) dated May 13, 2005 & RBI/2005/406 11.1 Keeping in view the decision to switch over to settlement of funds on the basis of on-line data uploaded to TIN with effect from April 1, 2005, the existing system of reporting CBDT transactions to RBI, CAS, Nagpur has been reviewed. Accordingly, it was decided that agency banks will submit the CBDT figures to RBI, CAS, Nagpur separately through digitally signed e-mail (to be signed by a class II certificate holder). The CBDT figures reported to TIN as at 13.15 hours on week days and 12.30 p.m. on Saturdays would simultaneously be reported to CAS, Nagpur for funds settlement through digitally signed e-mail. The data mailed after the cut-off time would not be accepted by CAS, Nagpur under any circumstances. 11.3 It was clarified that the financial data file uploaded to CAS, Nagpur on any given date for funds settlement and the challan data relating to that particular settlement date uploaded to TIN should exactly match. Files rejected subsequently by NSDL, if any, due to validation errors etc. should be processed separately and re-uploaded.Banks were advised to ensure that challan data in respect of each and every challan deposited by the assessee is uploaded and duly accepted by TIN. Such re-uploading of files to TIN would not affect the funds settlement data. The requirement of complete reporting to TIN would be achieved if the data going from Link Cells to CAS, Nagpur and the relative challan data going to TIN are uploaded simultaneously. 11.4 Link Cells were advised to ensure that there is no mismatch in figures uploaded to CAS and TIN for a given uploading date. 11.5 Nodal Branches were advised to follow the instructions contained in paragraph 6 of the ‘Accounting Procedure Relating to On-line Tax Accounting 12. Certain clarifications issued by the RBI for guidance to banks as regards OLTAS are reproduced below: (RBI/213/2004(DGBA.GAD.NO.H-1169/42.01.034/2003-04) dated May 22, 2004 & RBI/2004/181 12.1 Challan Identification Number (CIN) 12.2 Banks were requested to visit Income Tax website (www.incometaxindia.gov.in) for Frequently Asked Questions (FAQs) on OLTAS. 13. Further, banks were advised to ensure full participation of authorized branches and ensure that every challan record is transmitted to TIN by every branch where tax collection has been made. It was reiterated that a NIL statement (Record type 02) may be transmitted to the nodal branch when there had been no tax collection during the day to enable TIN to monitor OLTAS properly. It was also emphasized that the data transmitted to TIN should be correct and complete and conforms to the stipulated procedures. 14. Banks were advised of the following critical short comings which were brought to the notice of RBI by Directorate of Income Tax: 14.1 Non capture of PAN/TAN by banks - It had been reported from many centres that even where the taxpayer has correctly quoted his PAN in full, certain bank branches were either not entering it or were entering it in an incomplete manner. In this connection banks were advised that under the On-line Tax Accounting System (OLTAS) procedure/rules, it had been laid down that wherever the 10 digit PAN/TAN in the proper alpha numeric structure is quoted by the taxpayer the banks would only have to capture the PAN and the name of the taxpayer and not the address. 14.2 Non capture of the full name of the taxpayer - Perusal of the data uploaded to TIN indicated that many bank branches are still putting only one or two characters in the name column of the taxpayer. In some cases even symbols and dots were used. Banks may please ensure capture of taxpayer’s full name in OLTAS data. 14.3 Incorrect address field - The data analysed also reveals that the address field was not being captured properly by many bank branches. In many cases, just a few random alphabets or numbers were being entered which again indicated that the bank branches were not taking adequate care for full data capture. Banks were advised to take necessary corrective action. 14.5 Non uniform scroll data - As per the On-line Tax Accounting procedure rules, the scroll of a Nodal Branch for a particular day is to be identical for both the ZAO as well as for the data transmitted on OLTAS to TIN. It was, clarified that all collection data being sent to ZAO and TIN for a particular day must match both in respect of number of challans and Major Heads. Further banks were advised to ensure that each and every challan record is sent to TIN by every branch where collection has been made.” 15. De-authorisation of bank branches for collection of Direct Taxes (RBI/2005/412 (DGBA.GAD.No.H 5318 /42.01.034/ 2004-05) dated April 4, 2005 ) 15.1 With a view to streamlining the procedure for delisting of authorised bank branches under OLTAS, it has been decided in consultation with the office of Principal Chief Controller of Accounts (Pr CCA), CBDT, New Delhi that any proposal for deauthorisation of branches should be submitted by the Head Offices of the Agency banks to RBI, Central Office keeping in view the following parameters/ guidelines: 15.2 After the proposal is approved by RBI/ Office of Pr.CCA, CBDT the concerned bank should give wide publicity to the effect that the specific branch will discontinue acceptance of taxes with effect from a specific prospective date and advise us accordingly. 16. File Segregation Utility developed by Tax Information Network Requests have been received from some banks that Tax Information Network (TIN) should not reject the entire file of OLTAS data received from a bank's Link Cell because of a few erroneous records. The banks have desired that TIN should accept the records which are with correct validations while rejecting the erroneous records. On the basis of the discussions CBDT had with NSDL (TIN) And banks, TIN had developed a File Segregation Utility which was advised to banks. (Annex II) 17. Accounting Procedure relating to crediting of CBDT collections to Govt. Account – Public Sector Agency Banks (RBI/2005/411 (DGBA.GAD.No. H- 5287/42.01.034/2004-05) dated April 1, 2005, RBI/2006/150 17.1 It has been decided in consultation with Government of India to amend the instructions relating to the maximum number of days allowed for crediting tax collections to T+3 working days (where T is the day when money is available to the bank branch) instead of T+3 days (including Sunday and Holidays) with effect from April 1, 2005. For calculating working days holiday list of CAS, Nagpur will be reckoned. 17.2 It has been decided that the put through date, i.e. the date of settlement with the CAS, RBI shall be kept outside this existing time limit of T+3 working days. 17.3 Delayed period interest shall be imposed on banks for the delayed period and not from the date of transaction. In other words, the ‘delay period’ calculation will start from the day following the put through date. 17.4 The period of delay in a transaction of Rs.1 lakh and above shall attract delayed period Interest at Bank Rate + 2%. The Bank rate will be the rate as being notified by the RBI from time to time. 17.5 For the transaction below Rs.1 lakh each, the delayed period interest shall be levied only at the Bank Rate for delays up to 5 calendar days and above 5 calendar days at the Bank Rate + 2 % for the full period of delay. The Bank Rate will be the rate notified by the RBI as applicable at the time of transaction. 17.6 It has also been decided by the Controller General of Accounts that every Principal Chief Controller of Accounts (Pr.CCAs), Chief Controller of Accounts (CCAs) and Controller of Accounts (CAs) in Ministries/Departments shall undertake Quarterly Review of all the remittances made by the banks. If the delay is found to be 5% and more with the bank as a whole or with any of its branches in two successive quarters, authorisation for the concerned bank or the branch will be forwarded to the CGA for review with the recommendations of Pr.CCA/CCA/CA. The banks are expected to build up their own internal control mechanism so that the preventive and corrective actions are taken by the bank for its branches well in time. 18. Accounting Procedure relating to crediting of CBDT collections to Govt. Account – Private Sector Agency Banks. 18.2 Further, the instructions given at Para 17.6 above will also be applicable to private sector agency banks. 19. Drawing of Cheques by Assessees- Payees Name (DGBA.GAD.No.H-8294/42.01.037/2005-06 dated December 14, 2005) With a view to obtaining uniformity in the Payee’s name while drawing cheque/DD by assessees for depositing challans for Direct Tax Payment under OLTAS, it has been decided by the Income Tax Department to print the following instructions on the reverse of the Income Tax Challan : “Tax payer may please draw/issue cheque/DDs towards payment of Income Tax as under: Banks were advised to bring the change to the notice of all their authorised branches. 20. New Major Heads/Challans (RBI/2005/39 (DGBA.GAD.No.H-42 /42.01.034/2005-06) dated July 4, 2005) Banks were advised of the revised challan formats introduced by Government of India which were necessitated by the introductions of two new taxes i.e. Fringe Benefit Tax and Banking Cash Transactions Tax. Consequent changes/ rationalization made to Major Heads and Sub-Minor Head of Accounts by Income Tax Department are given below: CHALLAN NO.ITNS - 280 CHALLAN No.281

CHALLAN NO.282 This challan is for the payment of a number of taxes. The changes introduced in this challan are as under: CHALLAN NO.283 21. Verification of PAN/TAN (RBI/2006/55(DGBA.GAD.No.H-161/42.01.034/2005-06 dated July 7, 2006)) 22. Compulsory Quoting of Permanent Account Number (PAN)/Tax Deduction Account Number (TAN) on Challans from 1/1/2005 (RBI 2004/300 (DGBA.GAD.NO.H-2532-65/42.01.034/2004-05) dated December 14, 2004 & With a view to ensuring correct and prompt credit to tax payers, Central Board of Direct Taxes (CBDT), Government of India have decided to implement the provisions for mandatory quoting of PAN/TAN on Challans from January 1, 2005. Accordingly, no payment of taxes will be accepted by bank branches unless the PAN of the tax payers is quoted on Challans ITNS 280 & 282 or TAN of the deductor on Challan ITNS 281, as the case may be. The branches may display a notice prominently stating that ‘Quoting of PAN/TAN on Challans is compulsory from 1/1/2005’ in the branches and not to accept challans without PAN/TAN from that date. The procedure for obtaining PAN/TAN is available in the website of Income Tax Department (http://www.incometaxindia.gov.in or http://www.tin-nsdl.com). The branches may guide the assessees to obtain PAN/TAN before depositing the tax. The facility of downloading the challan form No. 280 & 281 with pre-printed PAN/TAN number may also be given wide publicity through your designated branches. 23. Banking Cash Transaction Tax (BCTT) (RBI/2005/43(DGBA.GAD.No.H-76/42.01.001/2005-06) dated July 5, 2005) 23.1 Banks were advised the procedure to be followed as regards levy of Banking Cash Transaction Tax on the cash withdrawal by the Government departments. Extract of the same is reproduced below: 23.2 The BCTT is also payable, among others, by an office or establishment of the Central Government or a State Government. Accordingly, Central Government Offices or establishments will be liable to pay the BCTT on the amount of cash withdrawn by them for their use, if the amount withdrawn by them is in excess of Rs.1, 00, 000/- (Rupees one lakh), in a single day from a single account. 23.3 In this connection, Government of India has observed that deducting the BCTT from the cheques’ amounts drawn by Government Departmental Officers by Agency Banks is not correct. Banks are, therefore advised to stop the practice forthwith. 23.4 In order to enable Banks to recover the tax from the Government departments, banks are advised to directly debit the Government account through the payment scrolls. The BCTT may be shown just below the relevant cheque amount in the payment scroll, indicating in clear words “Banking Cash Transaction Tax”. 23.5 Insofar as the reporting and settlement of the collections with the Reserve Bank of India, CAS, Nagpur and ZAOs of CBDT is concerned, banks will follow the procedure already prescribed for the purpose with respect to “Direct Taxes”.” 24. Obligation of Scheduled Banks to furnish (RBI /2005/ 85 (DGBA. GAD. No. H- 414 /42.01.001/ 2005-06) dated July 30, 2005) 24.1 As per Rule No. 5 of the Government Notifications No. 156/2005, dated May 30, 2005 scheduled banks are required to furnish a statement of number of taxable banking transactions entered into and Banking Cash Transaction Tax collected during the month on or before the expiry of the month immediately following the relevant month on a computer media. 24.2 Banks may, therefore, furnish the information in the manner and media as prescribed in the Rules at the address mentioned below: 25. On Line Tax Accounting System (OLTAS)- (DGBA.GAD.No.3774/42.01.034/207-08 dated October 9, 2007 RBI/2007/206 & DGBA. GAD. No.6212/42.01.034/2007-08 dated December 6, 2007) 25.1 Discrepancies in challan details uploaded to TIN It was brought to the notice of banks that the OLTAS data uploaded to TIN by them do not match with the relative data submitted through TDS/TCS returns submitted by detectors. Common irregularities observed were: (i) Date of Realisation is digitized as Challan Tender Date in the data uploaded through OLTAS. (ii) Uploading of incorrect Challan Serial Number, Major Head, PAN/TAN etc. (iii) Challan Serial No. not Stamped on challan counterfoil. (iv) Amount indicated against single challan bifurcated into two amounts and reported in two challans. Banks were advised to avoid the above errors and be more careful while capturing and uploading OLTAS data. 25.2. Data Quality Concerns In order to achieve accuracy in reporting PAN & CIN to TIN the agency banks were advised to: (RBI/2008/328 & DGBA GAD. No.H.12070/42.01.034/2007-08 dated May 22, 2008) The Agency banks were advised to issue computerized receipts for challan payments of OLTAS transactions comprising of relevant data as per prescribed proforma i.e. annex A-IV-I & II w.e.f June 01, 2008. The agency banks further advised to follow additional guidelines as under: 27. Cut off time for e-Payment transactions pertaining to Government Revenue (RBI/2008/275 & DGBA. GAD. No.10577/42.01.038/2007-08 dated April 3, 2008) Banks authorized for e-payment of CBDT revenue were advised that payment under OLTAS received up to 8.00 p.m. may be treated as received on the same day and those received thereafter be treated as received on next working day. 28. Mandatory Electronic Payment of Tax by Certain Categories of Taxpayers w.e.f. April 1, 2008 (RBI/2008/280 & DGBA. GAD. No.H.10875/42.01.038/2007-08 dated April 10, 2008) CBDT has made electronic payment of taxes mandatory for the following categories of taxpayers: (RBI/2008/321 & DGBA. GAD. No.H. 11895 /42.01.038/ 2007-08 dated May 15, 2008) The Agency Banks were supplied a CD containing area-wise PAN and names of taxpayers coming under Section 44AB of IT Act for the financial year 2007-08 and to take following action in case of submission of challan with cheque by taxpayers covered under Section 44AB of IT Act, which can be verified from the CD containing area wise PAN and names of the taxpayers coming under Section 44AB: ACCOUNTING PROCEDURE RELATING TO ON-LINE TAX 1. Procedure for acceptance of taxes at the receiving branches 1.1 A taxpayer can pay direct taxes at any authorised branch of the authorised bank either in cash, direct debit to account or by a cheque/draft drawn on the same bank or another bank/branch at the same centre where the payment is made. The payment of tax by outstation cheques/drafts can also be made at any authorised bank, or through an electronic means of remittance to the authorized bank / branch. For every payment there should be a challan in the prescribed format. The challan format is a single copy challan with the main challan at the top and the taxpayer’s counterfoil at the bottom of the challan (Specimen at Annexure 'A'). 1.2 At the counter of Receiving Bank Branch a. Whether main portion of the challan and the taxpayer’s counterfoil form have been filled in properly and the amount and major head of account to which the amount is to be accounted /credited is correctly recorded therein; b. Whether details of the Permanent Account Number (PAN) or Tax Deduction Account Number (TAN), name and address of the taxpayer, assessment year and nature and type of payment are properly filled in. The amount should be written correctly both in words and figures. c. Whether the Permanent Account Number (PAN) / Tax Deduction Account number (TAN) has been quoted in the challan at the prescribed place. U/s 139 A (5) (b) of the Income Tax Act, quoting of PAN is mandatory. Similarly, u/s 203A of the Act, quoting of TAN is mandatory. This number, as quoted by the taxpayer should be validated (checked to see whether it is in conformity with the valid PAN/TAN structure) and the designated banks accepting tax payment should ensure that the challans for payment are accepted only when a valid PAN is quoted in the challan. However, where the taxpayer indicates that he has already applied for allotment of PAN or TAN but has not yet been allotted the same, the tax payment challans may be accepted by the bank provided the tax payer indicates PAN/TAN application number in the challan. In such cases it should invariably be ensured that the full address of the taxpayer has been mentioned in the challan. 1.3 After scrutinizing the challan and satisfying himself that the amount of cash, cheque or draft tendered agrees with the amount shown in the challan, and also that the cheque is not post dated/stale the receiving teller or counter-clerk of the branch will issue a paper token to the tenderer to facilitate delivery of the counterfoil receipt to him. In the case of challans deposited with cheque or draft drawn on other bank branches, the counterfoil receipt will be issued only on realization of the amount of the cheque or draft and hence the paper token should bear the date on which the same will be available. 1.3.1 Challans tendered with Cash A challan tendered with cash, if found in order after scrutiny, will be stamped ‘CASH RECEIVED’. The bank will also stamp both the main portion and the taxpayer’s counterfoil of the challan with a stamp mentioning the name of the bank & branch, the BSR code the branch (7 digits), date of deposit (DDMMYY) of the amount and unique serial number of the challan (5 digits). The stamp will be impressed on both the main portion as well as the taxpayer’s counterfoil of the challan. Care must be taken to ensure that the impression of the receipt stamp is clear and legible. An authorized official of the branch will sign in full the taxpayer’s counterfoil of the challan and initial the main copy of the challan having received the amount. In the taxpayer’s counterfoil, the amount received will be indicated in both words and figures. The receipted taxpayer’s counterfoil will be returned to the tenderer and the main copy will thereafter be passed on for scrolling in the Receipt scroll. 1.3.2 Challans tendered with Cheque/Draft A challan tendered with cheque/ draft will be branded with a ‘double date stamp’ to indicate the date of tender of the instrument as well as the date of realization thereof. It may be possible that some branches might be following the practice of branding the challans with an inward date stamp as soon as the challans are tendered over the counter. In that case the double date stamp may not be necessary. However, it will be ensured that the inward date stamp is invariably branded on both the main copy and the taxpayer’s counterfoil of the challan. The checking official will initially ensure that there is no difference between the amount of cheque/ draft and the amount recorded in the challan by the tenderer. The cheque/ draft will thereafter be sent for realization. Subsequently, on realization of the cheque/draft, the date of realization will be indicated on the double date stamp or in the space in the challan as the case may be. The bank will also stamp both the main and the taxpayer’s counterfoil of the single copy challan with a stamp mentioning the name of the bank & branch, the BSR code the branch (7 digits) date of deposit (DDMMY) of the amount and unique serial number of the challan (5 digits). After signing the challan for having received the amount, the taxpayer’s counterfoil will be returned to the tenderer against the surrender of the token. 1.3.3 Numbering of Challans Running serial number will be given for all the challans (both paid by cash and by cheque) for each day. It must be ensured that the serial number on each challan issued on a particular day should be unique to trace it subsequently. The bank must therefore ensure that the serial numbers given to the challans deposited with cash do not overlap with the serial numbers given to the challans against which cheques have been realised on that day. Counterfoil of the challans tendered along with cash and cheque/draft payable at the same branch will be returned to the tenderer duly receipted at the counter. The challans tendered with cheques/drafts drawn on a different branch of the same bank or any other bank situated at the same centre, the tax-payer’s counterfoil will be returned duly receipted not later than the working day following the day fixed under the Rules of ‘Local Bankers’ Clearing House’ for return of unpaid instruments of any day’s clearing. 1.4.1 In case of challans tendered with cheque/ draft, the date of realization of the cheque will also be stamped on the main portion of the challan, which will be retained at the bank for onward transmission to Zonal Accounts Office (ZAO) along with the Receipt Scroll. Although as per the Income Tax Act the date of presentation of cheque/ Demand Draft realized will be treated as date of payment of tax, the cheque/ Demand Draft will be scrolled only after realization. 1.4.2 Double Date on Receipted Challan The main portion of the challan through which a cheque/ draft is deposited will, therefore, have two dates as under: i) Date of tender : DDMMYY (in the rubber stamp acknowledgement) ii) Date of realization: DDMMYY (at the place indicated in the challan) In case of cash tender the ‘Date of tender’ and ‘Date of realization’ will be the same. 2. Preparation of Scrolls by the Collecting Branch 2.1 A running serial number will be given to all the challans received at a bank branch counter on each day against which cash payments have been made or cheques/ drafts have been realized on that date. 2.2 All the challan fields such as name and PAN, the serial number, date of deposit and BSR code of the branch are required to be captured when the challan is deposited by the tax payer at the bank counter. The data structure of the fields of the challan for which data has to be captured and transmitted will be as informed to the banks by the Income-tax Department. Permanent Account Number (PAN) and the name of the taxpayer will invariably be incorporated in the Receipt & Payment Scroll. 2.3 At the end of customer banking hours, the bank branch should identify all those challans against which payment has been received in cash for the day or for which payments by cheque/draft have been realised for the day. As the details of all these challans is already in the bank’s computer system, the branch should generate a file containing all the challan data for which payments have been realised for that day and transmit it to its Nodal Branch for onward transmission to the Income Tax Department’s TIN through the banks' Link Cell. However, the non- computerized/ non- networked authorized branches should ensure that data is transmitted from it’s nearest computerized/ networked branch to the Nodal Branch. It should be ensured that no challan for which payment has been realised on that day is left out. A running scroll serial number extending through a financial year (1st April to 31st March) will be given to the records relating to each type of tax (major head) which are transmitted on a particular day. The complete data structure of records and the file which is to be transmitted by the bank to the Department will be in the format prescribed by the Income-tax Department. The collecting branch will in no case alter the online data file at its end after it has been transmitted to the Income Tax Department. 2.4 Treatment of Clearing Returns The collecting branch should also identify all those challans against which instruments were returned unpaid. Such instruments along with related challan should be kept separately in the bank for taking further necessary action as deemed fit. 2.5 The collecting branch will also generate separate printouts of the scrolls in Form and summary in Form based on the type of tax (major head-wise) on a daily basis from the challan data on its computer which has been transmitted to the Income-tax Department. The same running serial number extending through a financial year (1st April to 31st March), which was given to the scrolls transmitted for the relevant day, prefixed by the appropriate abbreviation of the type of tax (major head) concerned, will be printed on the scroll. The collecting branch will in no case generate any printed scrolls or summary from data which is changed in any manner from the data earlier transmitted to the Department. Thus the scrolls generated by the branch will exactly match the scrolls generated by the RCC from the data transmitted to the Department's TIN on-line by the bank. Thereafter, the branch will prepare a set of computer printed summary and receipts scrolls and attach with each scroll the physical challans arranged in the same serial order in which they are entered in the scrolls. At the beginning of the next working day, the receiving branch will forward the same to the Nodal Branch for onward transmission to the ZAO. 2.6 Transmission of Error Records In case of any error by the collecting bank branch in reporting the amount of payment made by a taxpayer or major head of payment, the bank will transmit the corrected information on-line to TIN through an error record, the format for which will be as prescribed by the Income-tax Department. Rectification of the errors in the amount and the head of account will also be reported to ZAO through ‘Error Scroll” to be sent through Nodal branch. Only the amount of tax payment as reported by the bank to the TIN will be accepted by the Income-tax Department as the payment made by the taxpayer. 3. Procedure for Payment of Income Tax Refund Orders (ITROs)/ECS 3.1 Direct tax refund work is entrusted to only one branch of an authorized bank generally Reserve Bank of India, State Bank of India or its Associate Banks at an ITD centre / a District. The Refund Orders will be presented to the branch by the taxpayer for transfer to his account with the same branch. Alternatively, it might be received through clearing. The specimen signatures of the officers of the Income-tax department who are authorized to draw refund orders will be sent to the paying branches concerned in advance by the Income-tax authorities. The specimen signature will be duly certified by an officer of the Income-tax Department whose specimen signature is already on record with the branch. Any change in the authorised official will be advised to the branch concerned immediately. The relieved officer will attest the specimen signature of the relieving officer. While passing the refund orders for payment, the passing official should exercise utmost care apart from the precautions usually exercised by the banks in connection with payment of Negotiable Instruments, the instructions issued by Controller General of Accounts as well as Reserve Bank from time to time. The payee is required to affix his signature in the space provided for 'Claimants signature' on the reverse of the Income Tax Refund Order (ITRO).The procedure relating to Refund Advices will continue as at present except that advices of paid ITROs and printed payment scrolls will no longer be sent by the bank to the Income-tax Department. 3.2 As in the case of receipts, refunds are required to be classified by the paying branch according to the type of tax under which the refunds are made. Separate major head wise payment records will be maintained in respect of payment of ITROs. 3.3 Direct tax refunds can also be credited directly to the taxpayer’s bank account through Electronic Clearance Scheme (ECS) of RBI. In order to avail of this facility, the taxpayer gives a mandate by mentioning type of his bank account (Savings or Current), account number and bank branch code (9 digit) in his Return of Income. After processing of the taxpayer’s Returns and determination of the refund by the Assessing Officer, all taxpayer’s refunds (in which credit through ECS has been sought) in the jurisdiction of an RCC are automatically consolidated on the computer system at the RCC. All this refund data is downloaded, encrypted and copied onto a magnetic media (floppy or rewriteable CD) or transmitted electronically. This is sent by the RCC to the local ZAO as well as refund issuing branch of RBI or SBI. After validating the data in the file, the bank debits the Income-tax Department Account for the total amount of the refunds and thereafter issues instructions through clearing to the different local braches of the banks where the taxpayer’s accounts are located to credit the taxpayer accounts with the amount intimated by the Department. This single debit to the Department’s account appears in the payment (refund) data transmitted by the bank to the Income Tax Department for that day. In case any of these credits to the taxpayer’s accounts are not effected due to reasons like closing of the account etc., the same is later accounted for by a separate minus debit entry for ECS Return in the Income Tax Department’s account and is intimated to the Income Tax Department through the payment (refund) data transmitted for that particular day. The files in the electronic media (floppy or rewriteable CD etc.) are returned along with the computer printed payment (refund) scroll to the ZAO while the same data is transmitted online by the bank to the Income Tax Department through the Income Tax Department’s Tax Information Network (TIN). 4. Preparation of Payment (Refund) Scrolls 4.1 The procedure for preparation of payment scrolls will be the same as the procedure applicable to receipts scrolls. 4.2 The scrolls will be made into set similar to the set relating to receipts except that instead of the challans, the paid Refund Orders will accompany the scrolls. The entire data regarding the paid refund vouchers will be transmitted electronically by the paying bank to the Link Cell for onward transmission to the Department’s TIN while the physical scrolls with the paid Refund Order will be forwarded to the ZAO through the Nodal Branch. If the Nodal Branch is not locally situated, all the above documents (receipt/payment scrolls etc.) should invariably be sent by Registered Post. 4.3 In the case of ECS Refunds, the data will be transmitted on-line to the Link Cell and subsequently to the Income Tax Department while the same ECS detail on electronic media will be sent to the local ZAO by Paying Bank through the Nodal branch 5. Loss of Counterfoil by the taxpayer 5.1 In the event of loss of receipted challan counterfoil by the depositors, the bank branches may, on receipt of a specific request in writing for issue of a certificate of credit from assessees, issue the same to the depositor based on their record after satisfying themselves about the bonafides of the applicant in each case and may charge a nominal fee at its discretion. The certificate should mention the challan details i.e. amount, bank name and branch, BSR Code and Date of Deposit of cheque/cash, major head, challan serial number, date of realisation of cheque /date of deposit of cash and Collecting branch scroll number and date on which details of tax payment have been transmitted earlier. 6. Functions of Nodal Branch 6.1 Nodal Branch will be responsible for the prompt and accurate transmission, accounting of the collections/refunds reported to it daily by all the receiving branches under its jurisdiction (including its own receipts). It will also be responsible for prompt remittance of the collections of all the receiving branches linked to it (including its own collections) to the Government Account at RBI, CAS, Nagpur. It will also be responsible for reconciliation of figures with the ZAO. 6.2 On receipt of on-line data regarding all the challans realised for a particular day from the Collecting Branches, the Nodal Branch will take the following action on day-to-day basis: a. It will collate the challan data on its computer system and transmit the data in the format prescribed by the Income Tax Department to its Link Cell for onward transmission to the Departments TIN on the same day after giving a common Nodal Branch scroll number and date to all the challan records being transmitted on that day. b. It will also generate a copy of the summary and main scroll based on the computer data in a floppy or other media (as informed by ZAO) and transmit it to the ZAO on the next working day. c. On receipt of the hard copy of the computer-generated Branch scrolls from the collecting branch, the Nodal branch will validate that these computer-generated branch scrolls exactly match the data transmitted earlier by the collecting branches. It will consolidate these computer printed Branch scrolls (with challans) received from all the branches including its own along with the main scroll by stitching the scrolls together Major head-wise. It will also generate a computer printout of the Major head-wise Main scrolls and Summary. It will then forward these (with challans) to the ZAO concerned on a daily basis. d. Second set of scroll prepared in the same manner without challans as discussed at (c) above will be retained by the Nodal branch for its record. e. The Nodal branch will also similarly generate computer printed separate main scrolls for payments (i.e. refunds), and forward them along with the paid ITROs to the ZAO. It will also forward ECS refund details on electronic media to the local ZAO. The refund data (in respect of paper ITROs and ECS refund) will be transmitted on-line by the Nodal Branch to TIN through the Link Cell. It will retain the advice/advices of the paid ITROs. f. During the first 15 days in April every year, the nodal branches will transmit and prepare two separate sets of scrolls – one normal scroll pertaining to April transactions and the other one pertaining to March transactions (which means scrolls of cheques / drafts / ITROs tendered and cleared upto 31st March by receiving branches and sent to the nodal branch subsequent to 31st March but before 15th April) - these will be scrolled by nodal branch as March residual account. The nodal branches will intimate the link cell at Nagpur for inclusion of these transactions as March transactions. The nodal branches will send another scroll for April transactions prominently indicating the month of account. Any cheque/draft tendered on or before 31st March and realised on or after 1st April will be treated as part of the April transactions. However, in light of the instruction that data for all challans for which payment has been realised on a given day should be transmitted online to the Income Tax Department on the same day, separate March residual scroll should only be needed in exceptional cases. g. The nodal branch will pass on the consolidated amount accounted by it to its Link Cell on day-to-day basis. 7. Crediting the tax collection to Government Account 7.1 The Nodal Branch acts as a pooling centre for all the receiving branches coming under its control and it is responsible for reporting of the transactions (along with all the related documents i.e. Challans and scrolls) to the ZAO. It is also responsible for transmitting the challan data for all these transactions to its Link Cell at Nagpur for onward online transmission to the Income Tax Department as well as for crediting the amount collected to Reserve Bank of India (Central Accounts Section or CAS), Nagpur. 7.2 The Nodal Branch will prepare a daily memo and send it on a daily basis to its Link Cell at Nagpur (GAD, Mumbai in case of SBI) which in turn will make a daily settlement with RBI, CAS, Nagpur. 7.3 The Link Cell of banks at Nagpur will consolidate the challan data received from the Nodal Branch for transmission to the Department's Tax Information Network (TIN) and will also monitor the daily receipts and check the accuracy of the daily memos received from the Nodal Branches. The Link Cell will then transmit the daily memos to CAS, RBI, Nagpur. 7.4 The Nodal Branches of the banks will carry out monthly reconciliation with ZAOs of the amount settled by them with their Link Cell at Nagpur. On the basis of their records the ZAOs will verify the statements received from the Nodal Branches both major head-wise and Nodal Bank-wise. In case of any discrepancy, the Nodal Branch will carry out the corrections immediately and adjust the difference in the amount already credited / debited to the CBDT’s account through its Link Cell at Nagpur under information to the ZAO. 7.5 For the purpose of final reconciliation of the transactions with ZAOs and the Link Cell, the CAS, RBI, Nagpur will generate a monthly statement and furnish the same to ZAO and the Link Cell of the banks. RBI, CAS, Nagpur will furnish by 20th of the following month, a monthly analysis indicating major head-wise receipts / refunds etc. to the CCA, CBDT. 8. Payment of interest on delayed transfer of tax collections 8.1 The tax collections effected by the designated branches of the authorized banks have to be credited to the Government Account, promptly on day-to-day basis. The maximum number of days allowed for crediting tax collections to Government Account at CAS, Nagpur is as under: 8.2 If there is any delay beyond the period prescribed above, the banks are liable to be charged interest for delayed period. The interest for delayed remittance as mentioned above is to be quantified and collected from the defaulting bank by the ZAOs. The rate of interest to be charged is Bank Rate as prevailing (which is generally notified biannually on May 1 and November 1) plus 2% or as decided by Reserve Bank in consultation with CGA from time to time. 9. Accounting of "March" transactions 9.1 Reserve Bank, Central Office, Mumbai will issue in the month of February each year special instructions to all banks collecting direct taxes regarding the procedure to be adopted in accounting the March transactions. 9.2 The Nodal banks will be receiving scrolls relating to March of the previous Financial Year in April of the current year. In order to account for the entire collections of March in the same financial year the Nodal banks have to follow the following procedure during the month of April: 9.3 It may also be noted that all the cheques / amount realized on or before 31st March should be treated as transactions relating to the current financial year and should be accounted for as such under the head “March or March Residual Transactions” in the current financial year. 9.4 While reporting to their Link Cell in Nagpur, the Nodal banks should send two sets of figures distinctly showing March Residual and April Transactions separately upto 15th April. 9.5 The date-wise monthly statements should also be prepared in two sets, one pertaining to March Residual Transactions and another relating to April Transactions. 10. Special arrangements during the month of March every year 10.1 The branches should follow the procedure explained in the earlier paragraphs meticulously and ensure that the collections made towards direct taxes are passed on promptly for credit to Government Account through the Nodal Branch / Link Cell. However, during the second fortnight of March every year, wherever the receiving branches and Nodal branch are situated locally, a special messenger system should be introduced by the receiving branches. All efforts may also be made to provide the collection figures on daily basis to the ZAO during the second fortnight of June, September and December every year, for onward transmission to the Government for monitoring, estimates etc. 11. Monitoring Committee - holding of periodical meetings 11.1 For the smooth functioning of the revised scheme for collection and accounting of direct taxes by the Authorised Banks, the Monitoring Committees consisting of officials from Nodal Banks/local authorities of the banks, ZAO and I.T. Department will be formed at every Zonal Accounts Office centre. The Committee will meet half-yearly and discuss various issues connected with direct tax work such as accounting, scrolling, reporting, remittance and reconciliation etc. and make efforts to sort out the problems at its own level. Further, annually there will be a special Monitoring Committee meeting in which very senior officials from CBDT, RBI, I.T. Department and banks will participate and redress the various problems being faced by the banks, ZAOs and I.T. Department in the fields. Banks will ensure that the necessary follow-up actions are taken on the Minutes of such meetings. 12. Redressal of public grievances 12.1 Each Authorised Bank should have an effective procedure for dealing with public complaints at the branches rendering service to Government Departments or members of the public as prescribed, from time to time. In case the bank detects a mistake in reporting of a tax payment or the major head of tax payment, either suo moto or being brought to its notice by the tax payer, the bank will promptly transmit the error record (as described earlier at paras 2.6 and 7.4) to TIN. This is imperative as the Income Tax Department will give credit to a taxpayer’s on the information transmitted by the bank to TIN. OLTAS Introduction Intended Users: Conventions used 1. Overview 2. Functionality

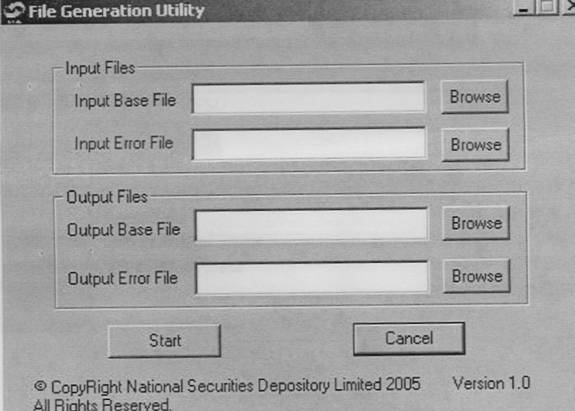

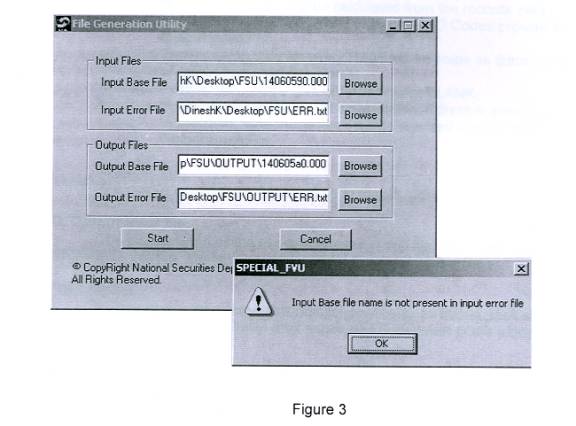

The utility contains name of utility at the top, buttons for minimizing and closing the utility, four text fields and four buttons named “Browse”, a start button and a cancel button. A copyright message and version number will also be visible. The user is required to enter valid inputs in all the four text fields described below. A. Input Base File: Input file name should be in “ddmmyyfv.bnk” format only.

File extension should contain valid bank code. B. Input Error File: There is no validation for name of the input error file.

Note : Output valid file will not get generated correctly if any one out of two input files has got tampered. Also Error file generated from FVU or obtained from OLTAS site is acceptable. NO OTHER formats should be used, as they may give wrong results. C. Output base file: a. Field MAJ_HD_CD, TOT_NO_OF_RFND, TOT_NO_OF_CHLN, TOT_NO_ERR_RFND, TOT_NO_ERR_CHLN, RFND_TOT_AMT, CHLN_TOT_AMT in RT04 are calculated from the records data present in output valid file. The output base file name should be in format “ddmmyyfv.bnk” D. Output error file : Start Button: Cancel Button: Annexure-A-IV-I Draft proforma of computer generated receipts

Annexure-A-IV-II Draft proforma of computer generated receipts

How do I make online tax payment sitting at home/office? Open a net-banking account with any of the banks listed above. What are the advantages of paying taxes online https://tin.tin.nsdl.com/oltas/index.html

For detailed information please go to: incometaxindia.gov.in PAY TAXES ONLINE IMP: In case of refunds adjusted against arrear demand, the normal refund should be attached with challan and sent to Bank by AOs as per earlier procedure. Master Circular — Index

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

ਇਸ ਪੇਜ ਨੂੰ ਸ਼ੇਅਰ ਕਰੋ:

ਭਾਰਤੀ ਰਿਜ਼ਰਵ ਬੈਂਕ ਮੋਬਾਈਲ ਐਪਲੀਕੇਸ਼ਨ ਇੰਸਟਾਲ ਕਰੋ ਅਤੇ ਨਵੀਨਤਮ ਖਬਰਾਂ ਤੱਕ ਤੇਜ਼ ਐਕਸੈਸ ਪ੍ਰਾਪਤ ਕਰੋ!

ਸਾਡੀ ਐਪ ਇੰਸਟਾਲ ਕਰਨ ਲਈ QR ਕੋਡ ਸਕੈਨ ਕਰੋ।

ਪੇਜ ਅੰਤਿਮ ਅੱਪਡੇਟ ਦੀ ਤਾਰੀਖ: